If I were to ask investors to name the best businesses in America, I suspect many would point to the Magnificent Seven, and understandably so. Technology giants such as Apple Inc., Microsoft Corp. and Alphabet Inc. are near monopolies that churn out reliably outsized profits.

Fewer, I’m guessing, would name the handful of companies that are arguably the Magnificent Seven’s biggest beneficiaries — businesses whose industry dominance and profitability are just as compelling and may prove to be more enduring.

I’m referring to the financial analytics companies behind the stock indexes and bond ratings featured daily in the financial press and followed widely by investors. The two most valuable and probably best known among them are S&P Global Inc. and Moody’s Corp., although MSCI Inc. and FTSE Russell, a subsidiary of London Stock Exchange Group Plc, are also noteworthy. (Bloomberg LP, the parent company of Bloomberg Opinion, also administers indexes through Bloomberg Index Services Ltd.)

These companies may not be as glamorous as Big Tech, but they have become as indispensable to the financial ecosystem as Apple is to smartphones or Alphabet to internet search.

It wasn’t always so. Analytics companies were once humble data providers to high-priced brokers and star fund managers slinging stocks and bonds. But when index funds began to take off in the 1990s, analytics providers increasingly stepped into the role of money managers, their indexes and bond ratings essentially dictating how trillions of dollars are invested. A generation ago, celebrity money managers were real people with proper names such as Peter Lynch and Bill Miller. These days, the brightest light on Wall Street is the S&P 500 Index.

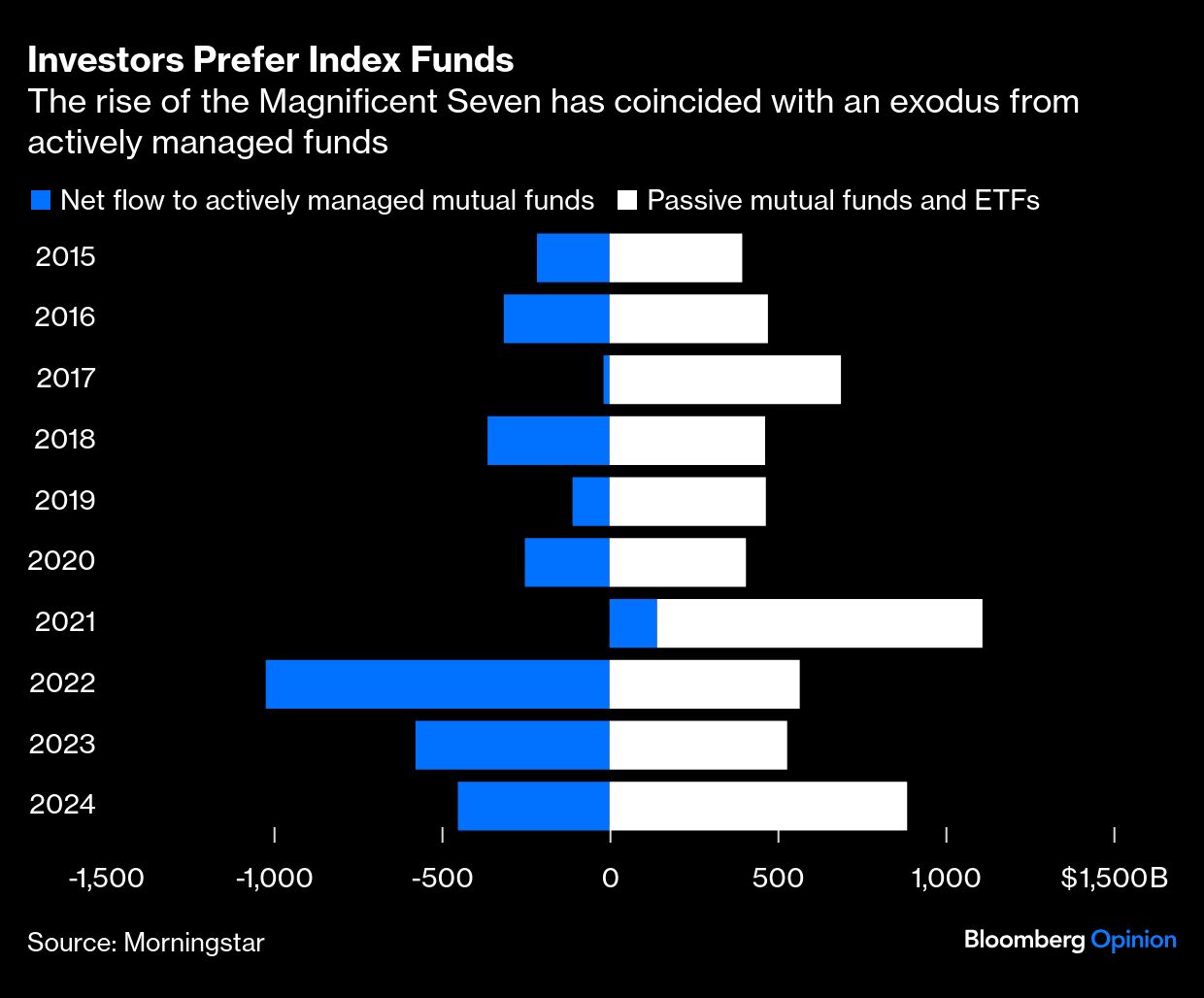

Every dollar that flowed to index funds swept prestige and profits from traditional Wall Street houses to data analysts, who receive a percentage of the money invested in funds that track their indexes. In 1993, stock and bond pickers oversaw 98% of the money invested in US-based mutual funds, according to Morningstar Inc. By 2014, their share of assets, which by then included exchange-traded funds, had dipped to 72%. Behind that move was a growing awareness among investors that most active managers can’t beat the indexes.

Then came the Magnificent Seven that made beating the market all but impossible. As the tech giants’ market value began to swell in the mid-2010s, so did their weighting in broad market indexes. They now comprise nearly a third of the S&P 500, meaning that as they go, so goes the market. Unfortunately for stock pickers, the Magnificent Seven have been among the best-performing stocks during the past decade. Any manager with less exposure to the tech titans than broad market indexes, which is practically all of them, had little hope of keeping up.

The market’s invincibility in recent years has bolstered investors’ impression that the true financial wizards are the data analysts at places like S&P and Moody’s, a reputation further enhanced by the dizzying array of indexes they have engineered to mimic traditional active strategies such as value, growth, quality and momentum. Since 2015, US investors have pulled $3.2 trillion from actively managed stock and bond mutual funds while handing close to $6 trillion to index mutual funds and ETFs. Active’s market share is now less than 50% and falling.

S&P and Moody’s have leveraged their growing influence to expand beyond indexes and bond ratings. They now provide market research, forecasts and risk analytics — once core offerings of Wall Street financial firms — to governments, companies, schools and practically anyone remotely adjacent to financial markets. Their stockpile of financial data may also give them a lead in the race to apply artificial intelligence and machine learning to financial markets. Their market value has swelled along with their offerings. S&P is valued at $167 billion, six times its market value 10 years ago. Moody’s, at $94 billion, is about five times more valuable than a decade ago.

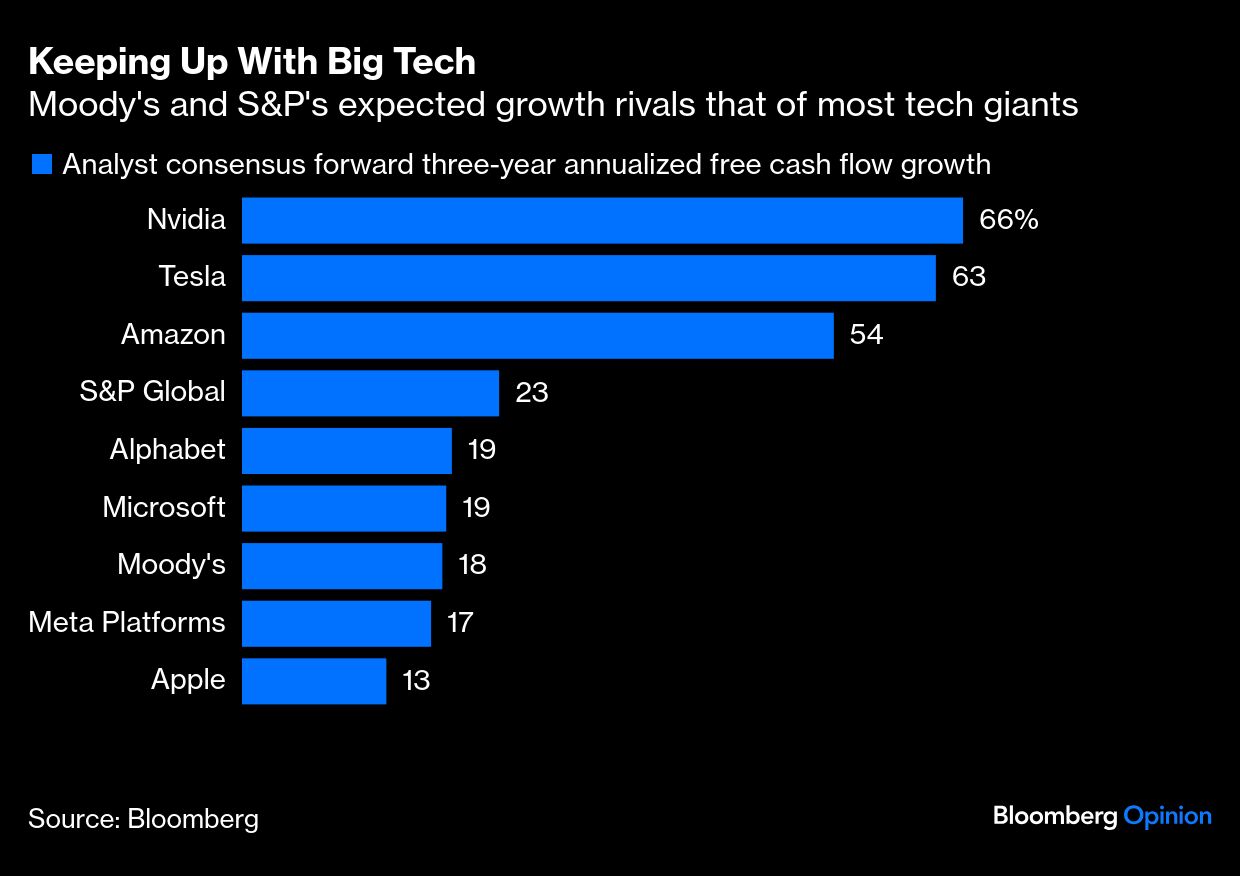

The brand and scale required to achieve their sweeping reach is a formidable moat. Analysts expect that S&P and Moody’s will grow free cash flow — the gold standard for many investors because cash flow is harder to fudge than earnings — as much or more than four of the Magnificent Seven over the next three years.

Nvidia Corp., Amazon.com Inc. and Tesla Inc. are expected to grow faster but also with more turbulence. The volatility of their estimated annual growth over the next three years is well higher than Moody’s or S&P’s. In Nvidia’s case, that volatility is five times that of S&P and 11 times that of Moody’s. Investors looking for the coveted combination of growth and stability can’t do much better than the two data analytics giants.

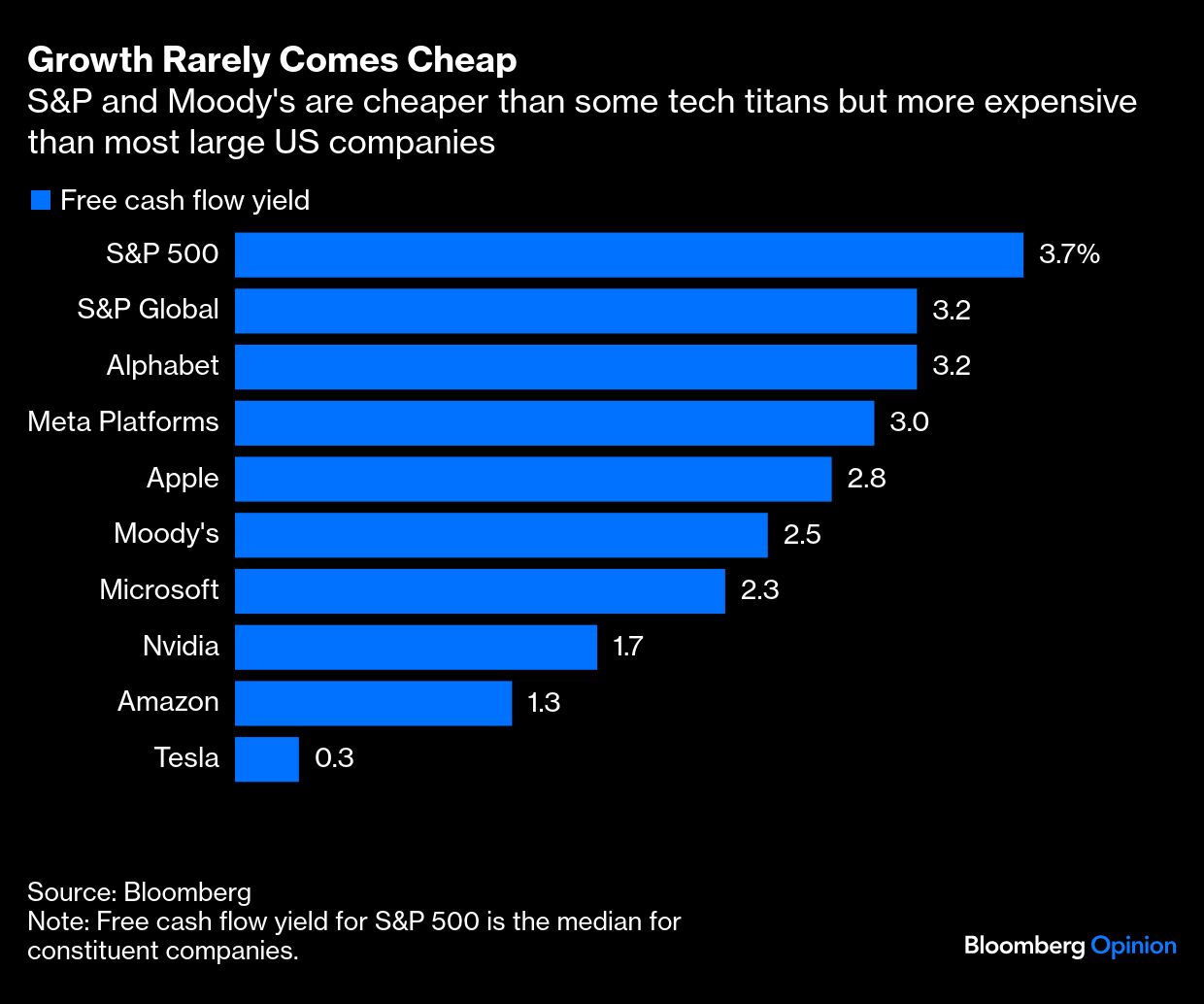

The kicker is that S&P and Moody’s are cheaper than most of the Magnificent Seven. S&P’s free cash flow yield — a ratio of free cash flow to price, where a higher yield signals a lower valuation — is comparable to that of Alphabet, the cheapest of the Magnificent Seven on that basis. Moody’s is more expensive but still cheaper than four of the Magnificent Seven.

That doesn’t mean S&P and Moody’s are a bargain. Their free cash flow yield is lower than the median yield for S&P 500 companies. A great company is only a great stock at the right price, and investors will have to decide if Moody’s and S&P’s expected growth justifies their lofty valuation. Warren Buffett, whose Berkshire Hathaway Inc. has owned Moody’s since its public debut in 2000, presumably still does.

Long after the current stable of tech highflyers has been replaced with the next generation of innovators, investors will still be buying index funds and consuming financial data — and data analytics companies will still be there to welcome the new tech titans.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Nir Kaissar