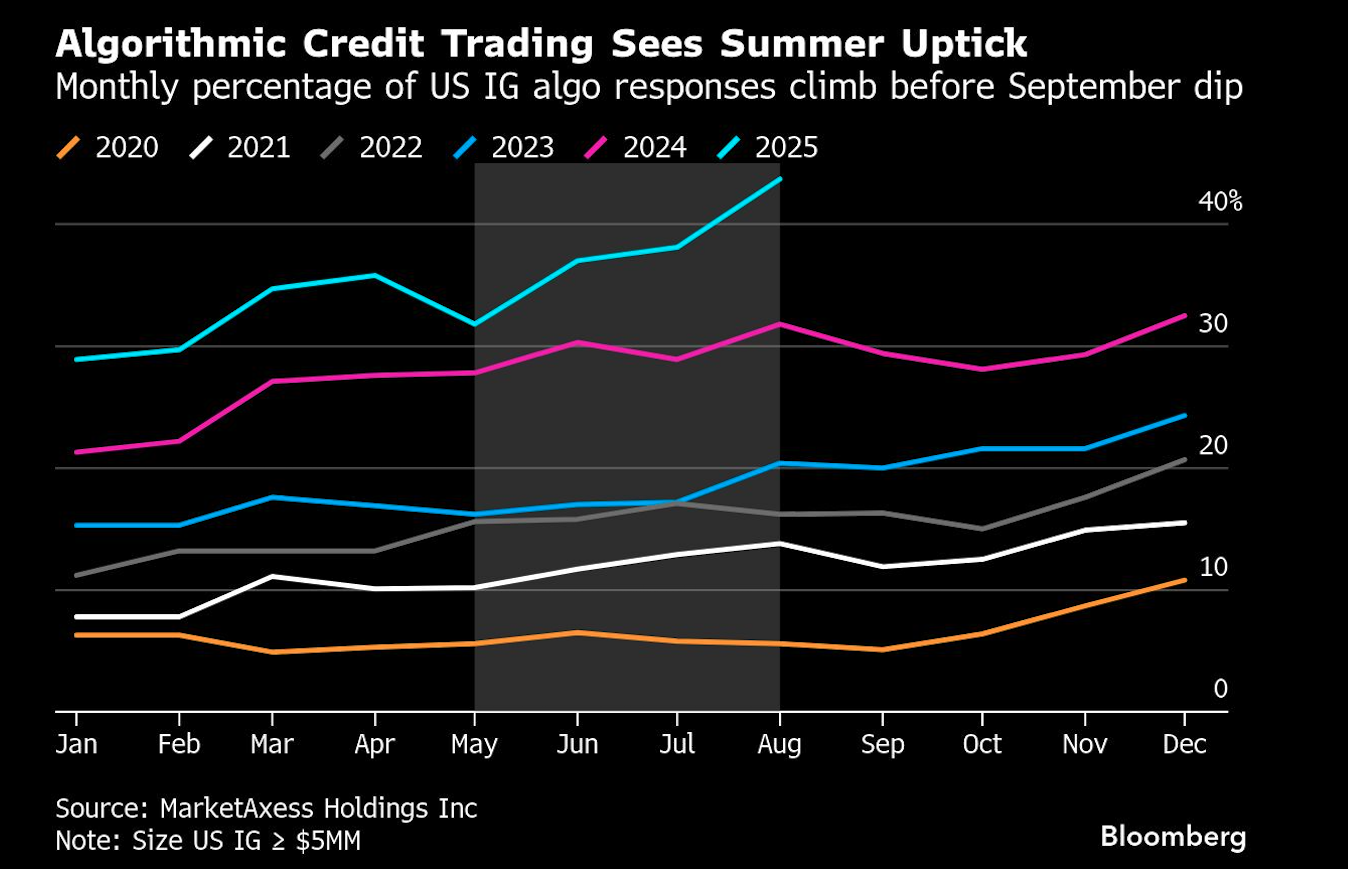

In August, as US credit traders go to the beach, algorithms are increasingly stepping in for them, allowing transaction volume to stay relatively high even during a traditionally slow period.

Algorithmic trading accounted for more than 40% of trading in the US high-grade market in August, a percentage that has climbed steadily since that month in 2020, when it was less than 10%, according to data from MarketAxess Holdings Inc., an electronic trading platform. In the last four years, algo activity usually dipped in September and picked up again in the last three months of the year, underscoring how automated trading helps to sustain volume — particularly in block sizes — during the summer and year-end holiday periods.

Credit traders are increasingly relying on algorithms, decades after they began dominating equity markets, and they have become reliable stand-ins when activity would normally sag. The result has been smoother markets with less volatility and lower trading costs. And for companies, it means more flexibility to sell bonds outside of traditional borrowing times.

“Algorithms are pushing the frontier — broadening coverage, smoothing liquidity and sustaining market presence through both turbulent and traditionally slower periods,” said Julien Alexandre, global head of research at MarketAxess.

August, historically seen as a relatively quiet month for US corporate bond trading, has been accounting for a growing share of annual volume, particularly in the high-yield universe, according to Tradeweb Markets Inc. data compiled by Bloomberg Intelligence’s Brian Meehan. While the share of investment-grade debt hasn’t grown as much, the broader picture is clear: August may no longer be a market dead zone.

While it’s too early to measure the month’s growth against the entire year, August has accounted for about 8% of annual volumes from 2022 to 2024 — up from around 6% to 7% in the four prior years, according to a July report from Barclays Plc analysts Zornitsa Todorova and Andrea Diaz Lafuente. There’s a similar uptick in holiday-packed December.

“The August shift marks a clear flattening of seasonal effects in credit markets,” they wrote, pointing to rising automation and algorithmic execution. Even the so-called Friday effect — where quieter trading volumes marked the end of the work week — has faded, with trades now on par with other weekdays.

Credit trading still shows seasonal slowdowns, driven in part by reduced primary issuance around holidays such as Thanksgiving in the US and longer summer breaks in Europe.

“There will always be some degree of seasonality, but we’ve already seen it smooth out,” said Sam Berberian, global head of credit trading at Citadel Securities. “That trend should accelerate as credit algos become more capable and a greater share of flows migrate to electronic execution.”

That acceleration is already evident. In the investment-grade market, nearly half of credit trading is now electronic, up from just 30% in 2018, the Barclays analysts noted. Electronic activity spikes over holiday periods like August and December — with August’s electronic share consistently five to 10 percentage points higher than in other months from 2018 to 2024.

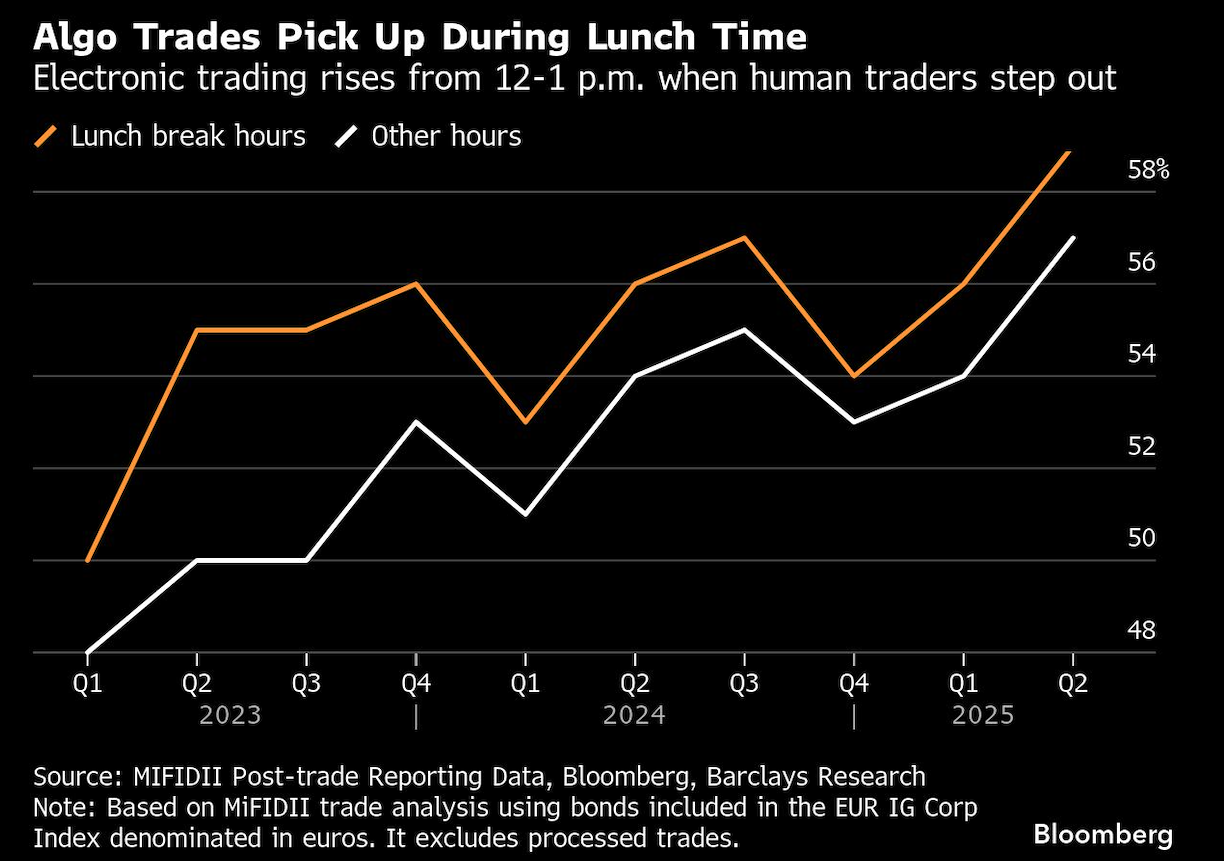

Automated tools also pick up the slack during lunch time. Barclays found that electronic trading between noon and 1 p.m. in Europe is about five percentage points higher than in any other hour, based on post-trade reporting data. Analysts believe the trend is similar on the other side of the Atlantic.

Portfolio trading — a newer technique that allows investors to buy or sell baskets of securities in one fell swoop — has also gained traction during those typically quiet months. Since 2023, December’s share of high-grade portfolio trading has been five percentage points higher compared to the average share in October and November, according to Barclays, further reinforcing the idea that systematic trading desks are stepping in when voice trading slows. This, in effect, also drives down execution costs.

“Historically, it’s been more expensive to trade during seasonally slow months due to thinner liquidity,” said Berberian. “But electronic and portfolio trading are driving the steepest reductions in costs and the biggest improvements in liquidity precisely during those periods.”

Mark Clegg, a senior fixed income trader at Allspring Global Investments, sees the same pattern. Portfolio trading, he notes, has helped smooth volumes when traditional liquidity thins during holiday months.

“This sure beats moving risk via block voice trades and hunting down beach-bound traders in both of those months,” he said. “If you are in a buyside seat and working with backup sales and a backup trader, costs to execute rise like the August heat index.”

A message from Advisor Perspectives and VettaFi: Transitioning your financial advisory business? Read our latest articles for guidance on launching an RIA, switching firms, or specializing.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Isabelle Lee, Caleb Mutua