The world is a risky place, and high-yield debt spreads to safe US Treasury securities are close to historic levels of stinginess, signaling complacency in markets — at least on the surface. But legendary investor Howard Marks says that’s the wrong way to look at it and long-term investors should consider allocations to credit.

I am quite sympathetic to the handwringing about the policy environment. Investors are trying to absorb a bizarre — some might say stagflationary — mix of economic ideas from President Donald Trump, including 19th-century style tariffs and Silicon Valley “move fast and break things”-style government downsizing and layoffs. The former could provide a supply-side shock to prices at the same time that real economic growth may be wobbling. Consumers, businesses and investors don’t know what to think, and that uncertainty is serving as a drag on the economy.

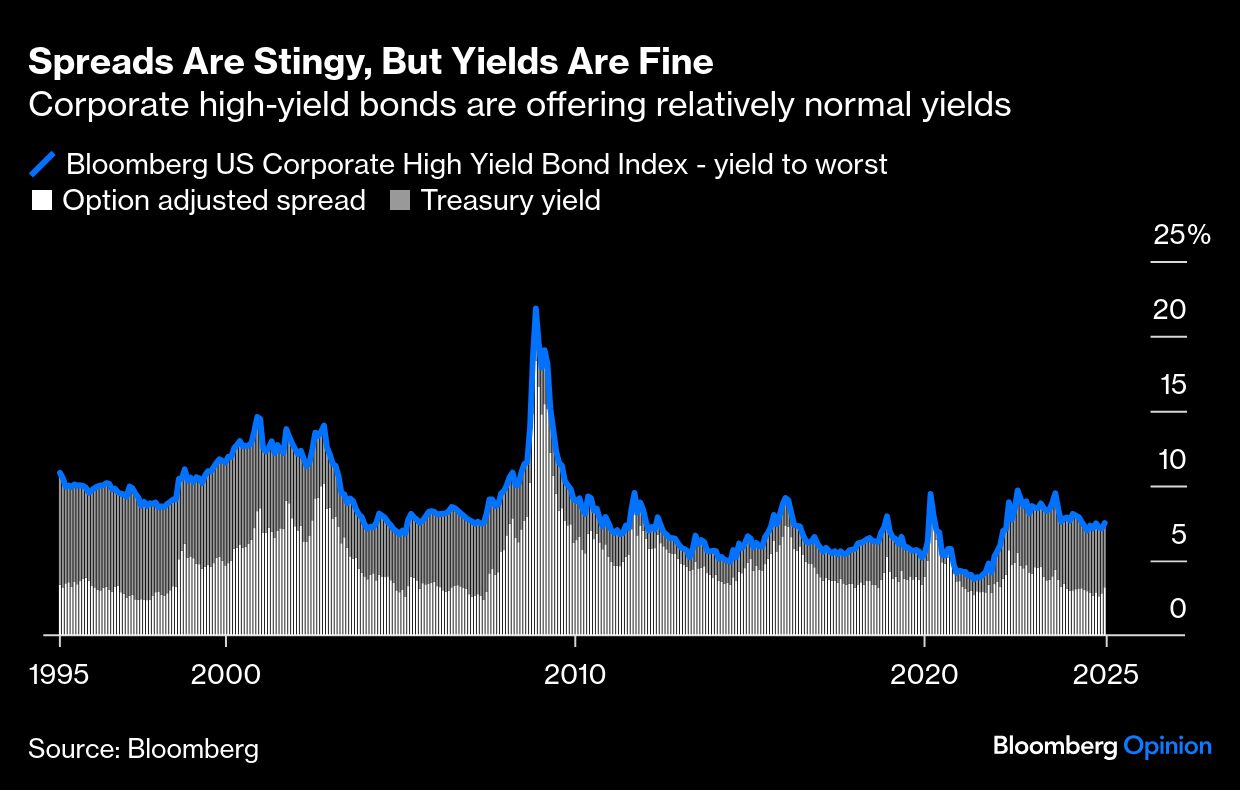

Meanwhile, even after widening about 53 basis points in the past month, the Bloomberg US Corporate High Yield Bond Index still yielded just about 314 basis points, or 3.14 percentage points, above government securities at the time of writing, a spread that’s in the most miserly 15th percentile. Outside of recent experience, the index has only seen spreads this narrow on rare occasions — on and off in the periods of 1994-1998, 2004-2007, 2018 and 2021-2022.

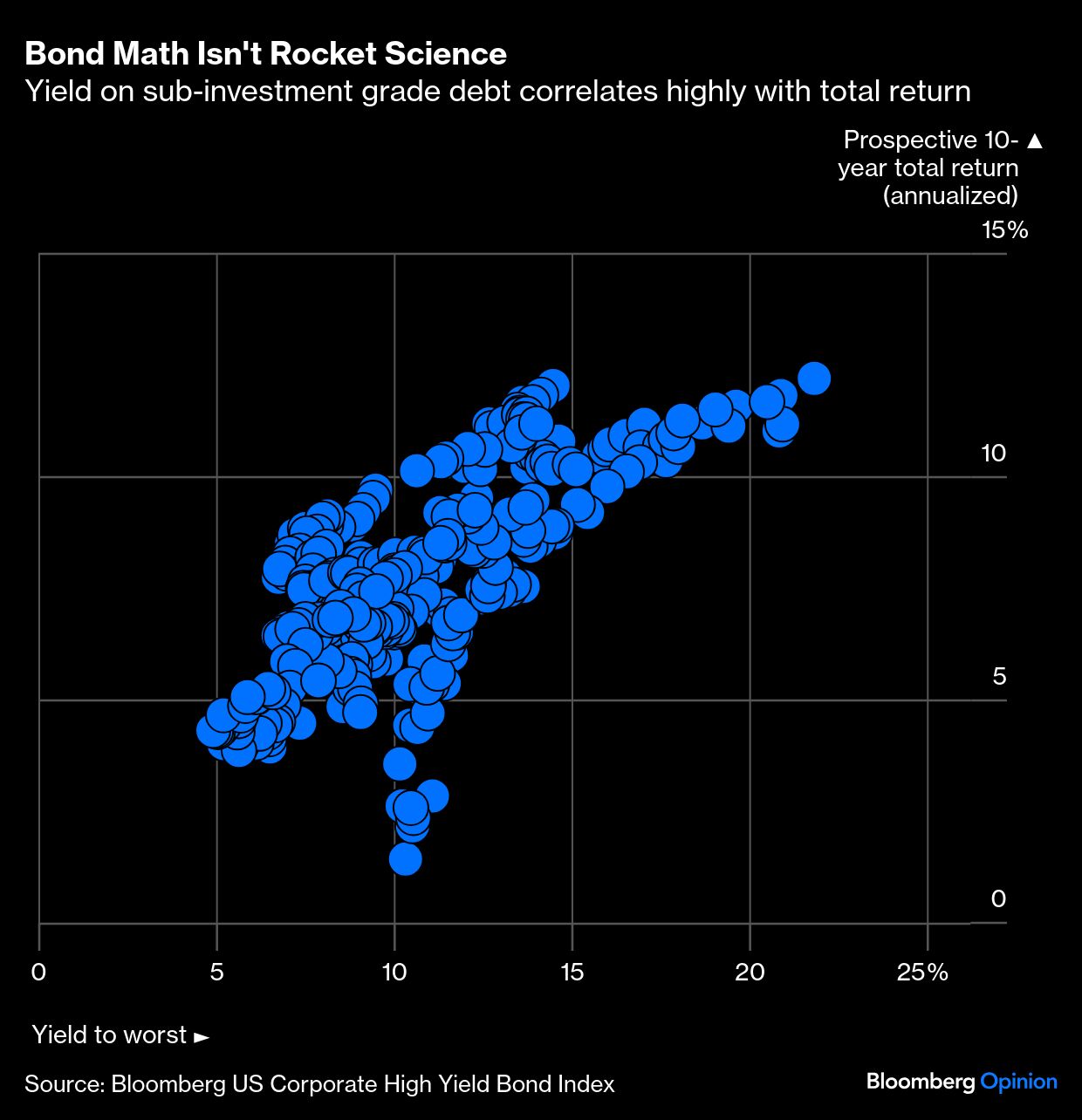

Here’s the thing though: To long-term investors, spreads don’t matter as much as all-in yields. You don’t need to be a rocket scientist to understand that prospective long-term returns are largely correlated with prevailing yields at the time of investment. And at 7.5%, those are still toward the middle of their historical distribution (around the 40th percentile). As the graphic below shows, history would suggest that today’s yields should produce decent 10-year returns. While some part of the return depends on default and recovery rates, the yields have a contractual element. You literally get what you pay for.

And the alternatives aren’t much better. Consider that long-run annualized returns for US equities — which have considerably more short-run variability — are only about 10%. Late last year, the clairvoyants at Goldman Sachs Group Inc. looked deep into their crystal balls and divined that S&P 500 Index valuations and concentration could lead to annualized returns closer to 3% in the next decade. If you shun both equities and risky credit, then you’ll have to camp out in Treasuries or high-grade corporates while you wait on a better entrance point, and it might not come as soon as you think.

“Forget spread,” Oaktree Capital Management co-founder Marks told me by phone last week (echoing the sentiment of a memo he published earlier this month). “Spread is the wrong thing to think about. Do you think the yield will be higher or lower a year from now? That’s what you should be thinking about. Do you care to venture a guess?” (More on my guess later.) Even with all the policy and macroeconomic caveats that I floated, Marks concluded those shouldn’t prevent new or increasing credit allocations. As the co-founder of a firm that manages high yield bond strategies, he’s obviously supposed to say that. Nevertheless, I buy his logic.

For long-term holders, the US high-yield index has never produced a negative total return over a 10-year horizon, and it’s only very rarely underperformed Treasuries. From the perspective of 10-year total returns, the worst months to have invested came in the 1998-1999 and 2012-2014 periods. Spread-based analysis might have helped you avoid corporate high yield in 1998, but it wouldn’t have helped you in 2012 or 2013. In fact, spreads looked quite juicy in the latter periods, but risk-free Treasury yields were so low that all-in yields were the real tell.

Are yields and spreads really sufficient to offset future credit losses inherent to this type of investing? Marks observed in his memo that during Oaktree’s 39 years in the high-yield business default rates have averaged 3.5%, and defaults have cost investors around 230 basis points annually altogether. That means that today’s spread of 314 basis points (and all-in yield of 7.5%) still provides ample cushion under normal circumstances.

Current default rates are lower than average. The quality of the issuers represented on the index has actually gotten a bit better (the Bloomberg index is now more than 50% rated BB, the first large category below investment grade). And a trimmed-mean gauge of the index’s interest coverage ratio puts operating income at about 2.8 times interest expense — down from the very good ratios of the past couple of years, but more or less in line with the 2010-2019 average.

Certainly, Trump’s tariff and cost-cutting alchemy take the economy to an unpredictable new place the likes of which Oaktree and the modern high-yield ecosystem have never really experienced. After all, “Junk Bond King” Michael Milken only started making his name in the 1970s, and the asset class didn’t achieve widespread adoption until a decade or so later. Most high-yield bond indexes treat the 1980s as the dawn of time; their sample periods fail to account for anything that you might associate with stagflation.

That all brings us back to Marks’ question: Do I care to venture a guess about where all-in yields are heading next? I suspect that yields on the index will drift a bit higher, and that long-term investors will get a better opportunity to lock in more attractive prospective returns than they have today. Policy concerns will cause growth uncertainty to fester, pushing up risk premia. The next catalyst may come as soon as April 2, when Trump has pledged to announce “reciprocal tariffs” on countries around the world — a policy that could open countless new fronts on the global trade war, inviting retaliation and corporate supply-chain snarls. I’d guess that Treasury yields will fall, but concerns about the inflationary impacts of the tariffs will prevent them from declining a lot, and that credit spreads will widen more than enough to offset the decline in Treasury yields.

There are a lot of moving parts in that thesis, while the one thing that’s sure is the 7.5% yields available to me right now if I have the stomach for them. During our conversation, I told Marks that I still expected to see a better entrance point in high yield, and he ribbed me that I was ignoring the risk that all-in yields might move down next, not up. After all, the median Federal Reserve policymaker just projected two rate cuts in 2025. The beauty of patient investing is that you don’t really need to have a crystal ball.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin