The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.

Clients work a lifetime for financial freedom. Once retirement comes, they often have a large nest egg to spend. However, there can also be a huge fear of spending the portfolio down. In a recent Morningstar Longview podcast, Vanguard CEO Salim Ramji stated.

One of the hardest problems, though, is just helping clients get over the anxiety around it. I mean honestly some of the most both heartbreaking and inspiring calls that I’ve been on at Vanguard have been clients who are in retirement, who have saved wealth, who have adhered to all of the Vanguard principles over 20, 30 years, and they’re just not spending what they should, and they’re not living the life and retirement that they should afford.

A recent paper by researchers David Blanchett and Michel Finke found that retirees don’t like spending down their wealth (principal). The paper, titled Retirees Spend Lifetime Income, Not Savings, found that retirees spend a much higher percentage of their annuitized income and spend about half the amount that they could safely spend from non-annuitized wealth. It’s actually quite difficult for savers programmed to build a portfolio to suddenly start spending down that portfolio.

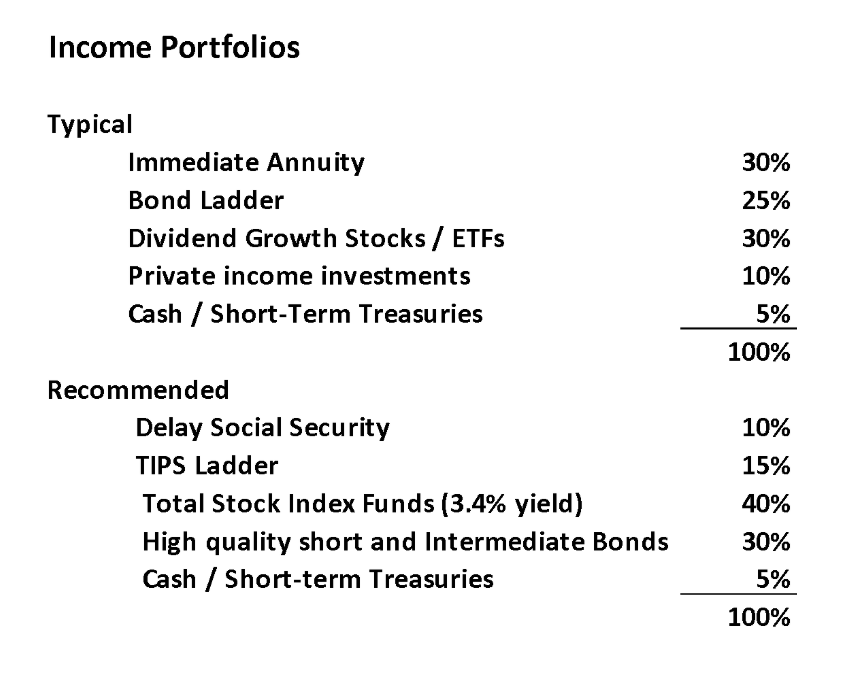

Let’s first examine the typical income portfolio and the associated problems I see with such solutions. Then I’ll propose an income portfolio I built for myself and use for others. Below shows just how different these income portfolios are, both using a 40% stock and 60% fixed income allocation, though this can vary greatly, depending on the client’s situation.

Problems With Conventional Income Portfolios

A conventional income portfolio might include a combination of the following assets, most of which I am wary of, for a $1 million portfolio.

Immediate Annuity: The immediate annuity solves the emotional problem of spending, since a predictable nominal cash flow has been purchased. In this case, 30% of the principal has been exchanged for lifetime cash flow (principal and interest) for the rest of the client’s life. The mortality credits provided by the insurance company assure the payments for life, freeing the client to spend this money more freely.

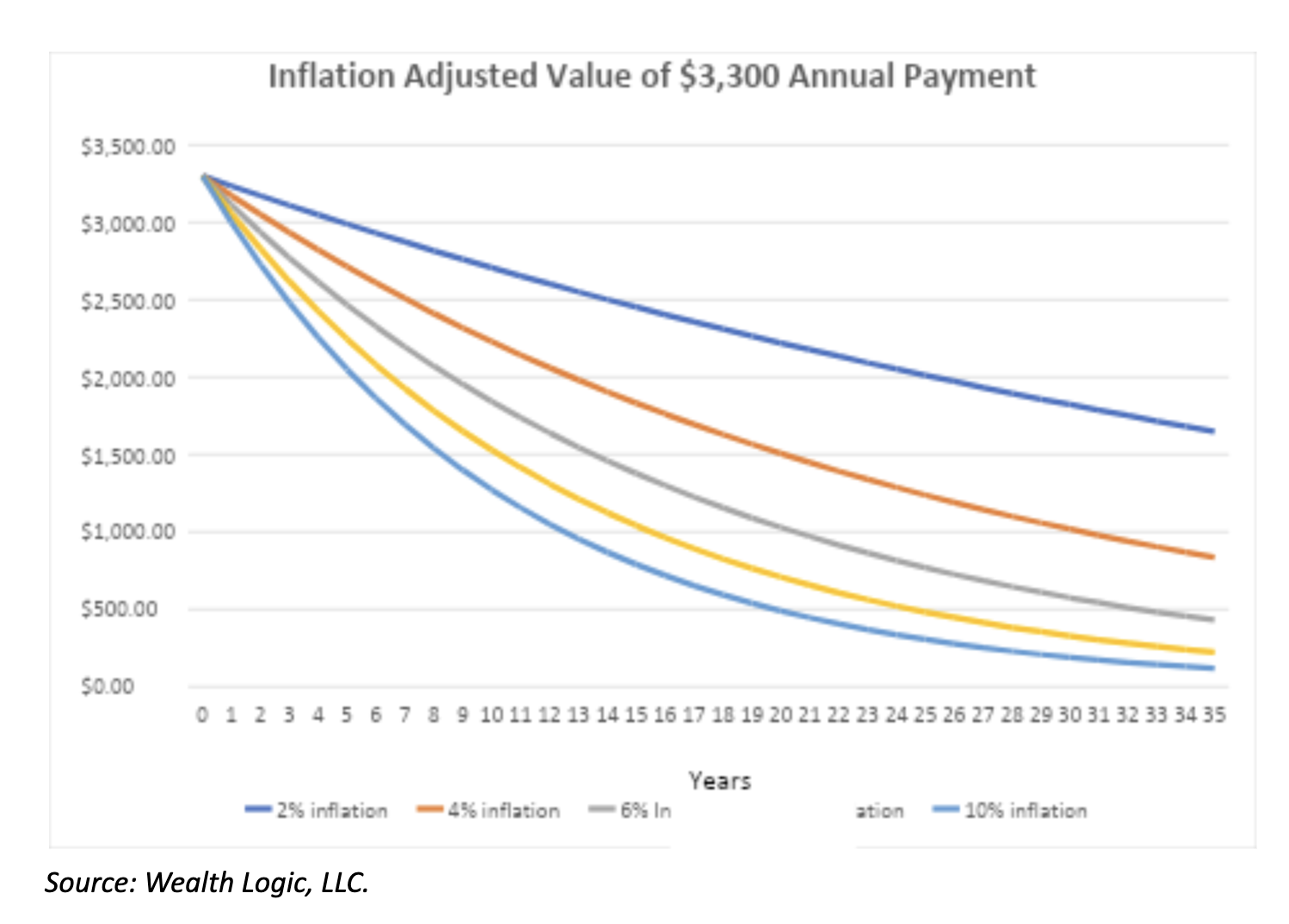

While this provides some psychological freedom to spend, it creates inflation risk that may be far more costly than having a longer-than-average life span. The chart below shows the spending power of a $3,300 annual annuity. Inflation could make that lifetime cash flow virtually meaningless. In my opinion, inflation is a greater risk than longevity. While annuities with fixed COLAs increase spending power over time, Blanchett points out that they actually increase inflation risk. In short, if actuaries aren’t allowing their insurance companies to accept inflation risk, I’m not going to recommend them. In Bill Bernstein’s words, clients play Russian roulette with inflation.

Dividend Growth Stocks/ETFs: Dividend stocks provide cash flow. I believe in diversification, so I look askance at a fund like the Schwab US Dividend Equity ETF (SCHD), which owns about 100 stocks. Morningstar shows it has an SEC yield of 3.74%, which is well over twice the dividend yield of the S&P 500.

Although I don’t know the future, dividend funds are value, and value has far underperformed the market. Owning the entire market has less risk. In addition, this is a tax-inefficient solution, since dividends can be taxed as high as 20%, plus the possible 3.8% investment income tax, plus the possible state income tax.

Private income investments: The vast majority of private investments I’ve seen start with so-called high income, and then that is dramatically cut, along with principal. They typically have high distribution costs, meaning they have to be sold.

Bond Ladder & Cash/Short-Term Treasuries: A high-quality bond ladder or bond fund combined with some high-yielding cash or short-term Treasury bonds may be appropriate.

A Better Income Portfolio

Income portfolios I build for others (and myself) must have a reasonable amount of inflation protection and be low cost. Generally, I take the measures outlined below.

-

Purchase inflation-adjusted cash flow for life: The single best solution to keep up with inflation is increasing Social Security. I reframe the way a client thinks about this decision. Say the client is 66 and can take $26,244 in annual Social Security benefits now or may collect 32% more if she waits another four years. If inflation averages 2% annually (the Federal Reserve’s target), then she will be giving up $108,167 by waiting, and that’s a lot of money. But by waiting, she will be getting an additional $9,090 in benefits annually beginning at 70, and that will increase with inflation.

-

Build a period-certain inflation-adjusted cash flow for life: Before recommending to clients, I first built a TIPS ladder for myself. Recently, a 30-year TIPS ladder can provide a real (inflation-adjusted) 4.55% safe withdrawal rate. While there are no mortality credits (to mitigate longevity risk), it essentially eliminates inflation risk. And, unlike Social Security, the ladder can be inherited by non-spousal beneficiaries. LifeX and Northern Trust both have introduced self-liquidating TIPS ladder ETFs. However, payments decrease over time rather than provide a constant real cash flow with certain spending power. My challenge to the ETF industry remains unmet.

-

Buy a tax-efficient stock income portfolio: The S&P 500 dividend yield is a paltry 1.31%, according to S&P Dow Jones Indices. That’s obviously not much income. Yet I argue the yield is 3.30% when you combine it with the stock buyback yield. One must reframe the way a stock buyback works. Say XYZ corporation paid the 3% in dividends; all would be taxable. But if it repurchased 3% of its shares and you sold the same 3%, you’d own exactly the same proportion of XYZ had it paid in dividends. The only difference is you get a lower tax bill, since there is basis in your shares and, unlike dividends, you only pay taxes on the gains.

There is some evidence that small- and midcap stocks are repurchasing shares at the same rate as the S&P 500. International companies are also buying back shares. As a result, the tax-efficient stock income portfolio is often a total U.S. and total international stock index fund, creating income by selling the same proportion as the stock buybacks.

-

Use high-quality short- and intermediate-term bonds (or CDs): As much as I love TIPS, I’m not willing to put all of anyone’s eggs in any one basket. And because I fear inflation, I’m not willing to go long-term. Even intermediate-term bonds lost over 13% in 2022. If an investor is in a high tax bracket, I’m willing to include up to 20% of fixed income in a low-cost high-credit muni bond fund.

-

Park some high-earning safe cash: While this may change soon, a Treasury money market fund is yielding 4.20% as of September 8, 2025. So, especially if your client lives in a state that has high taxes, there is little to no penalty versus. bonds.

Conclusion

Both of these portfolios have 60% cash and fixed income and 40% riskier assets (public equities and private investments) though I would argue the typical conventional income portfolio has far more risk with lower expected real income. The recommended portfolio has 25% of the assets protected from inflation (10% from delaying Social Security and 15% from the TIPS ladder).

Granted, some reframing must be done to educate the client that delaying Social Security is the same as buying an inflation-protected lifetime annuity and that stock buybacks are far more efficient than dividends. I’ve found clients embrace these concepts once they understand them.

The cash flows from the portfolio are a license to spend and will allow the client to better enjoy their retirement.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multibillion-dollar companies and has consulted with many others while at McKinsey & Company.

A message from Advisor Perspectives and VettaFi: Interested in learning more about how bond ETFs can help diversify your portfolio? Click here to read more.

Read more articles by Allan Roth

The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.