Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Summary

- Most target date funds (TDFs) do not follow academic lifetime investing theory, exposing retirees to more risk near retirement than theory recommends.

- Academic research and the Federal Thrift Savings Plan recommend 70–80% risk-free assets near retirement, but most TDFs are 90% risky assets.

- TDF providers justify higher risk due to inadequate savings, but this contradicts the scholarly guidance they claim to follow.

- Baby boomers should exit TDFs and move to T-bills and TIPS now, as a market crash could devastate retirement savings due to sequence of return risk.

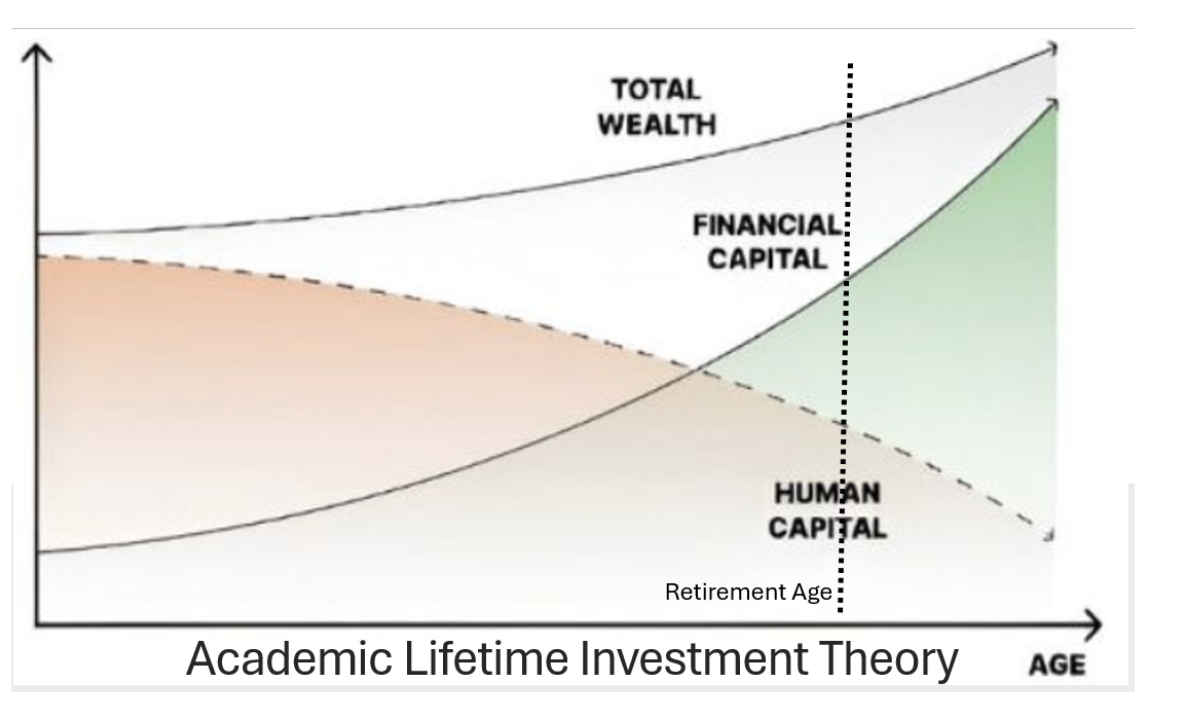

Target date fund (TDF) providers say they follow the academic theory of lifetime investing. As human capital (present value of all wages) depletes, we rely more and more on our accumulated financial capital (our savings). That makes sense.

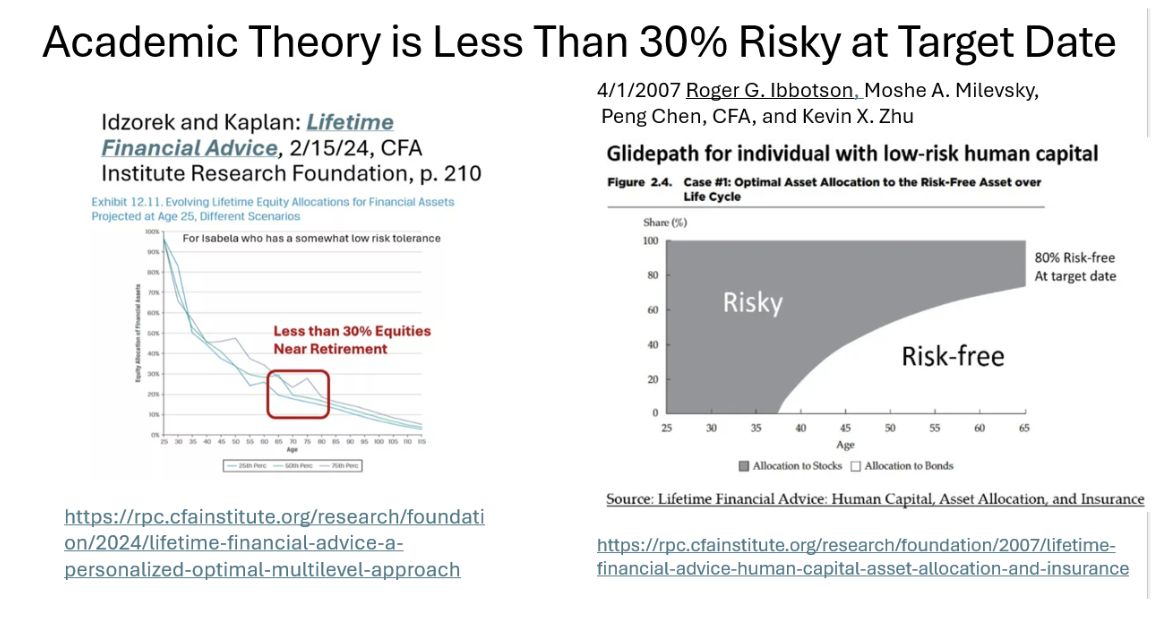

Thomas Idzorek and Paul Kaplan, in 2024, revisited the findings of a 2007 article by Robert Ibbotson, et. al titled “Lifetime Financial Advice: Human Capital, Asset Allocation and Insurance.” In “Lifetime Financial Advice: A Personalized Optimal Multilevel Approach,” the authors recommend risk-free allocations near retirement be at 70%, a revision from Ibbotson’s previously recommended 80%.

The theory is very safe for people near retirement, allocating less than 30% to risky assets, as shown in the following excerpts from the two studies:

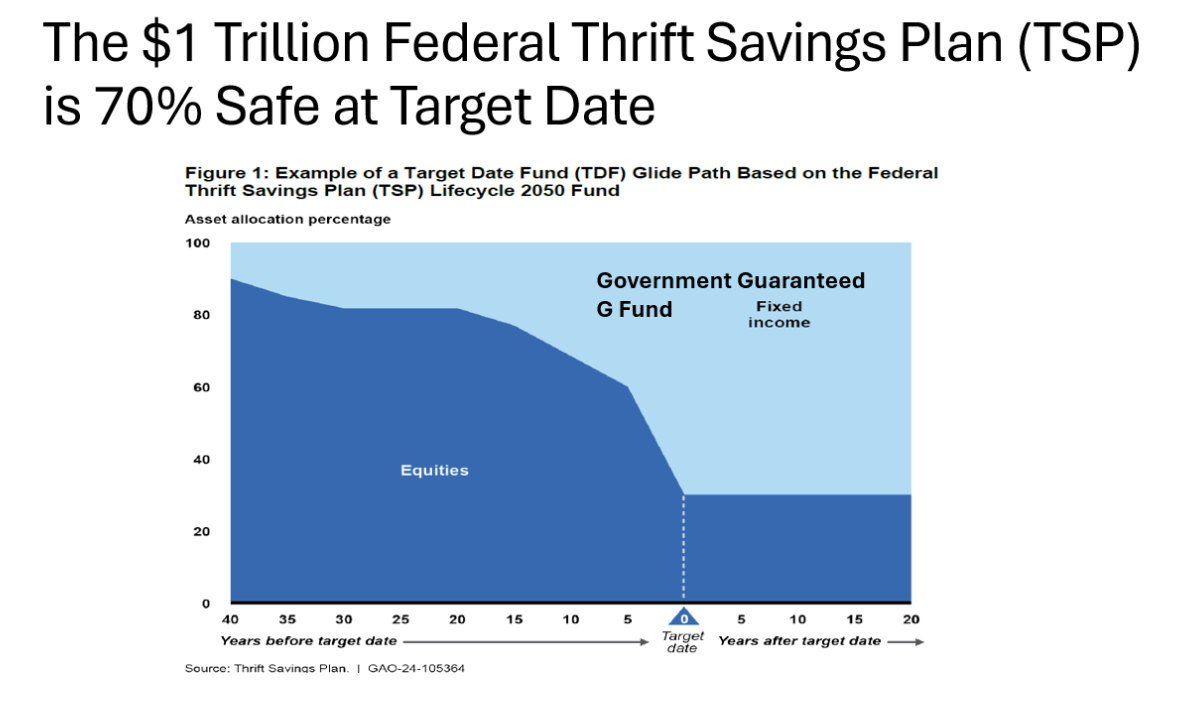

The theory is put into practice by the largest savings plan in the world. The $1 trillion Federal Thrift Savings Plan follows a glidepath that puts it at 70% risk free at its target date.

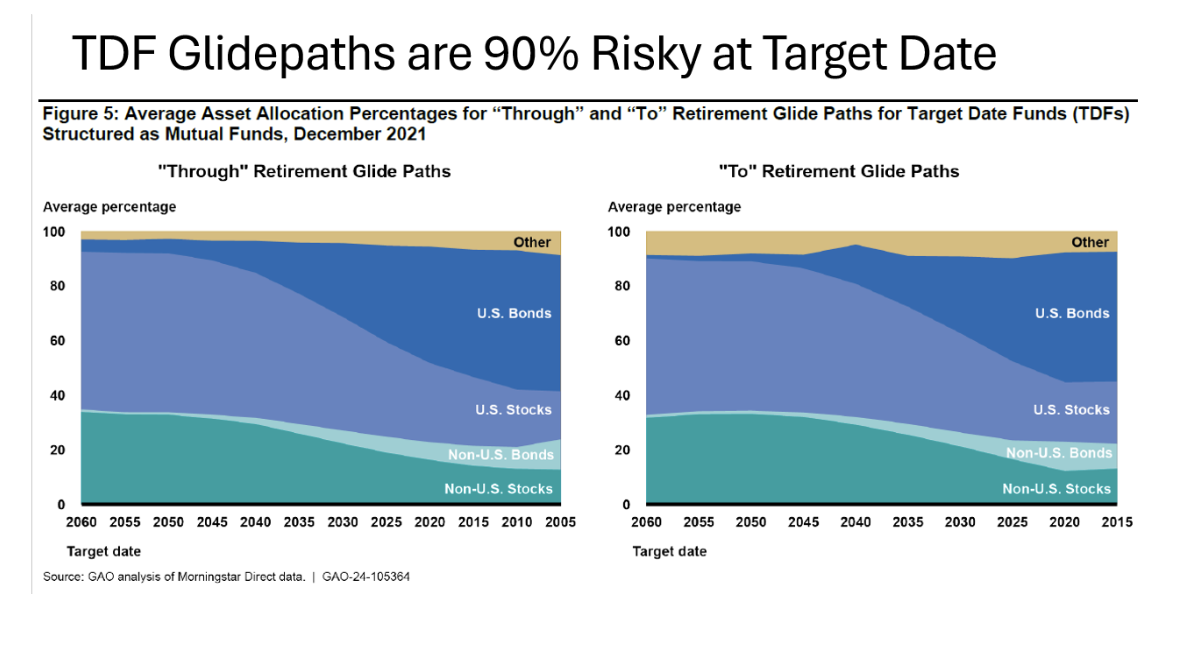

However, the rest of the TDFs, representing $4 trillion in assets, do not follow the theory, even though they say they do. They are 90% risky at their target dates, with 50% in equities and 40% in risky long-term bonds:

TDFs Are Riskier Than They Admit

TDF providers say it’s because people have not saved enough so they need the “medicine” of risk. At the same time, they say that they follow academic theory. But that’s impossible, since they can’t do both. As things currently stand, high risk has worked for the past 16 years, because it’s been the longest bull market ever.

But Stein’s Law will hold — if something cannot go on forever, it will end. There will be a stock market crash that will change everything. Can $4 trillion in TDFs be wrong? Stay tuned.

Conclusion

Baby boomers are in the Retirement Risk Zone when sequence of return risk is a threat. The next crash could ruin their financial security for the rest of their lives. The problem is that TDFs will not change until and if there is pressure to change. This could happen after the next crash, but it will be too late for boomers. In 2008, TDFs for those near retirement lost more than 30%, prompting the first and only joint hearing of the SEC and Department of Labor, but nothing changed.

This time $4 trillion is in play, much more than the $200 billion in the TDF industry in 2008. When the next crash comes, inevitably there will be an uproar. Baby boomers must not wait for that uproar. They need to get out of their TDFs now and move to the safety of T-bills and TIPS, following the guidance of academic theory. That’s just the smart thing to do.

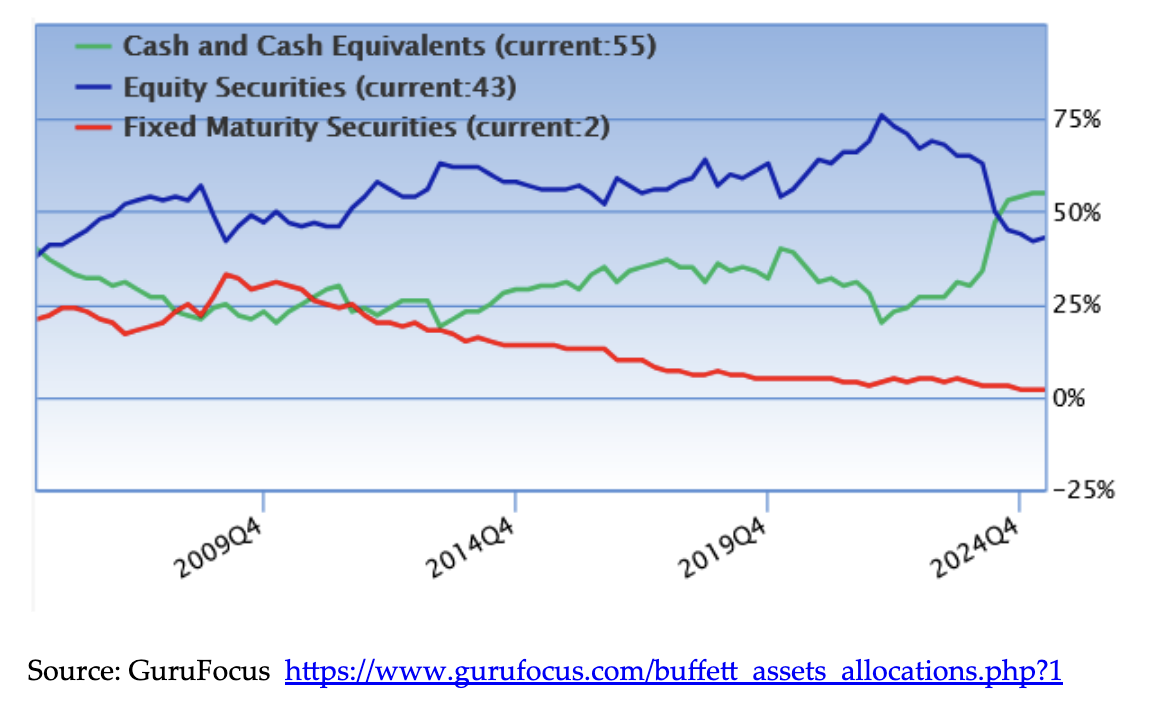

The need for safety near retirement is currently reinforced by a bubble in the U.S. stock market that has led Warren Buffett to increase Berkshire Hathaway’s cash (not bonds) exposure to the highest it has ever been.

Ron Surz is president of Target Date Solutions, developer of the patented Safe Landing Glide Path and Soteria personalized target date accounts. He is also co-host of the Baby Boomer Investing Show. Surz’s passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book, “Baby Boomer Investing in the Perilous 2020s,” and he provides a financial educational curriculum.

For anyone who relies on TDFs — or advises those who do — Surz’s new book is a must-read guide to understanding the risks, solutions, and future of a secure retirement.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Ron Surz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.