If you think there is a greater than 9% chance that we will be in a recession in the next 12 months, you should avoid high-yield bonds. But if you think the economy is recovering and interest rates will rise soon, you should invest in the lowest-quality bonds in the market.

If you think there is a greater than 9% chance that we will be in a recession in the next 12 months, you should avoid high-yield bonds. But if you think the economy is recovering and interest rates will rise soon, you should invest in the lowest-quality bonds in the market.

According to fixed income expert Marty Fridson, there are risks and opportunities in the high-yield market that you should consider whether you’re a bull, a bear, a hawk or a dove.

Fridson is the chief investment officer at Lehmann Livian Fridson Advisors LLC and a widely respected fixed income analyst. He spoke on May 9 at the 69th CFA Institute Annual Conference in Montréal on high-yield investment strategies.

I will review his analysis of default rates, his strategy for investors expecting rising rates and his explanation for the recent deterioration in covenant quality.

Is 2016 the beginning of a multiyear default-rate surge?

According to Fridson, “Default rates in 2016 are definitely higher,” but whether this is the beginning of a multiyear default-rate surge depends on whether you think we are heading into a recession.

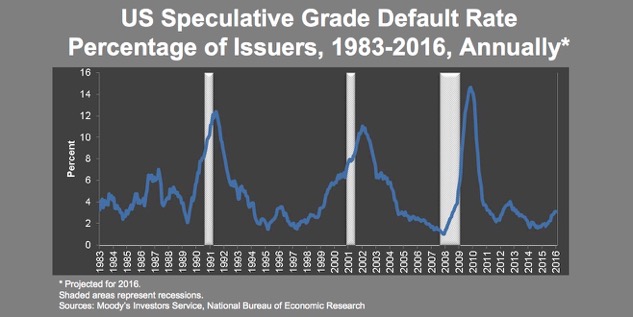

Fridson explained that default rate surges typically follow the pattern of economic cycles, and to illustrate his point he presented the graph below.

The data shows that surges in U.S. speculative-grade default rates throughout the last 33 years have typically coincided with economic recessions. But Fridson did not just present the graph to show a general trend; he introduced it so he could point out an important subtlety.

He stated, “The key point that comes out of this graph is that there was a mini-surge in 1985-1986 that did not continue to that low double-digit peak. So the question is if we are in that kind of period again. Because that was driven by a drop in oil prices.”

He explained that in 1985-1986 there was a mini-surge driven by defaults in the oil and gas industry, but that those defaults weren’t part of the overall business cycle. The economy continued to perform well even though the energy sector was faltering, so the default rates receded and didn’t rise again until the recession in 1990-1991.

“Whether this is just a temporary surge related to energy or a more general increase is really related to the question of whether we’re going to be in a recession,” Fridson said.

One way to answer this question is to look at the average length of economic expansions, according to Fridson. He explained that the average length of the last three cycles was 95 months, and the longest of the last three cycles was 120 months. Therefore, because it will have been 102 months from the end of the last recession to December 2017, he concluded that there is some historical evidence that supports expecting a recession in 2017.

Fridson said, “The former Treasury Secretary Lawrence Summers recently stated that he saw at least a 50% possibility of a recession by 2018,” and that part of this view is based on the fact that expansions don’t go on forever.

But high-yield investors should consider whether the market is priced according to this bearish outlook.

Fridson deduced the high-yield market’s estimate of the probability that we will enter a recession in the next 12-months, excluding data from the energy and metals because the commodities industries are already in recession.

According to his calculations, the high-yield market estimates the probability of recession as just 9% over a 12-month horizon. “If you think that the probability is substantially higher than that, it would be an argument for underweighting high-yield currently,” Fridson said.

What default rate does the high-yield market expect?

Fridson continued his discussion of default rates, but shifted to explain a fixed income investment strategy based on the market’s perception of the current default rate. He explained that sometimes the default rate the market is priced to expect is out of line, and that this typically happens during bad periods marked by panics and outflows.

When this happens, Fridson claimed, there are good opportunities for investors because “you get bonds trading at a level that indicates a high probability of default that really doesn’t belong there... so you get an overly pessimistic view reflected in the market.”

However, he cautioned investors about the pitfalls of turning to conventional metrics, like calculating the spread versus Treasury bonds minus an illiquidity premium, in order to gauge the market’s projected default rate when trying to identify opportunities.

Instead, Fridson prefers using a metric for the market-implied default loss rate that is based on the notion that defaults occur in the bonds that are trading at distressed levels. He calculates this by comparing the distress ratio to the distressed default rate, thereby accounting for the effects of economic cycles.

According to his analysis, as of May 8, “The high-yield universe is currently projecting a 5.8% default rate for the next 12-months, which is very close to Moody’s forecast of 5.6%.”

He explained that if we see divergence between these two metrics, and the market’s projected default rate is a percentage point or more above Moody’s forecast, it will likely be a good time to own distressed bonds because some assets will be unfairly priced.

For example, in the midst of a recession, a large number of bonds are at distressed levels, and this is sometimes because funds owning them have suffered huge outflows due to hard economic times (not because they have poor business practices). When this is the case, the distressed bonds are not necessarily likely to default in the next 12 months. According to Fridson, historical evidence shows that when the distress ratio rises, default risk actually declines. In this scenario, if the market thinks the default risk is higher than it actually is, there may be investment opportunities in high yield where investors can be overcompensated for the risk. Comparing Fridson’s metric to Moody’s forecast can be a useful tool to identify this type of opportunity.

Conversely, Fridson claimed that if the market’s expected default rate moves to a percentage point below Moody’s forecast, it is likely a bad time to invest because high-yield bonds will be priced too high.

Therefore, investors should keep an eye on movements in the market’s expectation of the default rate in coming months.

Positioning for rising interest rates

Although Fridson did not forecast his expectations for interest rates, he did discuss strategies that investors can use if rates rise. In doing so, Fridson made two claims that challenged the conventional wisdom of fixed income investors.

First, he argued that fixed income investors should not buy short-dated high-yield bonds under the assumption that they are less sensitive to rising interest rates.

“High yield bonds are a hybrid of interest rate instruments and equities, and they behave that way. As a result of that, they don’t perform the same way higher quality bonds do,” Fridson said.

His claims were based on an analysis of returns from 1996-2015 in which he showed that short-dated high-yield issues did not outperform during episodes of rising rates. Based on these findings, he recommended that high-yield investors avoid maturity-based strategies.

Second, Fridson claimed that positioning by quality is the best strategy because the lowest-quality bonds have historically outperformed during episodes of rising rates.

His claim that rising interest rates are good for highly leveraged companies, which are the lowest rated issues, is counterintuitive. “But keep in mind that high-yield bond companies do not have all of their debt in short maturities with floating rates,” Fridson said, “so if rates start to rise, the initial impact is nothing.” He argued that it would take years for the effect of rising rates to flow through their income statements.

Fridson also reasoned that rates rise because the economy is doing well and there is increased demand for credit. Therefore, he argued, as the economy strengthens the default risk declines, and the resulting decline in risk premiums benefits the riskiest companies the most.

“That, I think, is the best way to play a rising rate environment,” Fridson said.

Will covenant quality rebound as the credit cycle matures?

Fridson concluded his presentation by discussing changes in covenant quality throughout the last five years. He pointed to Moody’s covenant-quality index and explained that the series shows there’s been a steady decline in the strength of covenants.

He claimed that this is a result of issuers having the upper hand, and he believes the long-term trend will continue to be degraded quality.

According to Fridson, this is because of the dynamics between the issuers and the underwriters. He explained that underwriters are competing for the business of the same institutional customers. He argued that they can only to differentiate themselves by saying, “We have come up with a new gimmick in the covenants that people won’t figure out right away and realize that we’ve left a loophole for you to take advantage of at a later point, so this gives you more value.”

Unfortunately, he added, investors are unlikely to push back against covenant-quality deterioration because they are very fragmented and are unable to challenge the concentrated group of investment banks responsible for the majority of the deals.

Marianne Brunet is a financial markets analyst with Advisor Perspective

Read more articles by Marianne Brunet

If you think there is a greater than 9% chance that we will be in a recession in the next 12 months, you should avoid high-yield bonds. But if you think the economy is recovering and interest rates will rise soon, you should invest in the lowest-quality bonds in the market.

If you think there is a greater than 9% chance that we will be in a recession in the next 12 months, you should avoid high-yield bonds. But if you think the economy is recovering and interest rates will rise soon, you should invest in the lowest-quality bonds in the market.