President Donald Trump has said his reciprocal tariff policy was meant to stand up for the American worker, whom he portrayed as the victim of a decades-long shift toward unfettered globalization. His Rose Garden announcement on Wednesday pushed import duties to an average rate of around 22%, the highest in over a century. But even if these policies improve the lots of workers (and I really doubt it), the efforts are already coming at the expense of American retirees.

First and foremost, that’s because Trump’s grand experiment is precipitating the swift collapse of the S&P 500 Index, the underpinning of tens of millions of retirement savings accounts. The S&P 500 is down around 11% since Wednesday and 17% since the February high as equity investors speculate that the policies will unleash chaos in global supply chains, hurt corporate profits, delay capital expenditures and drive up many consumer prices. And while populists like Trump draw a false distinction between the fortunes of Wall Street and Main Street, it’s clear that many Americans are facing uncertainty and the prospect of financial duress from his policies.

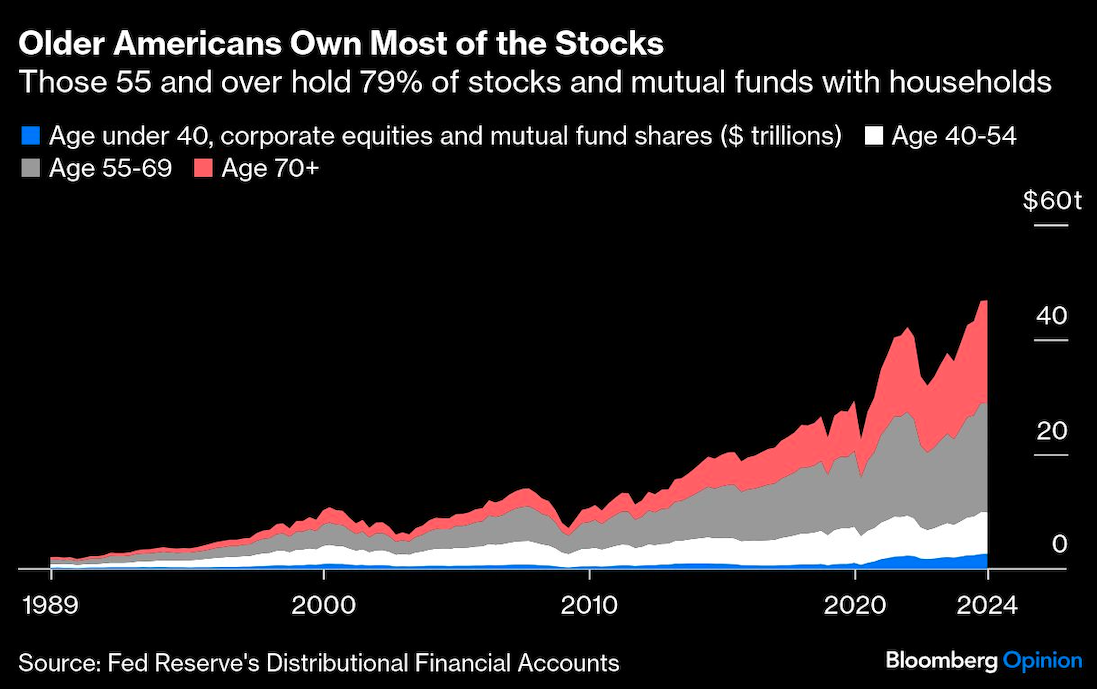

Men and women ages 55 and over now hold about 79% of corporate equities and mutual funds among US households, according to Federal Reserve data. In aggregated Gallup survey data from 2019-2024, about half of non-retired Americans expected their 401(k) or other retirement savings accounts to serve as a major source of income when they stop working, and 29% of actual retirees said that it already is. Although many of those older Americans should perhaps have trimmed their equity exposure as they aged into retirement, they don’t always follow that advice, and the relentless surge in stocks over the past 15 years may have encouraged an excessive allocation to riskier investments. In 2023 data of defined contribution plans, Vanguard Group found that the 65-and-over cohort had a 49% average equity allocation and the 55-64 cohort had 64%.

To the extent that the market keeps falling, it will automatically hit the millionaires and billionaires (okay, fine); the old and relatively well off (not great) and millions of regular retirees that worked hard all their lives to build a nest egg (bad). The outcome will be all-the-more challenging if, as many economists expect, tariffs deliver a stagflationary shock that keeps inflation high even as the the economy sputters.

But the fortunes of richer and older Americans are also intertwined with the rest of the economy, including the very workers that President Trump purportedly wants to help. Well-off Americans control a large majority of businesses, and lately, they’ve accounted for a surprisingly high proportion of the consumer economy. Research from Federal Reserve economists last year showed that it was the highest earners — the folks most likely to own stocks — who have powered the extraordinary run in retail sales.

The “wealth effect” suggests that households tend to make spending decisions, at least in part, based on developments in their portfolios. If the selloff translates into consumer retrenchment, that could affect the roughly 29 million jobs in retail, wholesale trade, transportation and warehousing. Elsewhere, it could show up in discretionary services such as leisure and hospitality, responsible for around 17 million jobs. Perhaps President Trump thinks those people will find new employment in the factories of the future, but that long-shot ambition may be cold comfort for those struggling in the here and now.

In Trump’s telling, any negative effect will be worth the price. He claims that he’s out to reverse the decades of “unfair” trade that hollowed out the US manufacturing base and led to stagnation in the real wages of many workers. His story of American greatness lost too often pays short shrift to the role of automation in cutting factory jobs and the declining role of unions in allowing wage stagnation. It also downplays the exceptionally good 4.2% unemployment rate, which is proof positive that other jobs have emerged as factory employment fell. I will grant him this: The economic status quo in the US has tended to enrich asset owners more than workers, exacerbating inequality, and it’s hard to completely rule out the notion that trade policy had some role to play. Certainly, the mercantilist trade tactics of China demand some hard choices.

But as we search for the ideal policy mix, we can’t sacrifice the stock market and court recession to test Trump’s theory about restoring lost manufacturing jobs — a move that would constitute burning down the house to smoke out a rat, eventually hurting everyone whether they own equities or not. And again, I remain skeptical that this strategy will even pay dividends for the people it’s theoretically supposed to help.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.