Goldman Sachs Group Inc. is looking to capitalize on helping private equity clients saddled with bets they can’t exit.

The bank’s asset-management arm is raising some of its biggest funds to help cash-strapped private equity firms and portfolio companies. Many of those firms have struggled to return cash to investors in a muted environment for mergers and initial public offerings, and are trying to ease that liquidity logjam.

Goldman is now approaching investors to pitch a $10 billion fund offering combinations of debt and equity, known as hybrid capital, according to people with knowledge of the matter. Such funds essentially expand financing to companies owned by private equity firms that can then turn around and funnel the cash back to their parents in the form of dividends.

New York-based Goldman also has been in the market to raise $15 billion for the latest iteration of its flagship secondaries fund, some of the people said. That vehicle will invest in private equity stakes and continuation vehicles, a popular tool that reworks assets to allow firms to hold their investments for longer.

“There’s a lot written about continuation vehicles but not about the hybrid-capital side,” Marc Nachmann, head of asset and wealth management at Goldman Sachs, said in an interview. “Hybrid solutions allow portfolio companies the creation of dividends upstream. That’s why we see hybrid capital as pretty interesting right now.”

He declined to discuss specific plans for Goldman funds in the space.

Like a $15 billion hybrid-capital fund the company raised in 2021, the new vehicle will offer financing instruments that provide the flexibility of equity with the structure of a loan, and which can often be converted to equity.

The asset manager’s push deeper into hybrid capital is yet another sign of investors trying to untangle snarled bets in a dealmaking environment that’s been hampered by political and economic uncertainty. Such funds essentially expand financing from private-credit firms to troubled private equity firms who want to keep increasing their investments or send more back to their investors in the form of dividends.

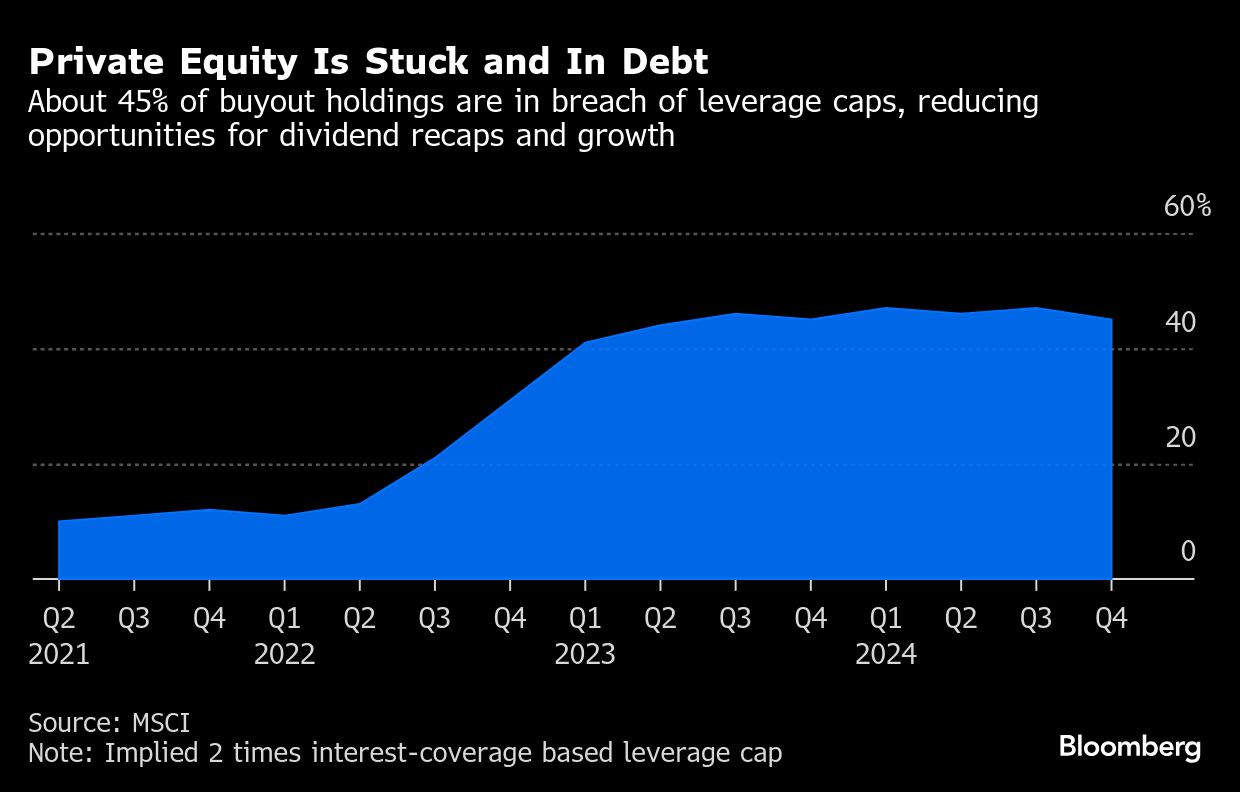

Portfolio companies at buyout firms globally are caught in a leverage squeeze as exits and financing become more challenging, boosting the demand for options. The squeeze could put more strain on distributing profits to limited partners and “throttle portfolio companies’ expansion, which may pressure exit valuations later,” according to a June report by MSCI Inc.

In total, Goldman counts $151 billion in private-credit assets, though more than half are non-fee-earning assets such as those on its own balance sheet or unfunded commitments from investors. The bank expects to reach $300 billion of private-credit assets by the end of 2028.

Goldman is hardly alone in the hybrid-capital space. Carlyle Group Inc.’s AlpInvest, which has about $97 billion of assets under management, has raised over $4 billion for its portfolio finance platform. Eldridge Capital Management — a subsidiary of the $70 billion asset manager Eldridge — is also pitching a similar fund.

Goldman is also telling investors it can offer quick-turn financing to cash-strapped investors by moving stakes in private equity funds into special-purpose vehicles, offering pricing with greater guarantees than they might get in a normal secondary sale.

Private equity’s thorny problems are also pushing the sector’s more complacent investors to focus on improving the productivity of their companies, rather than just sitting back and waiting for valuations to grow.

“There are definitely people out there who have a reputation for value-add operating improvements and have done that for a long time,” Nachmann said. “There are others who had a history of leaving the companies alone and counting on multiple expansion.”

Ultimately, Nachmann said, the tougher environment may compel private equity investors to think harder and more creatively about improving the companies they buy. “It is a good thing for the economy to improve the productivity and the return on capital in the existing asset,” he said.

Nachmann also oversees Goldman’s own $212 billion private equity business, which focuses on mid-market and asset-lite opportunities in sectors such as services and software. His private equity arm, he said, has avoided the mistakes made by those its private credit arm is now helping to bail out.

“A lot of private equity firms counted on one way out, which has created a backlog,” Nachmann said. “We’ve been always focused on having multiple ways out.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Todd Gillespie, Preeti Singh, Sridhar Natarajan