The greenest of all green shoots – the recent rise in housing prices – is little more than a mirage, according to Whitney Tilson, founder and CEO of T2 Partners, a New York-based hedge fund and mutual fund manager.

“It’s likely the news of home price stabilization will turn out to be the mother of all head fakes,” Tilson said. He spoke to a group of financial analysts in Boston last week.

Real estate prices are fundamentally dependent on supply and demand, and Tilson’s argument rests on several indicators that point to supply far outstripping demand in the near term.

The three-month run-up from April-June was not unusual, he said, because housing prices almost always rise in the spring; that is the peak selling season and the time of highest demand.

Shining light on the shadow inventory

More importantly, a glut of “shadow inventory” is not reflected in the published statistics, and it will push housing prices lower in the coming months, Tilson said.

Shortly after taking office, the Obama administration and several states imposed moratoriums on foreclosures. This has caused a temporary and artificial spike in the inventory of bank-owned homes facing foreclosure, and once those houses come on the market prices will drop.

At the end of July, 4.1 million existing homes remained unsold, equivalent to 9.4 months of supply, still way above historically “normal” inventory levels of about 5 months supply. There were another 1.2 million homes at least 90 days in default, on which the foreclosure process had not yet begun. And there were another 1.5 million homes somewhere in the foreclosure process.

Banks, it seems, would rather have someone living in the home than face the uncertainty of trying to sell a vacant house.

Add those numbers up, and there is an additional 15 months of shadow inventory not reflected in the official numbers, Tilson said.

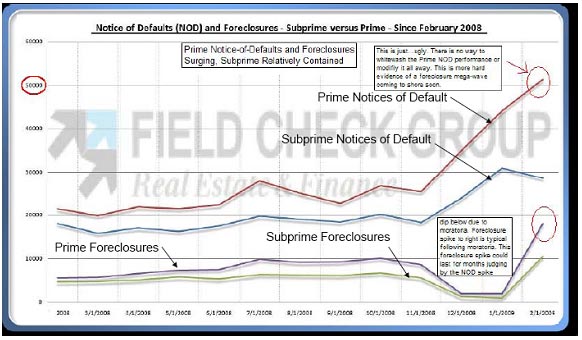

The graph below compares the acceleration of defaults (upper two lines) to the relatively steady pace of foreclosures, including the dip earlier this year caused by the government moratorium. The difference between the two represents the shadow inventory.

While inventory has grown, transactions in the housing market have bifurcated. Most of the activity has taken place at the low end of the market, particularly among distressed properties. The high end of the market has “frozen up.” For example, California has 15 months of inventory for homes priced at more than a million dollars.

Tilson expects housing prices will drop at least another 5-10%, putting prices back on historical trend lines, before stabilizing sometime in 2010. But Tilson also warned that prices could overshoot to the downside, something that has often happened when major asset bubbles burst.

An $8,000 first-time homebuyer tax credit has buoyed home prices, Tilson said, but it is due to expire at the end of November. If it is not extended, prices will be pushed lower.

A bulging pipeline

The most powerful downward pressure on prices will come from the pipeline of defaults and foreclosures, which Tilson said is larger now than at any time in history.

He spoke of several types of loans that are coming through this pipeline.

The role of the Federal Hosing Authority (FHA) in guaranteeing mortgages has grown significantly since 2005, when it had a 2% market share. Now the FHA accounts for 23% of all mortgages, but its standards resemble those of subprime lenders. It allows loans with 3.5% down for borrowers with FICA scores 600 (subprime) and 10% down for 500 FICA scores (deep subprime).

“Thousands of shady subprime mortgage lenders rebranded themselves and are now doing FHA-backed business,” Tilson said. “Approved FHA lenders grew from just over 9,600 at the end of FY07 to nearly 14,000 today, according to the Department of Housing and Urban Development (HUD).”

The FHA has poor systems, poor controls, and is undercapitalized, according to Tilson. He expects that it will need to be bailed out by Congress, which could lead to tighter lending standards and further downward pressure on prices.

At the onset of the financial crisis, there were $1.5 trillion outstanding subprime loans. Defaults on these have subsided, but they are persisting for other types of loans. Thanks to job losses and instability in the economy, default rates on the $4.5 trillion in currently outstanding prime loans (mostly guaranteed by the GSEs) began to surge in early 2008 and continue to rise. The same is true for jumbo prime loans, second lien loans, and home equity lines of credit (HELOCs), many of which remain on banks’ books. Then there are loans outside the housing sector – the largest group being the $3.5 trillion in outstanding commercial real estate loans – for which Tilson said default rates are still increasing.

The ominous pace of prime and Alt-A defaults, compared to the stabilization of subprime defaults, is shown in the graph below:

Although prime and Alt-A loans will not suffer the extreme default rates seen among the subprime loans, each is much larger in size than the subprime market.

And the bad news does not end there.

There are approximately $2.4 trillion worth of Alt-A mortgages currently outstanding, almost twice the value of the subprime market. (Alt-A loans are made to borrowers with credit scores between those of subprime and prime borrowers, with lending standards between those two groups.)

Tilson showed the projected reset dates for a representative sample of the Alt-A universe:

Fortunately, most of these loans will reset to rates not much higher than their current rates, since short-term interest rates are currently very low. Most are tied to the 6- or 12-month LIBOR, and if that spikes over the next several years, it could trigger a landslide of defaults.

Prospects for the future

The wildcard in forecasting defaults is predicting the behavior of the nearly one-in-four homeowners with mortgages who are now “underwater” – they owe more than their house is worth. Tilson said there is no historical precedent for this situation, and no way to predict how many homeowners will mail in their keys when their house’s value declines.

Indeed, the stigma of defaulting and walking away from one’s home is abating, as millions of Americans have already chosen this path.

Tilson’s “best guess” is that his projection of a 5-10% decline in house prices will translate to a similar 5-10% increase in defaults.

Loan modification programs are not working. Once a loan has been modified, there is a still 50% chance that a borrower will be 60 or more days in default within the next year, based on loan modification statistics from the last year. The reason, according to Tilson, is that those borrowers are too deeply underwater to have an incentive to keep payments current.

All this bad news has not tainted Tilson’s view of the market. His is still “net long” in his hedge fund, but he has been adding to his short positions. At a macro level, he is “very bullish on American” and has added to his positions in blue-chip stocks and a few selected turnaround situations.

“People really, really want this to be over,” Tilson said of the collapse in the housing market and of the much larger financial crisis. “But this was an enormous, global bubble, and those bubbles take a long time to deflate.”

Read more articles by Robert Huebscher