Britain’s property-transaction tax, known as stamp duty, is set to rise sharply. Currently, first-time buyers pay no tax on properties worth up to £425,000 ($550,000). Starting next month, that threshold drops to £300,000, which will result in a charge of £6,250 on a £425,000 purchase.

That’s created an artificial rush to complete purchases. However, far from easing Britain’s housing crisis, market stagnation is likely to make the problem considerably worse, deterring investment and consumer demand.

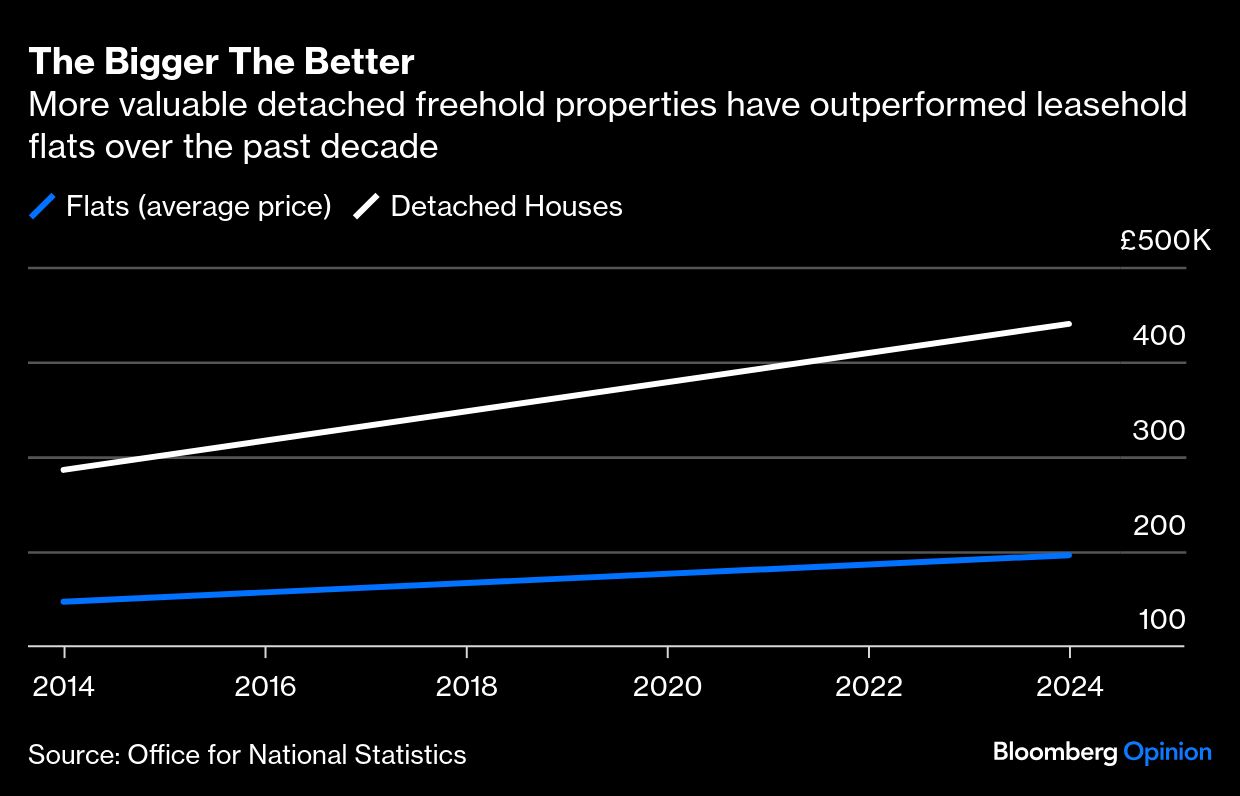

The property market is far more complex and nuanced than both homeowners and, more importantly, policymakers, recognize. Indexes, such as those published by mortgage lenders Halifax and Nationwide, give a misleading picture of uniformity, distilling price movements across a wide variety of property types and tenures down to a single figure.

For example, a typical home in the UK has increased in value by 24% the past decade — half the 48% rise in the Retail Price Index — but detached houses have risen by 35%, while apartment prices have barely budged.

A glaring anomaly for the least affluent is that rent increases have generally accelerated, rising 7.8% in the year to January. Ordinarily, the prospect of record rents would have incentivized investors to fill the void. However, since 2016 successive governments have sought to discourage purchases by investors such that the stamp duty charge for the £425,000 property will amount to £32,500 from next month. Indeed, far from buying additional properties, smaller landlords have been exiting the sector in droves in the face of the growing tax and regulatory burden.

More worryingly, it had been hoped that commercial landlords, who build property specifically for the rental market, might plug the gap. The stock of so-called build-to-rent properties has risen by 23% in little more than a year. However, at just over 120,000, it remains an insignificant part of the private rental market, which currently provides 4.7 million homes. Moreover, the deteriorating outlook has seen construction starts drop by 20% over the past 12 months.

So, if property professionals are giving the market a hard pass, is now really the right time for tenants to be buying their first home?

While the question is simple enough, the answer is complicated and far from obvious. The reasons for this divergence in pricing are varied, but most are consequences of Britain’s archaic leasehold system of ownership, an old problem that’s getting worse for a confluence of legal and financial reasons.

Leaseholders own the right to occupy their apartment for a specific period, possibly for centuries, but they don’t own the land upon which it sits or a share of the building itself. Instead, they pay ground rent to the actual landowner, known as the freeholder. The freeholder then levies an annual service charge on leaseholders to pay for the insurance and maintenance. This is zero-risk free cash flow and an historical anachronism that should be expunged.

A further anvil weighing down apartment prices is the legacy of the horrific Grenfell Tower fire. A parliamentary committee has estimated that 700,000 people live in similarly dangerous apartments and as many as 3 million people have properties that they can’t sell until the faulty cladding that caused the disaster has been replaced. This can afflict buildings from as small as 11 meters (36 feet) high. The total cost of remediating the problem could rise to £22.4 billion, according to parliament’s public accounts committee. The consequences have led to homeowners trapped with properties they can neither sell, insure nor mortgage and in some cases are no longer permitted to even occupy.

Not only did the tragedy lead directly to significant additional costs, but the previous government responded by introducing a new class of so-called “non-qualifying leases,” specifically to further discourage landlords. While homeowners are, to a limited extent, shielded from the full cost of work to remedy these shortcomings, investment properties were explicitly excluded from this protection. Moreover, even after this type of property may have been sold to an owner-occupier, the leases remain ineligible, or non-qualifying, in perpetuity. So, it is quite possible to have two identical properties in the same block, but with two significantly different valuations depending on whether the lease qualifies or not.

Newly built properties ought to avoid this building standards complication but come with their own challenges. Builders like to charge a premium for these brand-new homes However, just like a new car, that premium evaporates the moment the property is occupied. The practical consequence is that mortgage lenders typically require deposits of at least 15% on new builds, beyond the reach of most first-time buyers.

Mortgage lenders are also becoming fussier. They are also very sensitive to flood risk and actively restrict, or even halt, lending in certain areas as the climate risk evolves. Much of central London is in the government’s highest flood-risk category.

The key advice therefore is that while first time buyers now enjoy significant cost advantages over investors, they should tread carefully in areas where professionals have demurred. The risk of being trapped in a home that suddenly becomes near-impossible to mortgage or requires expensive remediation work is nontrivial. So don’t be too concerned that you may have missed the stamp duty deadline. Instead, take the time to do your homework.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Marcus Ashworth