Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Most private equity funds set their ”hurdle rate,” or preferred return, at around 8%, though this may vary depending on the fund’s strategy. This means the fund manager must generate an annualized net return of at least 8% for investors before the manager can share in any of the profits.

In an asset class where investors typically expect net performance of around 15%-20%, the preferred return is a critical tool to ensure that managers achieve a prespecified baseline return before they can collect incentive compensation.

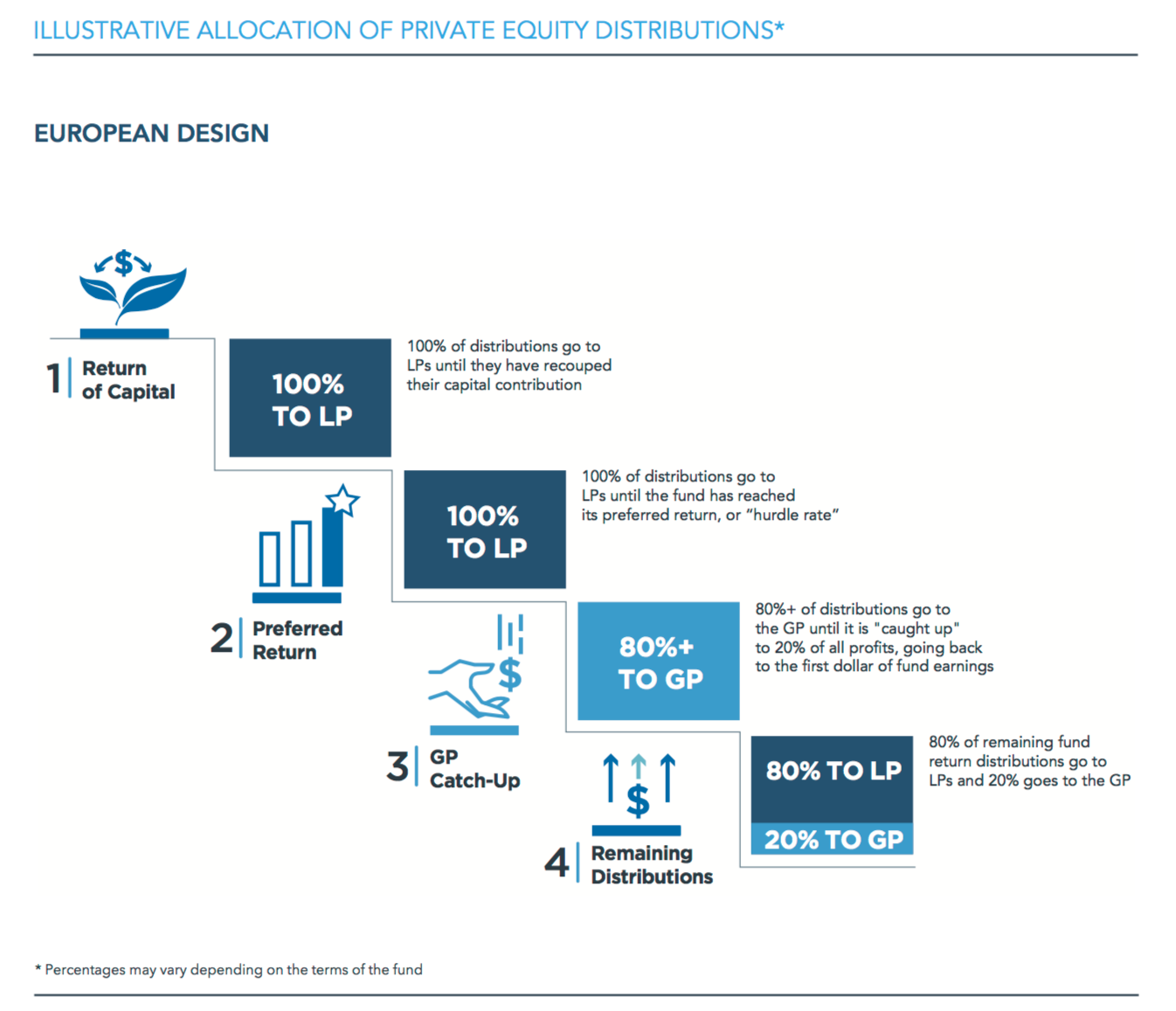

However, it is important for investors to properly assess a private equity fund’s waterfall, or the allocation of distributions between the general partner (GP) and limited partners (LPs), in order to ensure proper alignment of interests. There are four primary components to a distribution waterfall:

-

Return of capital: 100% of a fund’s proceeds are distributed to investors until they have received an amount equal to the total amount they have invested.

-

Preferred return: Investors continue to receive 100% of fund proceeds until the fund has achieved its preferred return, or hurdle rate, as defined in the fund’s offering documents. While the typical preferred return in private equity is 8%, it is often 6% in the case of private credit funds, which usually have lower target returns than buyout funds.

-

GP catch-up: Once a fund has returned all contributions to investors and reached its preferred return, the GP is then able to begin collecting carried interest, which is calculated by going back to the first dollar of profits generated by the fund. In order to recoup the GP’s share of returns accrued prior to reaching the hurdle rate, most managers include a GP catch-up provision, which allows a manager to retain most of a fund’s profits (often 80%) until it has received its stated share of the gains.

-

Remaining distributions: After the manager is "caught-up" and has received its incentive for fund returns beyond the hurdle rate, all remaining proceeds are then allocated between LPs and the GP at the specified rate (typically 80%/20%, respectively).

While these four components are relatively standard across most private equity funds, there are variations on how a GP may implement its waterfall. The most common variations are the European and American waterfalls. The designation of European versus American refers to the way that the waterfall is structured, not the geographical location of the manager. Under a European waterfall structure (described above) carried interest is calculated at the fund-level across all deals. In this situation, the GP does not begin to take carried interest until the fund has returned all LP contributions across all deals, and delivered the preferred return.

By contrast, an American waterfall is calculated on a deal-by-deal basis, where GPs are compensated for each successful deal. This often allows the GP to begin taking a share of the profits or carried interest earlier in the life of a fund. In some cases, this can alter a GPs behavior, as collecting carry on a few large, successful deals early on may reduce their incentive to optimize performance later in a fund’s life. An American waterfall also can result in a GP receiving carried interest on a fund that is underperforming its hurdle rate, provided that there are individual deals that have outperformed the preferred return. Almost all funds that utilize an American waterfall include a “clawback” provision, which allows investors to recoup the carried interest at the end of a fund’s life if the fund underperformed and the GP collected more than its share of the fund’s profits.

European waterfall: Performance is measured versus the hurdle rate at the fund level.

American waterfall: Performance is measured versus the hurdle rate on a deal by deal basis.

European waterfalls are more favorable for investors because they delay the payment of carried interest and prevent GPs from collecting incentive compensation on funds that underperform. Due to the somewhat complex nature of waterfalls, investors should carefully examine a fund’s terms to understand how carried interest is paid. It is important that the waterfall structure is designed to appropriately balance the needs of both the investor and the manager to maximize the alignment of interests between all parties involved. A well-designed waterfall can be a benefit for LPs, as it creates strong alignment and properly incentivizes the manager to optimize returns. When a fund is performing well, fund managers reap the benefits along with their investors.

Nick Veronis is co-founder and managing partner, and Dan Fletcher is assistant vice president, research and due diligence, iCapital Network, a New York-based alternative investment marketplace.

More Alternative Investments Topics >