Regional Banks Are Ripe for Mergers as DC Warms to Consolidation

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsFor years, US regional banks have operated under a paradox. Like all companies, they need growth to survive and want to do so predictably. Every billion dollars in new assets directly pads the bottom line. But the post-2008 regulatory crackdown designed to make banking safer has also made the slow-growth strategy trickier.

The moment a bank tiptoes across a key threshold like $100 billion or $250 billion in assets, more compliance costs kick in, potentially weighing on new revenue growth for years. Alternatively, banks can catapult past each regulatory asset threshold, typically through a merger or acquisition. A $90 billion bank joins forces with an $80 billion one, hopefully creating an institution that’s big enough and profitable enough to justify the new costs. “The basic premise is you’d rather leap across than crawl across,” says Gregory Lyons, a corporate partner specializing in financial institutions at the law firm Debevoise & Plimpton. “You don’t want to be the bank that has $250.1 billion. Because then you get all the regulatory burdens but not the scale.”

Making the big jump hasn’t been easy, though. The Biden administration’s aggressive stance on bank regulations and the 2023 crisis around Silicon Valley Bank and others hindered mergers and acquisitions. Banks that announced deals often found themselves in limbo, waiting more than a year for sign-off from regulators. Interest-rate hikes quickly eroded banks’ bond values and capital cushion, making M&A less feasible financially. Regional banks found themselves too big to sit still but too small not to worry about inching over the next regulatory hurdle.

Now the change in the Oval Office is set to potentially break the logjam. Signaling a much friendlier stance on consolidation, regulators under President Donald Trump cleared the way in April for Capital One Financial Corp.’s blockbuster acquisition of Discover Financial Services. With other Biden-era merger guidelines expected to be rolled back—and the Federal Reserve indicating an openness to deregulation—banking analysts and investors are eyeing a major reshuffle. “It’s not going to be getting any better than this from a regulatory perspective,” Lyons says.

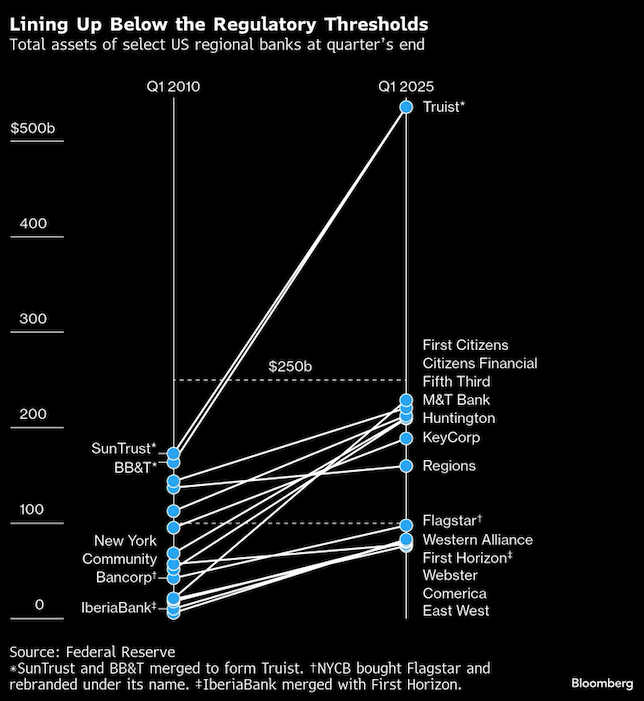

Plot banks on a chart by their assets, and you’ll spot what looks like a crowd milling around a closed airport gate, waiting for boarding announcements. Multiple US banks are now idling below key asset thresholds. As of the first quarter of this year, five regional banks are within $50 billion dollars of the $250 billion threshold.

Another six regional banks sit just below a key $100 billion line. So what exactly determines these thresholds? Following Basel III, a global regulatory framework that was developed in the aftermath of the 2008 financial crisis, US banks are sorted into categories based on asset size. Whenever a bank grows past $100 billion, $250 billion or $700 billion, it graduates to a higher level of scrutiny as it’s deemed more systemically important to the broader financial system. The challenges of upgrading technology, legal and accounting expertise, and balance sheet capacity to meet stricter capital and compliance requirements can take years to complete. Some estimates point to a 1% to 2% increase to a bank’s annual expenses.

Complicating matters, inflation has eroded the real value of the thresholds, making it easier for banks to hit each line. Gene Ludwig, a former chief banking regulator for the Clinton administration who’s now an adviser and venture capital investor in financial services companies, says the current asset-based classifications are outdated. “We can’t expect banks to thrive under rules built for another era,” he says. “When regulatory thresholds fail to reflect reality, banks are forced into a false choice: limit their ambitions or outgrow their regulatory category.” But indexing thresholds to inflation would bring other complications. Graham Steele, a former official at the US Department of the Treasury, says that a moving target would make planning deals more difficult.

In practice, the thresholds aren’t quite magic lines that change everything for a bank once they’re crossed. Regulators, Ludwig notes, expect banks to prepare for these standards long before they officially cross the threshold. In a speech last year, Michael Barr, then-vice chair for supervision at the US Federal Reserve, noted that many of the risks at Silicon Valley Bank built up when it was still below the $100 billion threshold. He called for regulatory supervision of fast-growing banks to escalate “on a gradual slope and not a cliff.”

For banks, the real-world costs of early prep work for crossing a boundary can be enormous. Huntington Bancshares Inc. in Columbus, Ohio, started preparing for crossing the $250 billion line in 2022 when it had only $170 billion in assets. Chief Financial Officer Zach Wasserman says the effort has cost the bank an additional $50 million to $100 million in expenses each year and won’t be completed until early next year. The bank had $210 billion in assets at the end of March.

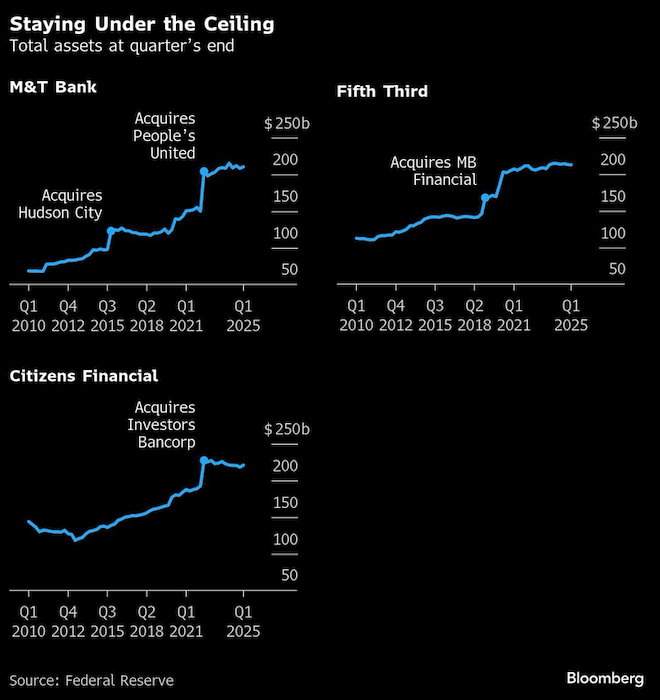

SunTrust Banks Inc. in Atlanta and BB&T Corp. in Winston-Salem, North Carolina, were the rare banks to cross the $250 billion line in recent years. They did so through a merger forming Truist Financial Corp. in Charlotte, North Carolina, with more than $500 billion in assets. Many other banks, including M&T Bank, Fifth Third Bancorp and Citizens Financial Group, have cruised steadily along below $250 billion for several years. Asset growth isn’t the only option for improving profits, says Gerard Cassidy, co-head of global financials research at RBC Capital Markets—regional banks can also improve their mix of assets and reduce expenses.

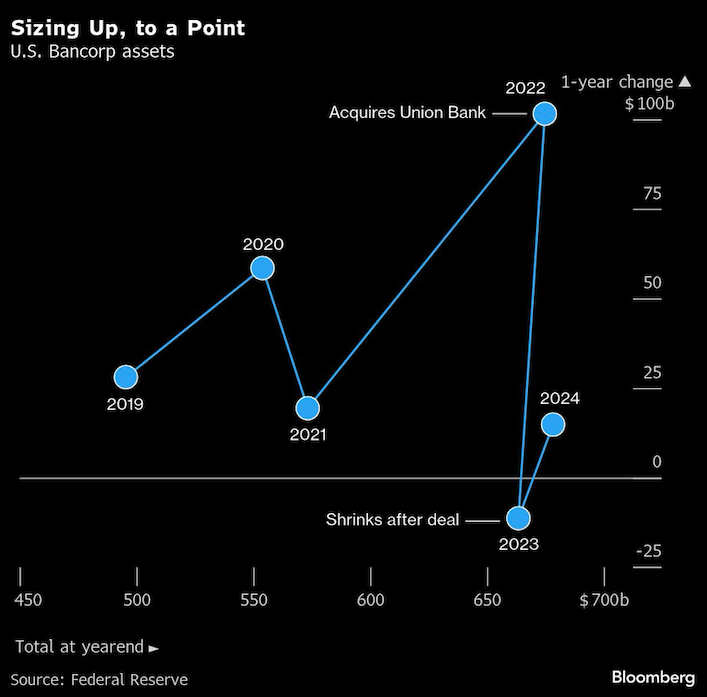

The delicate nature of approaching a regulatory threshold is best understood by looking at a bank that recently attempted it. In late 2021, U.S. Bancorp, a bank in Minneapolis with $559 billion in assets at the time, announced that it would acquire the core regional banking business of Union Bank from Mitsubishi UFJ Financial Group Inc. to expand in California. The ambitious acquisition would add approximately 1 million customers and $133 billion in assets, but it also landed the combined entity so close to the $700 billion threshold that U.S. Bancorp preemptively chose to comply with the next, stricter tier of rules.

The timing proved difficult for U.S. Bancorp. Caught between expensive integration costs and the market pressure that came with rising interest rates, the bank decided to sell off assets, in part to avoid being bumped up into the stricter regulatory category. Now the bank, which got a new chief executive officer in April, is again the subject of investor speculation about a merger that would bring it well past $700 billion in assets. “It’s not on the table,” said CEO Gunjan Kedia in an interview with Bloomberg News in May. “We take our medium-term goals very seriously, and M&A does not fit that promise to restore our valuation, to restore investor confidence.” The bank says it plans to stay under $700 billion until at least 2027.

Regulatory changes may be coming. Michelle Bowman, the new vice chair for supervision at the Fed, appointed by Trump, has been a proponent of tailoring bank regulation to an institution’s overall risk profile, not merely its raw asset size. Bank executives, who would benefit from greater flexibility, were vocal supporters of her nomination. Critics worry that more flexibility will mean more risk-taking. “This whole approach really acts like regulators can in advance predict which banks are going to cause financial instability,” says former official Steele.

Regulatory changes could cut both ways for M&A. Some banks might find it easier to merge, whereas others could decide it’s less essential to do so. “What used to look more like a cliff or a wall to get over is much smaller and may not even be that big a bright line at the end of the day,” First Horizon Corp. CEO Bryan Jordan said at an investor conference in June. His Memphis-headquartered regional bank, with about $80 billion in assets, is one of many now preparing to cross the $100 billion threshold in the next few years.

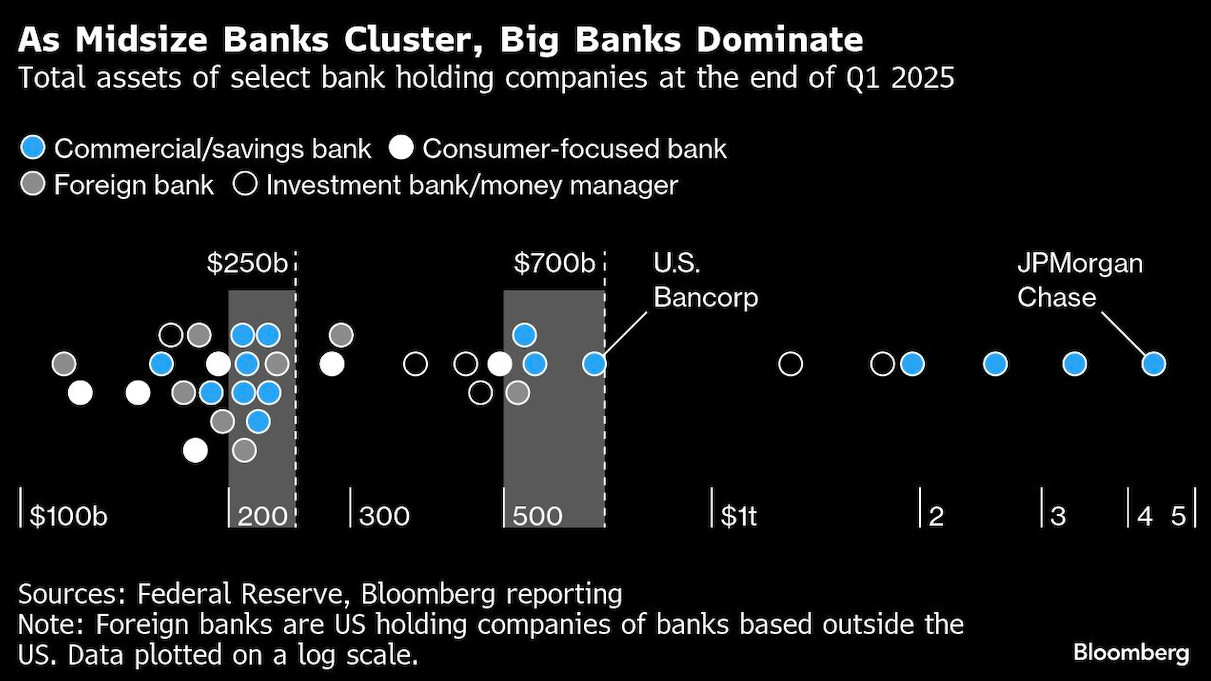

The regulatory hurdles have contributed to the growing chasm between the super-regionals and the four largest banks: JPMorgan Chase, Bank of America, Citigroup and Wells Fargo. “In the banking industry, Goliath is winning, and scale is making more of a difference than ever before,” says Mike Mayo, head of US large-cap bank research at Wells Fargo Securities. Since 2010, JPMorgan Chase & Co. has more than doubled its assets, from $2 trillion to about $4.5 trillion. Its nearest rival, Bank of America Corp., now holds almost $3.5 trillion in assets. Next in size comes Citigroup Inc., followed by Wells Fargo & Co. at just under $2 trillion. And then, leaving aside investment banks Goldman Sachs Group Inc. and Morgan Stanley, it’s a big drop to U.S. Bancorp.

“We have a handful of extremely large banks and we essentially hamper the ability of the super-regionals to compete with them,” says Randal Quarles, a former Federal Reserve official. “I think it would be a better system if you had a more continuous range of size.” The last time a true banking giant was formed was 2008, when Wells Fargo crossed the $1 trillion asset mark by acquiring beleaguered Wachovia Corp.

“Three decades ago, if you asked me if this was the way I thought it would play out, I would say absolutely not,” Mayo says. “JPMorgan should have more trillion-dollar bank competitors, and as long as they don’t, I’m going to keep increasing my price targets and probably my earnings estimates.” —With assistance from Mark Glassman

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All