As the specter of stagflation ripples through equity markets, investors are zeroing in on the upcoming consumer inflation report to see how close the dire economic scenario is to becoming a reality.

A combination of slowing economic growth and rising price pressures isn’t investors’ base-case scenario just yet. Still, the latest government reports showing hiring has cooled while services inflation resurfaced is starting to weigh on sentiment, raising uncertainty about the pace of interest-rate cuts. The latest economic data “magnifies the importance” of this week’s CPI report, JPMorgan Chase & co. strategists wrote in an August 5 note.

To Karl Schamotta of Corpay Inc., the way to navigate the risk of stagflation is to stick to defensive sectors like utilities, communications services and consumer staples while shunning growth-focused sectors like consumer discretionary. To him, the extra challenge comes from balancing expectations for rising prices against US President Donald Trump’s pressure on the Federal Reserve to lower rates.

“This is a turning point in the economy that we stand at and markets are really unsure as to what direction we’re going to go in,” said Schamotta, chief market strategist at Corpay. “We need to worry that a Fed that’s less focused on its price stability mandate is going to allow inflation to be higher over time.”

Across Wall Street, uncertainty about a return of 1970s-style stagflation has economists and strategists concerned the Fed will hold interest rates steady, eliminating a key catalyst for the stock market.

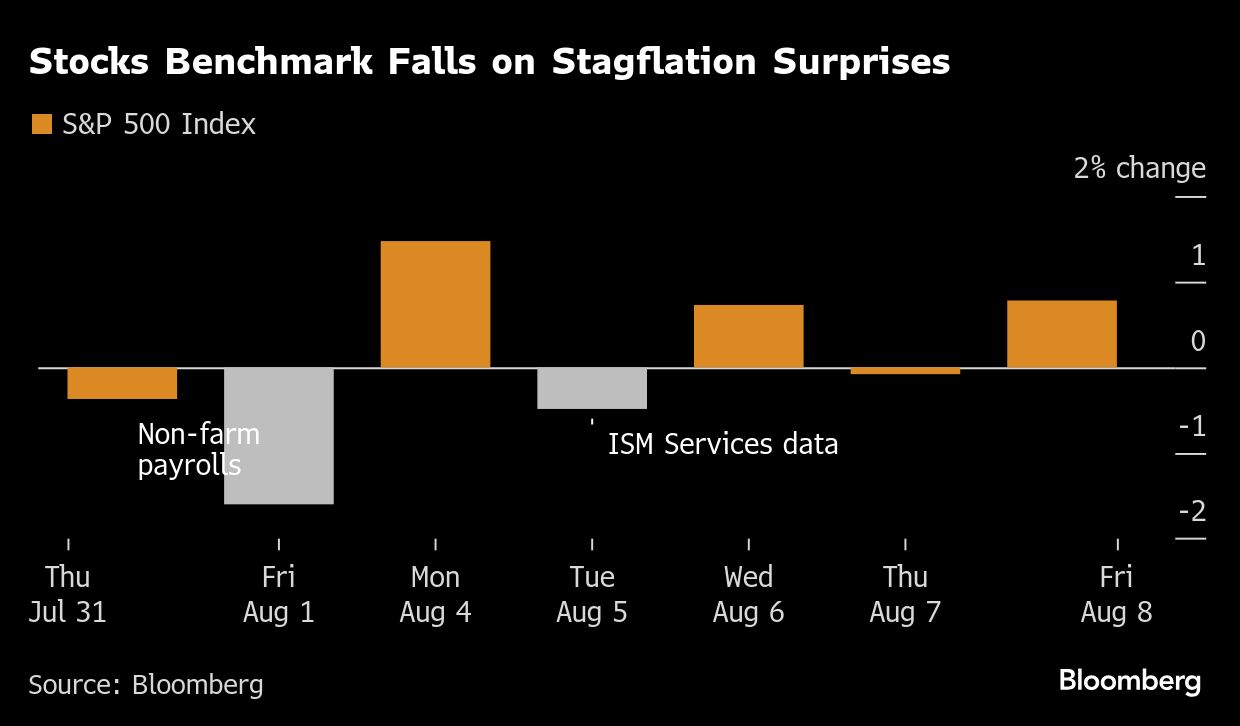

The S&P 500 Index, which has climbed 8.6% so far this year, dropped after a weaker-than-expected jobs report earlier this month and an uptick in services inflation.

“In a stagflationary environment, it is dangerous to cut without clear evidence that inflation has peaked,” Bank of America economists wrote in a note, reiterating their call the Fed will remain on hold for the balance of the year even with weaker jobs numbers.

‘Stagflationary Shocks’

Torsten Slok, partner and chief economist at Apollo Management, prefers sectors like telecommunications, healthcare, utilities and technology that are less impacted by macroeconomic uncertainty and tariffs.

Notably, he listed energy among the sectors that are set to see a negative impact. The group was a winner in the inflationary cycle of 2022, leading the S&P 500 higher two years in a row as traders sought a hedge from rising prices in the oil-and-gas producing sector.

“Tariff hikes are typically stagflationary shocks – they simultaneously increase the probability of an economic slowdown while putting upward pressure on prices,” Slok wrote in a Thursday note.

Brian Jacobsen, chief economist at Annex Wealth Management, likes sectors that exhibit less volatility in this environment and are offering some positive business and earnings momentum, including financials, industrials and technology companies that behave like “business staples” rather than consumer staples. He likes Microsoft Corp. and Amazon.com Inc. for their cloud businesses.

To be sure, Jacobsen said he does expect the market’s anxiety about stagflation will wane in the coming weeks, as he expects some of Trump’s tax cuts may spur investment, potentially offsetting the weaker job numbers in future reports.

For now at least, uncertainty remains high. US consumer inflation expectations rose in July, according to a monthly Federal Reserve Bank of New York survey.

“We think inflation is a longer-term cycle,” said Mark Dodson at Cypress Capital. He added that he sees inflation accelerating in 2026 and Treasury yields and mortgage rates “may not fall the way many expect when the Fed pulls the trigger.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Geoffrey Morgan