The Federal Reserve’s asset purchase program, known as quantitative easing, has twice helped save the US economy — first during the financial crisis and then again with the Covid-19 pandemic. Its long-term viability depends on policymakers’ ability to shut it down when it’s no longer needed, without injecting unnecessary volatility into markets. That makes the next 12 months critically important.

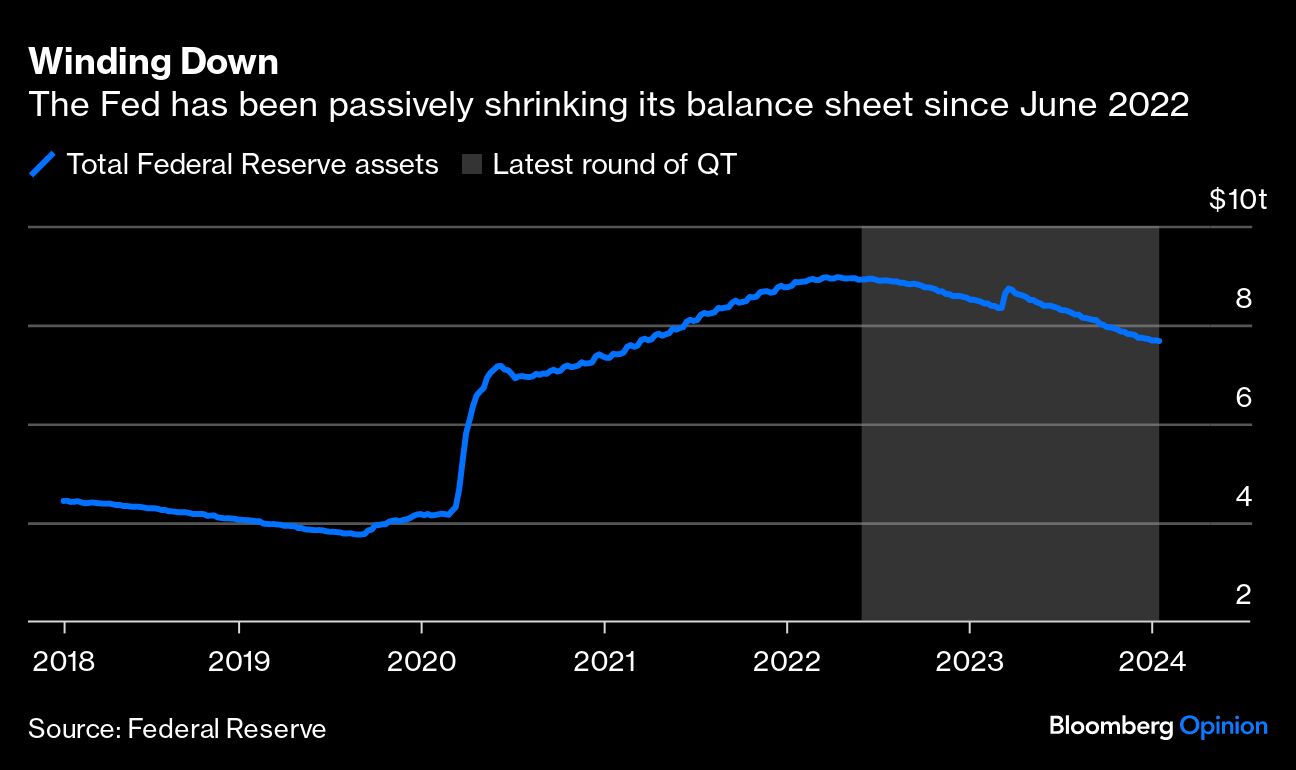

The Fed has been allowing as much as $60 billion in maturing Treasury securities and $35 billion in mortgage-backed securities to roll off its balance sheet each month without reinvesting the proceeds, part of a broader process that started about 19 months ago. Such quantitative tightening has drained liquidity from the financial system — ostensibly the opposite of what was accomplished under QE — in the interest of “normalization.”

So far, the process has been going fine. Money markets — where the Cassandras tend to project most of their QT nightmares — have been functioning relatively well. For all the consternation about the increase in the secured overnight financing rate late last year, the blips proved small and short lived. Meanwhile, Treasury buyers have been able to absorb the increased government bond supply without major indigestion. And bank reserves have fallen some (as by design), but are still well above the levels that most policymakers consider “ample.”

Now, Fed policymakers must avoid pushing their luck, and announce a slowing of the pace of bond purchases in the coming months and a timeline for when they will end.

First, there’s no real upside to continuing to run QT at the current pace. A Bureau of Economic Analysis report later this week should show that inflation is close to the Fed’s 2% target. Yet even if you’re banking on a resurgence, most reasonable estimates suggest that QT has amounted to the equivalent of perhaps one or two rate increases worth of tightening at most. The Fed’s main tool in the inflation fight is — and will remain — its policy rate, and virtually no price stability is sacrificed by slowing the pace of QT sooner rather than later.

Second, there’s the lesson of 2019. Back then, the Fed had been “normalizing” its balance sheet for around two years — having the effect of removing bank reserves from the financial system — in a process that former Fed Chair Janet Yellen had said would be like “watching paint dry.” But in September 2019, the repo markets where financial institutions help fund themselves experienced major disruptions, forcing the Fed to intervene and stop the whole QT process with egg on its face.

That’s why there’s some palpable nervousness around QT a year and a half into the latest round of the program. Jamie Dimon recently told JPMorgan Chase & Co. investors that the Fed’s balance-sheet reduction policy was among the major downside risks he was monitoring. Bill Gross, the Pacific Investment Management Co. co-founder, used a Bloomberg Television appearance this week to urge the central bank to stop the process posthaste. And the minutes of the Fed’s Dec. 12-13 meeting showed that “several participants” thought it was appropriate to start discussing the potential conditions around an eventual slowdown in QT.

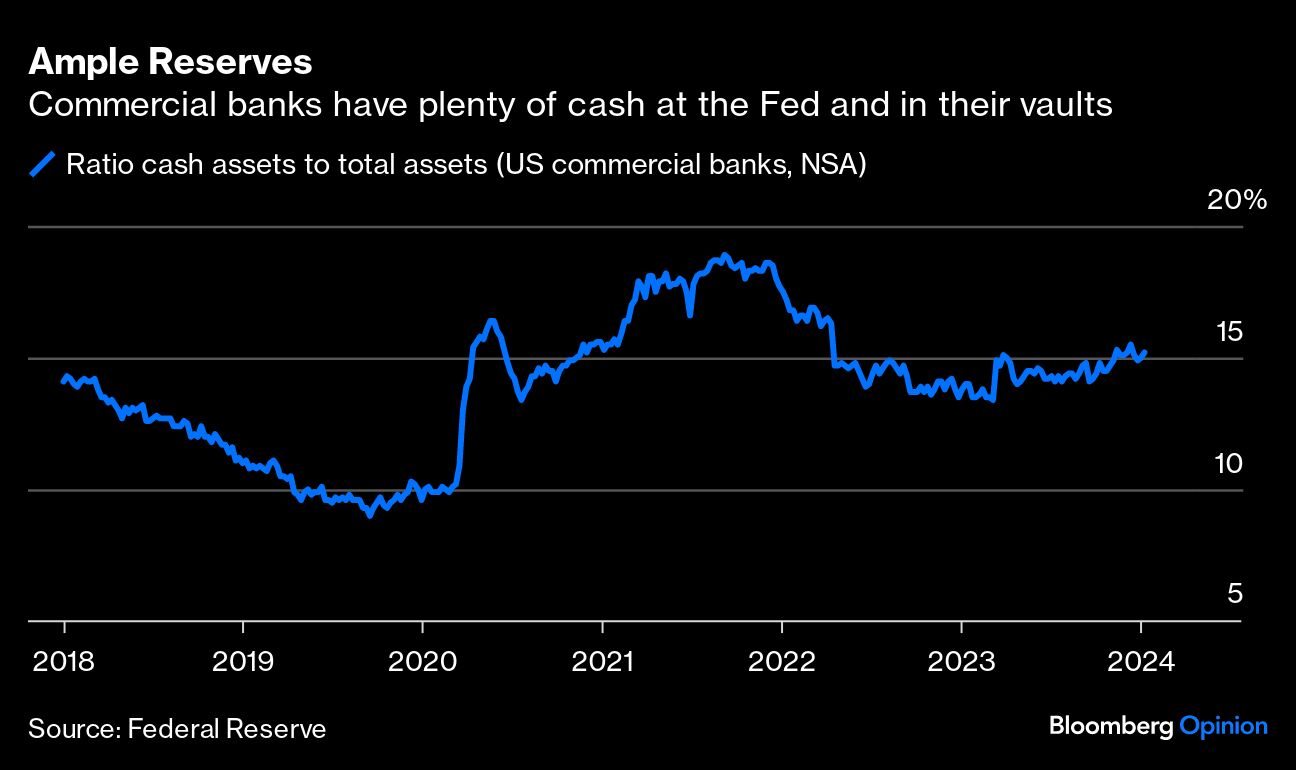

The Fed has committed to operating in an environment of “ample” reserves, and economists and Wall Street types have a bit of a parlor game around guessing what “ample” means. At the present $3.5 trillion (about 15% of total assets), reserves are above the 13% level that Federal Reserve Bank of New York President John Williams flagged as appropriate in a 2022 paper and well in excess of the much lower levels hit in 2019. In the current context, the incentives are almost entirely skewed toward overestimating what constitutes “ample.”

Before the financial crisis, the central bank regulated interest rates by controlling the levels of reserves through open market operations — a so-called corridor system — and too-high reserves were thought to blunt the Fed’s sway. Nowadays, the Fed offers competitive interest rates to banks and others to set a floor under market rates. It doesn’t need to destroy reserves.

Some people, of course, worry that the Fed’s balance sheet is a risk in and of itself. They point to the operating losses incurred at the Fed in the course of the latest inflation fight. Because it acquired longer-duration assets in the QE process, it locked in low rates of passive income and has been paying out high rates of interest to short-term borrowers. In the long run, this is needless handwringing. When rates were on the floor, the Fed remitted large sums of profit to Treasury to cut the deficit. Over the course of the business cycle, it should be expected to get back to that point. It needn’t make a mad dash to reduce the duration of its asset portfolio.

Policymakers like to think they’ve learned something quantitatively about how much liquidity they can safely drain from the system. But in reality, a number of post-mortems show there were a confluence of factors at play in 2019. The already-low reserve balances coupled with the effects of large outflows from corporate tax payments, as well as the settlement of $54 billion in Treasury debt. It was a perfect storm, and another may be hard to foresee.

The Fed has a bit of an extra cushion this time. Under normal circumstances, you’d expect QT to directly reduce bank reserves. When the Fed stops rolling over its bond holdings, banks theoretically step in and acquire more Treasury securities at auction, effectively emptying some of their reserves. But in recent years, money market funds had parked large quantities of money at a Fed reverse repo facility, creating a repository of pent-up demand for the securities that’s been absorbing some of the blow from recent QT. Trends in the so-called ON RRP suggest that the reverse repo buffer may be drained in a few months’ time, and that’s led some observers to prepare for another leg down in bank reserves.

Meanwhile, the Fed simply doesn’t need another blowup. It would risk the prospects of a rare soft-landing for the economy and enshrine the belief that all Fed inflation fights inevitably end in recessions and higher unemployment. It would also validate all those critics who say that QE is a genie that, once unleashed, can’t be put safely back in its bottle. In this cycle, the Fed has so far proved those naysayers wrong, ensuring asset purchases can remain a part of the central bankers’ toolkit for years to come. It’s not worth risking the alternative scenario.

A message from Advisor Perspectives and VettaFi: Advisors: You're Invited to Exchange! Nothing would be a better start to the new year than if you joined us at Exchange, an in-person conference for members of the financial services community in Miami, Florida on February 11-14th. For a limited time, we're offering you a free Exchange ticket!* Register today with code WINTER24 to claim your pass.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin