President Donald Trump’s chaotic tariff policies have upended global trade and led to questions about whether the days of US exceptionalism and leadership that attracted capital from around the world are over. America’s labor market is on shaky ground, with job growth grinding to a halt. Inflation rates show signs of turning higher again, raising doubts about whether the Federal Reserve can resume interest-rate cuts. So, naturally, the benchmark S&P 500 Index of stocks is… at a record high?

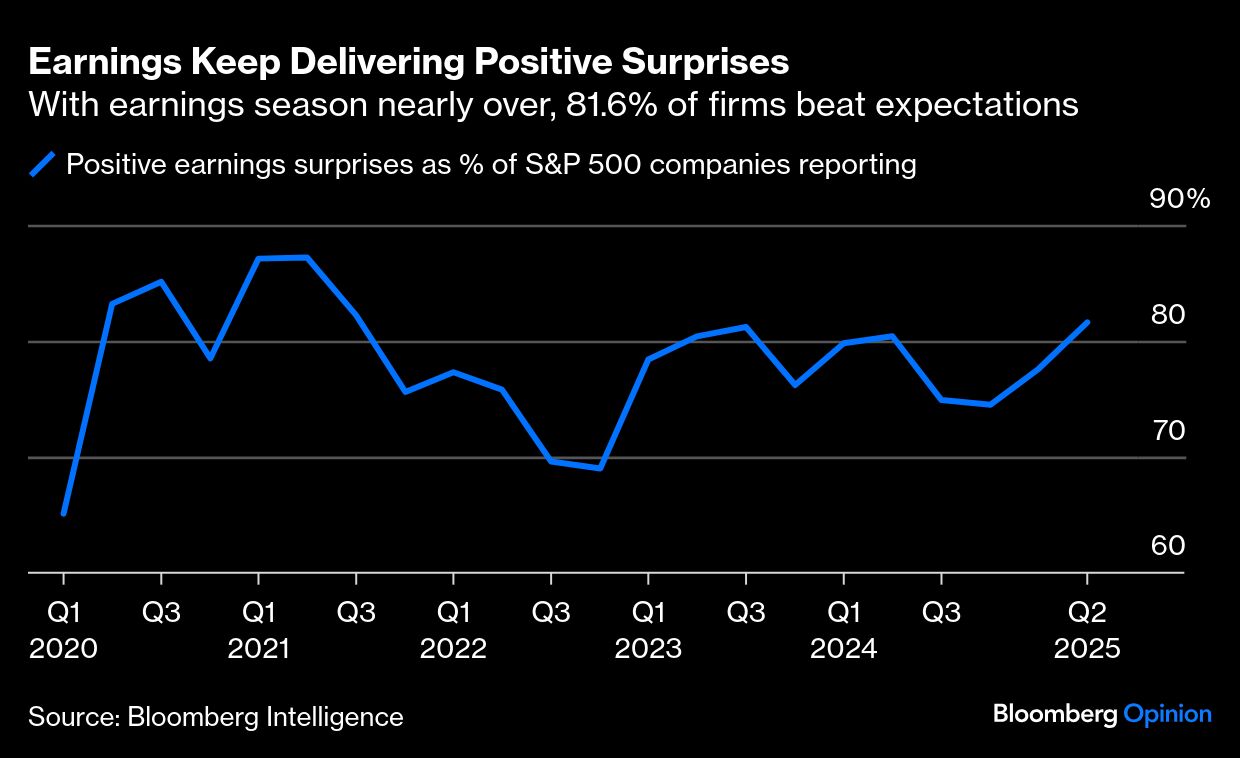

It’s really no mystery why equities are seeming to defy logic when you realize that fundamentals, rather than sentiment, ultimately prevail. Just consider the current earnings season, which is just about to wrap up. With about 83.7% of S&P 500 constituents by weighting having reported results for the second quarter, earnings look to have surged 10.5% from a year earlier, obliterating Wall Street’s forecast of a 2.8% gain, according to Bloomberg Intelligence. Some 81.6% of companies have topped estimates, the most since 2021. This has led analysts to bump up their 12-month price targets at the fastest clip since early 2024.

Now comes the big question: Can corporate America continue to outperform or are markets just whistling past the macroeconomic graveyard?

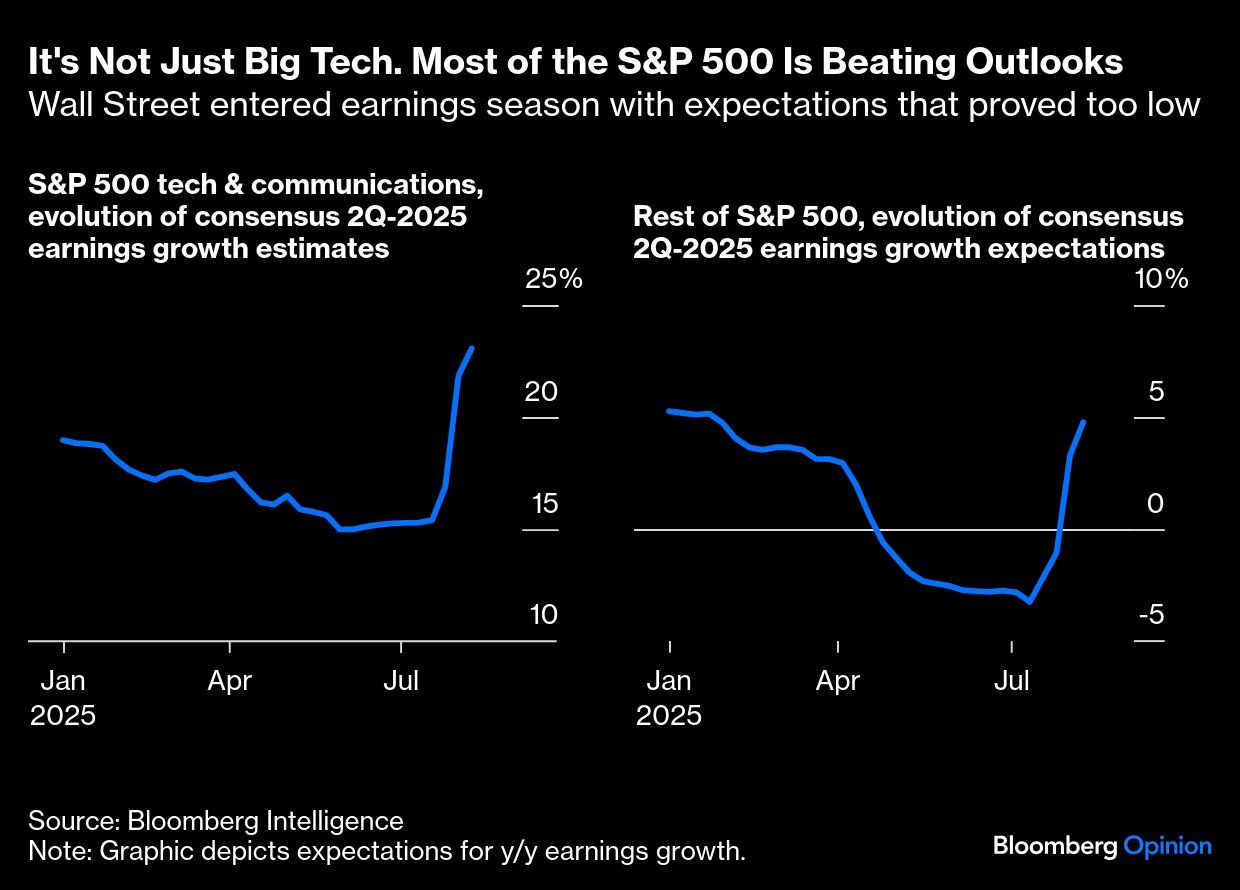

To answer that question it first helps to understand why earnings have exceeded expectations. The too-low second-quarter forecasts appear to be a holdover from the “Liberation Day” tariff panic of early April. Trump’s shocking opening salvo on April 2 — elements of which were subsequently delayed, tweaked or walked back — triggered broad and precipitous downward earnings revisions that analysts have been slow to adjust, with the exception of tech and communications companies. Excluding those sectors, S&P 500 earnings were supposed to fall 3.3% year-over-year, but may end up growing around 4.8%.

Second, those tech and communications superstars — several of which operate in cloud or advertising businesses that aren’t directly affected by the global goods trade — keep surpassing already-high expectations. We still need to hear from the Nvidia Corp., the unofficial mascot of the bull market in all things tied to artificial intelligence, but the two sectors’ earnings are on pace to grow 23.1% in aggregate, whereas Wall Street expected 15.3% growth. Results have gotten bumps fromMicrosoft Corp., Meta Platforms Inc. and Google-parent company Alphabet Inc.

Still, it’s more than just luck and lazy analysts. The reality is that big companies have become nimbler and leaner, allowing them to leverage their already substantial market power. As my Bloomberg Opinion colleague Thomas Black pointed out, many companies have pulled back on their initial assessments of how badly tariffs will hit their bottom lines, partially a reflection of the lower effective tariff rates on certain key markets.

Toymaker Hasbro Inc., a major importer from China, initially estimated a tariff-related hit of $60 million to $180 million, but now says the actual hit to 2025 profits will be at the low end of that range. “While tariffs represent a headwind for the business, the current duties are better than the range we discussed in our last earnings call,” Chief Executive Chris Cocks told analysts last month. “We are compensating for these costs through a combination of cost reductions, rebalancing our marketing spend, diversifying our supplier mix, and implementing some targeted pricing actions.”

Another key point (courtesy again of Tom) is that benefits in the new tax and spending package recently passed by Congress could more than offset the tariff hit to cash flows for some companies, including 100% bonus depreciation and research and development expensing. Defense and security manufacturer Lockheed Martin Corp. said the tax law could provide $400 million to $600 million in cash tax benefits. That’s potentially more than the $500 million combined cash flow hit the company expects this year from both tariffs and a classified aerospace program it’s working on.

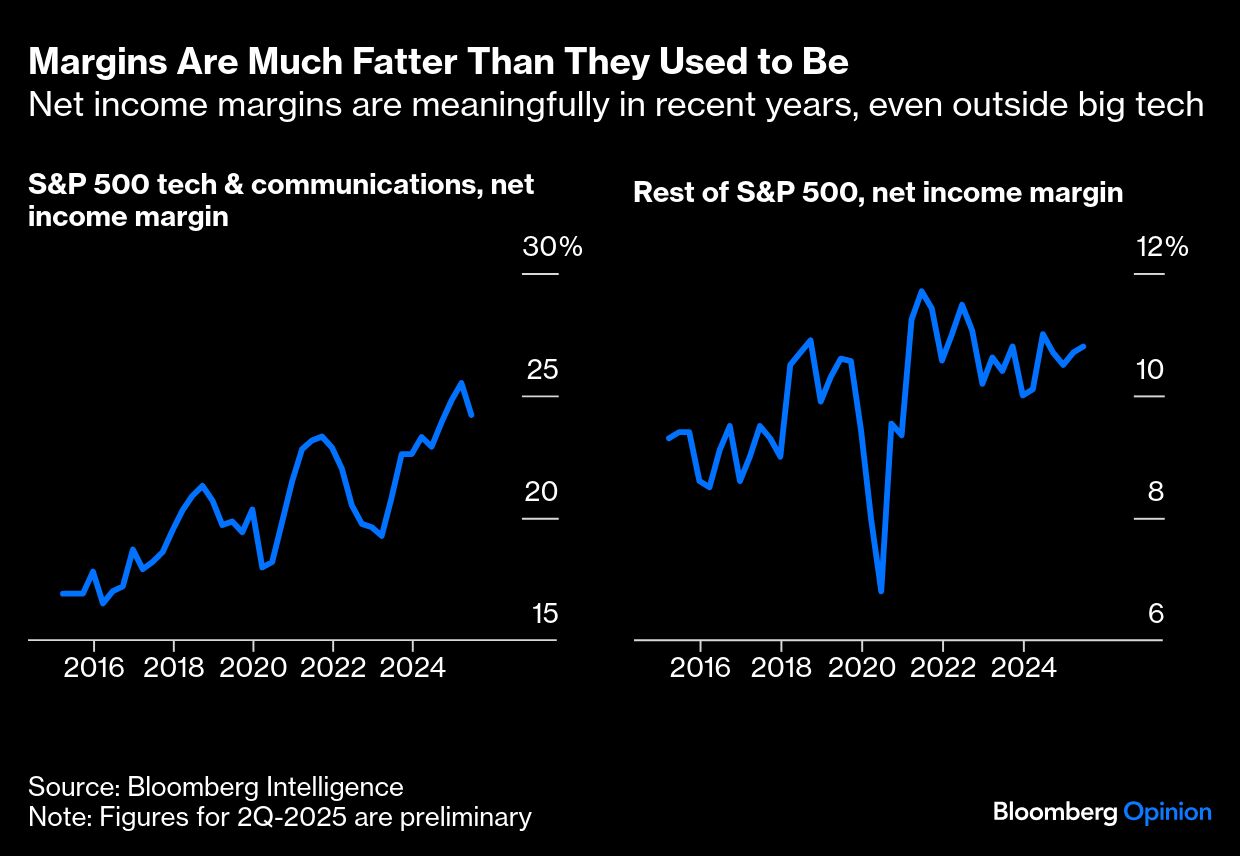

At least anecdotally, the positive momentum in corporate fundamentals looks plausibly sustainable, which should help underpin equities even at current valuations. The ability of companies to manage their bottom lines is a reflection of a broader a push toward leanness and efficiency made more urgent by the dark days of the global pandemic. Even excluding the tech and communications stocks, S&P 500 net profit margins now consistently run at around 10% to 11%, significantly higher than the 9% that was normal pre-2020. For whatever reason, Wall Street continues to underappreciate this new aspect of corporate America.

Although earnings from America’s biggest companies have so far weathered tariffs, those levies are just getting started. Corporate executives knew well in advance that if Trump won the election in November 2024 he would implement tariffs and they planned accordingly. Will earnings grow just as impressively when the full average tariff rate of around 20% goes into effect and companies run through existing inventories? And will companies be able to pass on those costs to customers, preserving margins? Such concerns are reasons why economists expect the economy to decelerate sharply this quarter and the final three months to be right around stall speed — or worse.

It may be a cliche, but it’s true that the stock market isn’t the economy — and it’s probably truer than ever now as the advent of AI promises to remake the economy, fueling the optimism of equity bulls. It’s also true that there’s never been a time when stocks managed to blissfully ignore an outright recession, if that’s where things are headed. The exuberance in the S&P 500 runs into a reality check by way of the Russell 2000 Index of smaller companies, where second-quarter earnings are poised to generate just 2.7% growth, barely covering the rate of inflation. Privately-held small businesses may be struggling even more, because they completely lack the access, scale and negotiating power that have buoyed their publicly-traded peers. According to an estimate by the right-leaning US Chamber of Commerce, small businesses will have to pay an extra $202 billion a year on tariffs, which works out to about $856,000 per company on average.

The S&P 500 at a record high may empower Trump to further challenge economic orthodoxy in ways that are truly bad for business that he can’t easily walk back. Thankfully, America’s top companies have found ways to weather the Trump headwinds. And they may find ways to keep doing so, if you believe the numbers.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin