The US oil industry is often compared to being on a treadmill: you run fast just to stay still. Because shale wells quickly sputter, companies need to rapidly drill replacements — a laborious and expensive endeavor. Of late, the treadmill feels like it’s running just a bit slower. The result? American oil production is holding up despite Saudi Arabia and Russia driving prices down.

The outcome is crucial for the crude market as two out of every 10 barrels worldwide are pumped by the US. For the OPEC+ cartel, more resilient American oil production will lower prices for the rest of this year and into 2026.

The trend was clear during the industry’s earnings season. In quarterly updates and conference calls, most companies announced what Houston oil banker Dan Pickering summed up as “more production, less spending.” Jeff Leitzell, chief operating officer of shale giant EOG Resources Inc., set the tone: “Once again, we outperformed both our production and cost expectations.”

Shale companies are doing more with less by creating wells more quickly, and that reach further into the rock. In the process, they’re reducing the number of drilling rigs and fracking crews, lowering costs. Kaes Van't Hof, chief executive officer of shale giant Diamondback Energy Inc., reckons his company is pushing “the limits of efficiency.” Others are too. Once upon a time, shale wells took several weeks to drill; now, some are ready in four days.

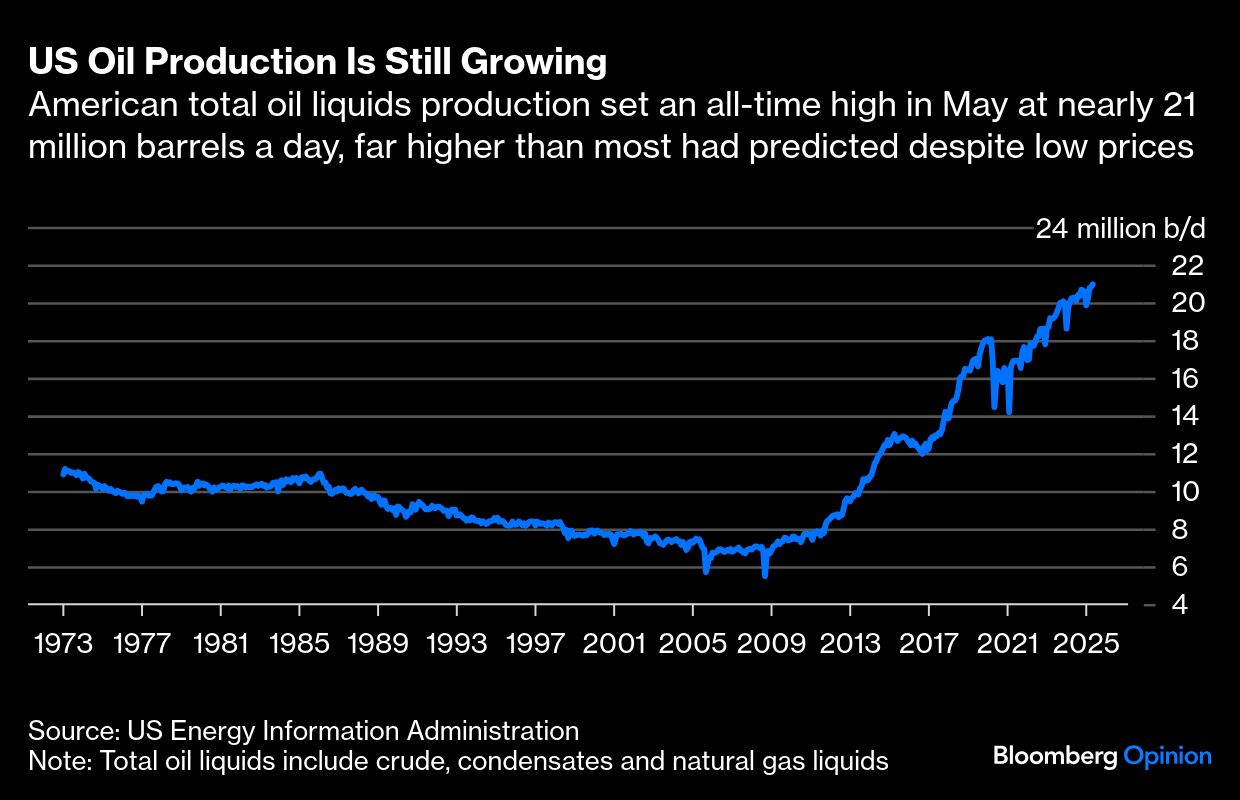

With the efficiency drive slowing the treadmill, US oil production is holding up far better than my already upbeat prediction earlier this year. In May, I anticipated that output would peak at around 20.4 million barrels a day and then stay close to that zenith in an undulating plateau. Others, perhaps influenced by the downturn of 2015 and 2020, predicted rapid decline.

In fact, the most recent monthly data shows that US petroleum output hit an all-time high of 20.96 million barrels in May, after preliminary figures based on weekly data were revised significantly higher. The same weekly data pegs output in early August at about 20.8 million barrels a day.

The message is twofold: not only is US petroleum production holding up, it’s doing so at a much higher level than many expected only a few months ago. In the first five months of the year, US total petroleum output has averaged just over 20.5 million barrels a day, up from about 19.8 million during the same period in 2024. A lot of the production gains have come from so-called condensates and natural gas liquids, rather than crude.

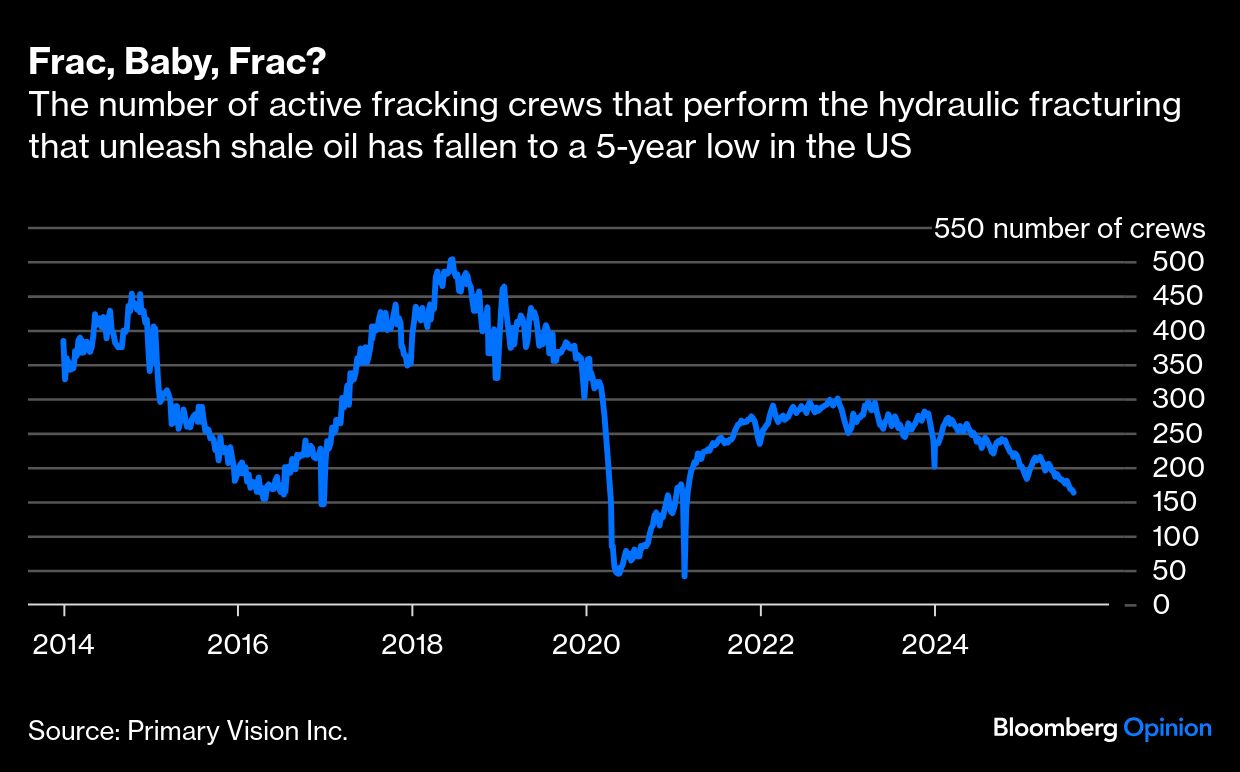

Despite the efficiency-driven resilience, at some point shale production will fall, considering the amount of cost-cutting the industry has already embarked on. Van't Hof of Diamondback called such a decline “inevitable” after the number of active oil drilling rigs now fell to 411, the lowest since late 2021, according to data from energy services business Baker Hughes Co. But in shale, drilling isn’t the most important barometer. Far more important is the proportion of so-called frac crews, the specialized teams that perform hydraulic fracturing, or fracking, on the wells; injecting water, sand and chemicals underground to free oil from the hard-to-crack shale rock. The number of frac crews has dropped to a five-year low of 163, according to Primary Vision Inc., a firm that tracks industry trends.

With shale, small price shifts matter a lot: The difference between booming production and declining output is measured in a fistful of dollars, perhaps as little as $10 to $20 a barrel. At $50, many companies are staring at financial calamity and production is in free-fall; $55 is survivable; $60 isn’t great, but money still flows and output holds; at $65, everyone is back to more drilling; and at $70, the industry is printing money and output is soaring.

In May, the American oil industry was on the ropes, with crude approaching $55 a barrel. Then, Israel attacked Iran, driving prices as high as $78.40 a barrel. The conflict handed US shale producers an unexpected opportunity to lock-in forward prices. That hedging, alongside the efficiency gains, is now sustaining production.

West Texas Intermediate, the industry’s oil benchmark, is now hovering just under $65 a barrel. Executives have indicated that WTI will need to trade in the low-to-mid $50s for a full month before the shale industry reduces spending further.

Moreover, shale isn’t the only game in the American oil industry. The US Gulf of Mexico accounts for nearly 20% of total US petroleum production, and output there is likely to increase this year as several projects come onstream.

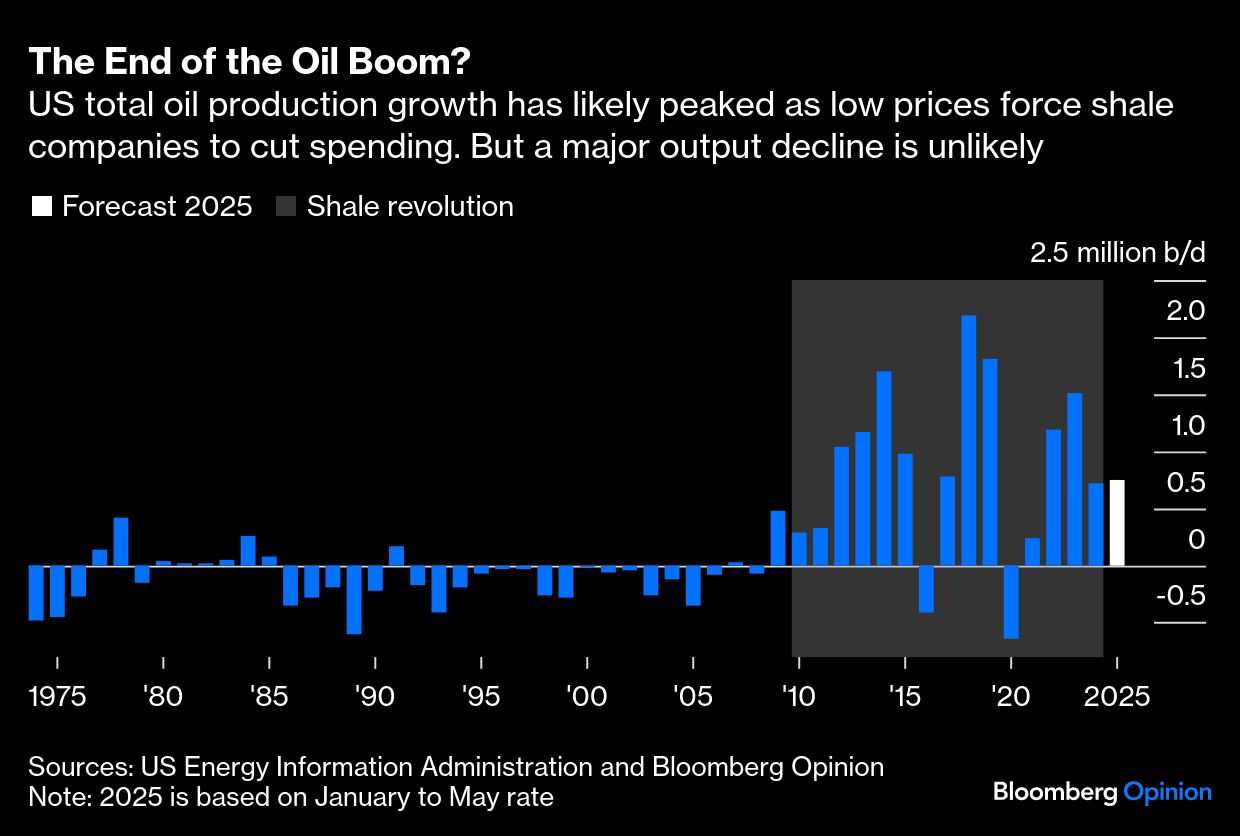

For now, everything suggests the US is riding the OPEC+-induced oil price crash even better than the most optimistic had expected, and certainly a lot better than the naysayers’ dire predictions. With so much of the year already over, it’s clear that US oil production, on an annual average, will grow in 2025 relative to 2024. Any decline in 2026 will only come from a higher baseline — and probably be shallower than OPEC+ had hoped. If the cartel wants to subdue the American oil industry, it will need to drive prices even lower.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Javier Blas