Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

This is a follow-up to my article of May 29, 2017 encouraging financial advisors to use the actuarial budget benchmark (ABB) to develop sustainable spending plans (SSPs) to better serve and retain your clients. This article will discuss:

- “Real-world” situations frequently ignored by retirement researchers and other retirement experts when illustrating or testing proposed distribution/spending approaches;

- Budgeting/planning limitations of sustainable withdrawal plans (SWPs) and Monte Carlo modeling currently in use; and

- How the ABB can be used together with our recommended smoothing algorithm to help you develop more robust SSPs for your clients that will handle most situations. I call this SSP the “smoothed ABB.”

I also present an example to demonstrate how the smoothed ABB works over a 10-year projection period for a hypothetical couple. Finally, I encourage advisors to experiment with the smoothed ABB to see if you should add it to your consulting toolkit.

Background

I discussed how the ABB is calculated in our May 29, 2017 article. Briefly, it involves an annual mark-to-market calculation (using assumptions inherent in inflation-adjusted annuity pricing) to solve for the current and present value of future spending budgets that balances the present value of clients’ assets with the present value of their spending liabilities. Refer to that article for additional details.

Unfortunately, good budgeting is not that simple

Developing a reasonable spending budget is not as simple as we are sometimes led to believe. Real-world complications frequently ignored (or assumed away) by retirement researchers and experts include:

- Many individuals are part of a couple and plan as a couple;

- The individuals in a couple may not be the same age and may not retire at the same time;

- Income sources before retirement don’t always stop at the same time and income sources after retirement don’t always start (or stop) at the same time;

- Couples generally don’t live the same period of time and income needs generally change upon the first death within the couple;

- Future expenses are generally not the same each year. Some future expenses may be non-recurring, some may be recurring, some may increase at a rate higher than general inflation and some at a lower rate. This is a significant, frequently-ignored, issue that will be discussed in more detail below;

- Some income sources in retirement may be paid in fixed dollars and some in inflation-adjusted dollars;

- Individuals will generally not spend exactly their spending budget each year; and

- Individuals experience one pattern of future investment returns, not an average of 10,000 patterns generated for Monte Carlo modeling based on historical returns.

Ignoring these complications can lead to ineffective client budgets and financial plans.

Budget/planning limitations of SWPs and Monte Carlo modeling

Because SWPs don’t coordinate with other sources of income and are simply drawdown algorithms, their use is frequently inconsistent with a couple’s (or single individual’s) retirement goals in these real-world situations. Since SSPs focus on spending, and not withdrawals from accumulated savings, they can be tailored to address these real-world situations to better meet retirement spending objectives. And while the SPP I discuss below is more complicated than most simple SWPs, you can use my spreadsheets to perform the annual present value calculations necessary to make it work and obtain a better result for your client.

Monte Carlo models frequently used by financial advisors are great tools for developing probabilities of certain outcomes, but these models are not necessarily effective in developing a current-year spending budget or for determining when that budget should be revised. A Monte Carlo model will typically inform a client that if she invests her assets in a certain way, she has a 90% probability of being able to spend $X per year for the rest of her life. The model generally doesn’t separate recurring and non-recurring spending and it doesn’t really give your client a plan of action if her assets decrease by 30% in one year (or increase by 30%). The model results imply that, irrespective of actual investment experience, your client should stay the course with respect to her investment strategy and keep spending $X per year come hell or high water (and not worry about the 10% failure probability). Thus, it is more of an “implied plan.” This is a potential shortcoming for many Monte Carlo models. Michael Kitces addressed this shortcoming in his post of December 7, 2015, Is Financial Planning Software Incapable of Formulating an Actual Financial Plan, when he wrote,

… virtually no financial plan today actually constitutes a real “plan” for anything. After all, the whole point of planning is to formulate the strategy of how to handle a range of possible future scenarios. If A happens, then we’ll do B. If C happens, we’ll do D instead. Yet financial plans today, and the financial planning software that supports the process, is incapable of illustrating such scenarios and the appropriate responses! Answering a simple planning question like “how much do the markets have to decline before I need to cut spending in retirement, and how much would I need to adjust my spending to get back on track” cannot be easily answered with any financial planning software available today!

Planning for non-recurring expenses

Most SWPs and Monte Carlo models focus exclusively on recurring expenses in retirement. A more robust SSP should separately plan for future expenses that are non-recurring in nature as well as those expected to be recurring from year-to-year. For example, if a client’s mortgage payments are expected to cease shortly after retirement, it makes little sense to fund that same level of expense over the retiree’s entire remaining lifetime. There are many possible expenses that fall into this category, including pre-Medicare medical costs, long-term care costs, desired amounts to be passed to heirs, special dental costs, home-repairs, new cars, travel plans, etc. A financial advisor should discuss these separate costs with clients (and whether they will be front-loaded or back-loaded) before pulling out their Monte Carlo model that predicts a 90% probability of being able to spend a flat $X each year in real dollars.

Using the smoothed ABB

Because it involves a mark-to-market calculation of client assets and spending liabilities, the ABB can produce volatile results from year-to-year due to investment fluctuations. Those undesirable fluctuations can be mitigated by smoothing the results. The smoothing algorithm that I recommend involves:

- taking the recurring spending budget amount from the previous year;

- increasing that amount by the desired increase in spending budget for the previous year (generally the actual increase in general inflation for the previous year); and

- testing that the resulting amount (the preliminary recurring spending budget) is not more than 110% of, and not less than 90% of, that years’ ABB for recurring expenses.

- If the preliminary value falls within this corridor, that value becomes the recurring spending budget for the current year. If the preliminary value falls above or below the corridor limit, the applicable corridor value is used as the current year’s budget.

In addition to being able to handle most situations, using the smoothed ABB is consistent with the following client goals:

- Maximizing current levels of spending without jeopardizing ability to meet future anticipated expense needs;

- Efficiently matching spending patterns with patterns of expected expenses;

- Not spending too much and not spending too little;

- Avoiding year to year spending volatility;

- Having spending flexibility; and

- Leaving approximately desired amounts to heirs at death.

Example: 10-year projection of spending budgets

To illustrate how the smoothed ABB works to achieve these general client goals, I performed a 10-year projection of spending budgets for a hypothetical couple, Bob and Sue. This example is fairly complicated because it makes valuation assumptions in calculating the ABB in each year of the 10-year projection period and different projection assumptions with respect to actual experience during the next 10 years. In order to reduce the level of eye-glazing experienced by readers, I have moved much of the discussion about those assumptions to the appendix.

Data/goals

Bob is currently age 65 and Sue is age 58. Both have fully retired with no plans for part-time employment. Based on a future inflation assumption of 2% per annum, their financial advisor has projected Bob’s age-70 Social Security benefit to be $31,480 per annum and Sue’s to be $28,300 per annum. Both of them plan to defer their benefits until age 70. Bill has a company-sponsored pension benefit that currently pays him a fixed amount of $20,000 annually for the rest of his life with no benefit upon his death to Sue. Sue expects to receive a single-life annual pension benefit of $15,000 per annum when she commences her benefit at age 65.

Bob and Sue currently have $1,000,000 in assets, invested fairly aggressively.

Bob and Sue have four years remaining on their home mortgage. They estimate this cost to be a fixed amount of $20,000 per year for the next four years. Additionally, they would like to travel over the next 15 years and have estimated that they might spend an extra annual amount of $15,000 (in real dollars) for these non-recurring travel expenses. Finally, since Sue is not eligible for Medicare, they have estimated that her extra cost for comparable medical coverage for the next five years will be about $5,000 per annum.

Bob and Sue have determined that the equity in their home should be sufficient to cover their anticipated long-term care costs. They have also set aside sufficient separate reserves for unexpected expenses and burial expenses. They have no desire to leave a large estate to their children. While I made these assumptions to simplify the example, these “complications” can certainly be addressed in the ABB, if necessary.

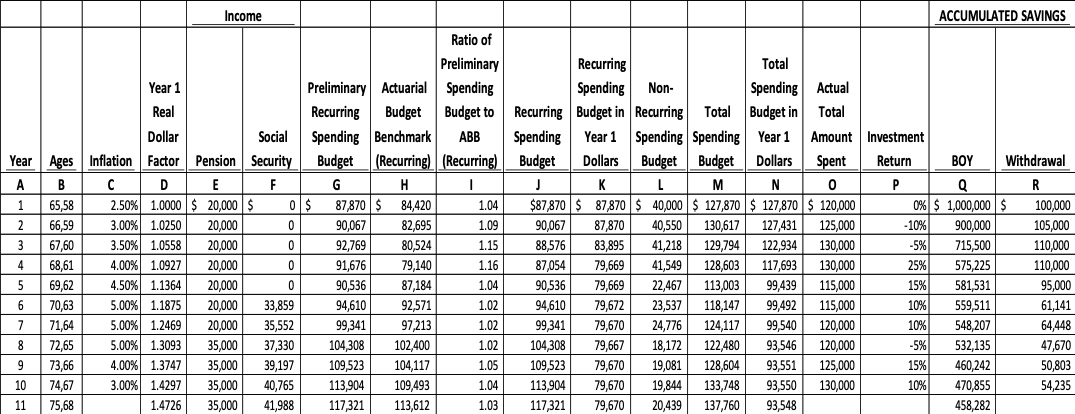

Ten-Year Spending Projection for Bob and Sue

Results

The above chart shows that:

- While the ABB for recurring expenses (in Column H) may bounce around a bit from year-to-year as a result of fluctuations in projected investment returns and inflation, Bob and Sue’s recurring spending budget measured in real dollars (in Column K) is expected to decrease somewhat initially (because the ratio of their preliminary recurring spending to the ABB exceeds 110% in years 3 and 4) but remain constant thereafter under these projection assumptions. This result could be different under different projected investment and inflation experience, but the recommended smoothing algorithm is reasonably effective in avoiding year to year spending budget volatility, while at the same time keeping Bob and Sue’s recurring spending on track.

- By treating their home mortgage, desired travel expenses and Sue’s pre-Medicare extra medical expenses as non-recurring expenses, Bob and Sue have maximized their total expense budget without jeopardizing their ability to meet future expenses. The total spending budget in year 1 dollars in column N shows that they have “front-loaded” their total spending budget to cover these non-recurring expenses without unnecessarily increasing their expected future recurring expense budgets.

- They have flexibility to deviate from their annual spending budget. Column O shows that, like most real-world couples, they are sometimes going to spend more than their spending budget and sometimes less.

- Withdrawals from accumulated savings in column R are equal to the total amount actually spent by Bob and Sue in column O minus their income in columns E and F. Contrary to results obtained using SWPs, there is nothing “systematic” about Bob and Sue’s withdrawals from savings under this SSP.

- Under these projection assumptions, the smoothed ABB produced results generally consistent with Bob and Sue’s spending goals (including their goal to travel while they can). However, they may wish to look at projections involving longer (or more pronounced) investment boom and bust cycles to further stress test the smoothed ABB.

Conclusion

Developing a reasonable spending budget is not a simple task. While the calculations necessary to develop a reasonable budget in those circumstances may be more complicated than SWP calculations, the process is simplified by using the actuarial budget calculators (ABC) and present value calculator (PVC) spreadsheets available on my website to calculate the necessary present values and ABBs.

I encourage advisors to:

- Use my workbooks (or improve them) to develop SSPs for your clients. In doing so, I recommend that you separately budget for your client’s non-recurring and recurring expenses.

- Model your client’s future recurring and non-recurring spending budgets under reasonable projection assumptions.

- Experiment with the smoothed ABB to see if it just might do a better job of developing spending budgets for your clients (and therefore increase your bottom line). If you don’t like certain aspects of the smoothed ABB (for example, the smoothing algorithm), make improvements to it.

- Consider using the more robust ABB (smoothed or not) as the spending algorithm in your Monte Carlo models, or consider other ways in which the ABB can be incorporated in your consulting toolkit.

Ken Steiner is a retired actuary with a website entitled, "How Much Can I Afford to Spend in Retirement."

Appendix

Example projection assumptions

Assumed future rates of inflation for projection purposes are shown in Column C of the chart below and future rates of investment return are shown in Column P. I have selected a pattern of investment returns involving early investment losses followed by mostly investment gains (as might be expected for current retirees given today’s market conditions). Over the 10-year period, the average investment return is about 6% per annum, or about 2% per annum after inflation.

I assume that neither Bob nor Sue will die during the 10-year projection period, and I assumed they will both stick with their intentions to commence their Social Security benefits at age 70 and their pension benefits at age 65. I have increased the initial Social Security benefit estimates to reflect projected increases in inflation. I assumed their travel expenses would increase each year with inflation and Sue’s extra medical costs would increase with inflation plus 1% per year.

Example valuation assumptions/ABB calculations

I have used the Actuarial Budget Calculator (ABC) for Retired Couples to calculate Bob and Sue’s current year spending budget and their ABB for the current year and each of the next ten years. For purposes of determining their initial year preliminary spending budget, Bob and Sue decided to use the current default assumptions (4% investment return/2% inflation/2% future spending budget increases/lifetime planning period based on healthy, non-smoker with a 25% probability of survival), except they believe their current investment mix will produce at least a 3% real rate of return over their expected retirement rather than the default assumption of 2%. To calculate their current and future projected ABBs, I assumed that the current default assumptions will be increased to 4.5%/2.5%/2.5% in year two and remain unchanged during the remainder of the projection period. I also assumed Bob and Sue are comfortable assuming their recurring expenses in total will increase with general inflation in future years and decrease by 33% upon the first death within the couple. Finally, I used the present value calculator workbook to calculate the present values at the beginning of each year of the 10-year projection period of Bob and Sue’s future mortgage payments, Sue’s extra medical costs, travel expenses and estimated future Social Security survivor benefits payable to Sue upon Bob’s expected earlier demise.

Read more articles by Ken Steiner