For too long, British oil company BP Plc denied, obfuscated and played down its troubles. The market and the media, rather than the company, was the issue. On Tuesday, the oil major took the first step toward redemption: “BP can and will do better for investors,” it said. Amen.

Incoming Chairman Albert Manifold and Chief Executive Murray Auchincloss will conduct a wide-ranging review of the company’s entire portfolio of businesses — all of them. That should mean there will be no more sacred green cows. The aim is “maximizing shareholder value moving forward – allocating capital effectively.” Or, in plain English, sell, restructure or shutdown whatever doesn’t make enough money – and sadly, there’s plenty. BP also announced a “further cost review,” corporate jargon for cost cutting and firing employees.

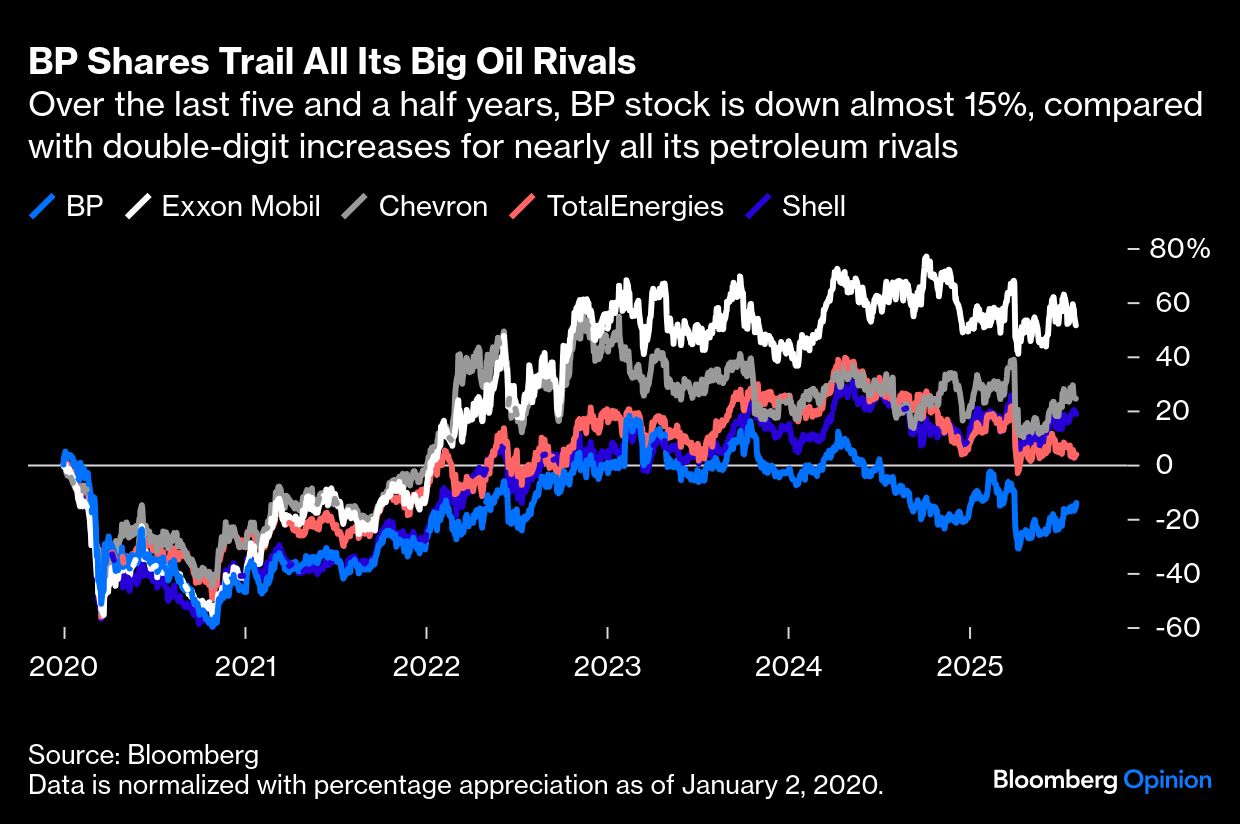

Regular readers know I’ve been a critic of BP for the last five years or so. To me, the company has squandered shareholders’ money trying to shift from its tried-and-tested business of pumping, refining and selling oil and gas. Forced by poor returns in its green projects, inflated costs and the arrival of an activist investor , it finally “reset” its strategy in February. But it seemed a half-hearted change; more a 90-degree move than the 180-degree U-turn needed. Since then, BP executives have continued to blame the market, rather than themselves, for their travails.

Enter Manifold, the former CEO of New York-listed cement company CRH Plc. His appointment as BP chairman last month didn’t get investors excited, to put it mildly. “Albert who?” was a typical comment. But months before he formally starts in October, he’s signaling he gets both the task ahead and its urgency. In many ways, he’s replicating what he did in his previous job. And what a success that was.

The first good sign is that he’s acting even before he sits down in St. James’s Square, the company’s headquarters a stone’s throw from Buckingham Palace. In a quarterly earnings release, BP said that Manifold and Auchincloss had had the first meeting, and they agreed on several actions. First, is the admission the company needs to do better. Second, the move to put all the businesses under review. Third, a commitment that costs need to come down further, and quickly. And fourth, highlighting that maximizing shareholder value is key. All music to my ears (and those of BP’s shareholders).

It's tough to be a Big Oil company. Investors prefer technology champions rather than old and polluting industrial behemoths. Thus, the chairman’s first job often is to give shareholders a reason to buy the stock – above that of its rivals. For BP, that means demonstrate that it’s a better custodian of value than its peers, which included better-managed companies like Exxon Mobil Corp., Chevron Corp. and Shell Plc. So far, BP has failed to do so. But the new comments from its incoming chairman suggest change is afoot.

The crucial step to convince shareholders is to lower the breakeven oil and gas price that BP profitability requires. When the company announced its new-ish strategy in February, it said it anchored it around $70 a barrel – using 2024 real prices. Add inflation, and that equals nearly $72 a barrel in today’s money. Look at your screen, and Brent is below that. The only way to get out that hole is to cut costs, perhaps savagely.

BP had promised to reduce annual operating costs between $4 billion and $5 billion by 2027. Paul Singer’s Elliott Capital Management, which has built a 5% stake in the company, has called for an additional $5 billion. On Tuesday, Auchincloss admitted that his initial target, set only in February, wasn’t enough. That’s quite an indictment on the CEO.

Day-to-day costs aren’t the only problem: BP is still investing in many green ventures that appear ill-suited for its fossil-fuel expertise. Hopefully, the portfolio review initiated by the incoming chairman will flag them for divestment, lowering overall capital expenditure needs from the current $14.5 billion target in 2025, and a range of $13 billion to $15 billion for 2026-2027. Selling some of those businesses would allow BP to reduce its inflated headcount, too.

BP is making progress. The second-quarter result was better than expected, and the company lifted its dividend. With the incoming chairman openly accepting the company needs to do a lot better, there’s hope: More than five years after BP embarked on a value-destruction strategy, the British oil major is sketching the outlines of a project that would make it investable again. Shame it took this long.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Javier Blas