Protection Without Compromise: The Surprising Evidence About Inflation-Focused Equity Strategies

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Many advisors avoid allocating to inflation-protecting equities, fearing the age-old rule that protection comes at a price. However, my recent research with my colleagues Giovanni Bruno and Ben Luyten at Scientific Beta suggests this industry-wide fear is unfounded: Inflation-hedging stocks perform just as well as their inflation-sensitive peers.

Does Protection Against Inflation Shocks Come at a Cost?

Recently, investment practice has shown growing interest in equity strategies that emphasize stocks with favorable sensitivity to inflation. A host of equity indices and exchange-traded funds promising inflation protection have been launched. For investors considering such strategies, a crucial question is whether such equity portfolios incur a cost in the form of lower expected returns.

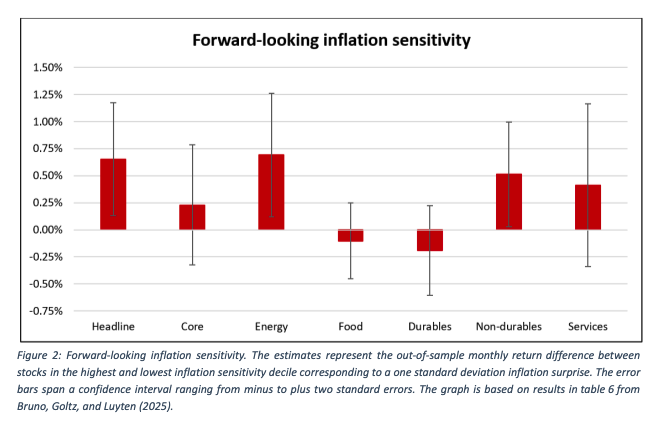

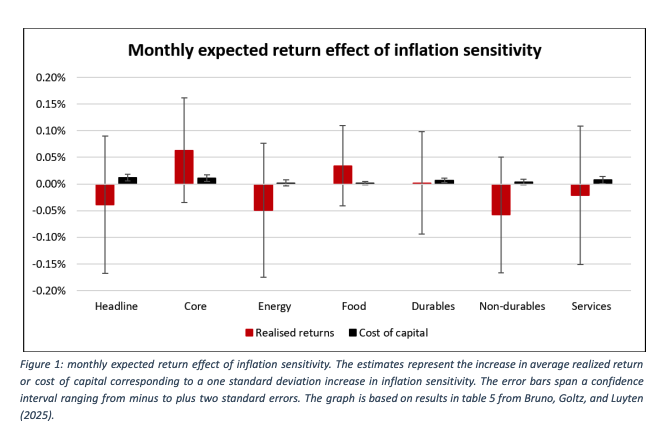

In our detailed empirical analysis of this question, we go beyond headline inflation and analyze more granular components such as core, energy, or durable goods. Furthermore, instead of simply documenting the realized returns for portfolios that offer inflation protection, we provide an additional set of test results based on forward-looking cost of capital estimates, which are widely used in the accounting literature. Since realized returns contain noise specific to the historical sample, combining both sets of results can lead to more robust conclusions.

The results are easy to summarize: We find no evidence of an inflation protection cost in the form of lower expected returns when allocating across stocks. The average realized returns for stocks with the most and least favorable inflation sensitivity are not distinguishable from each other. This result holds for headline inflation and each of the inflation components we consider.

In addition, the difference between these two groups of stocks in terms of forward-looking cost of capital is very small. On average, there is no more than one basis point difference in monthly expected return between stocks with the most and least favorable sensitivity. Again, this holds when we look at both headline inflation and individual components. If anything, these results indicate that stocks that offer protection against inflation come with marginally higher expected returns.

Figure 1 presents these main results. Negative bars with a confidence interval fully below zero would indicate a cost of protecting against inflation shocks.

Why Inflation Protection Does Not Penalize Returns

Economic theory suggests that inflation protection should only lead to lower expected returns if inflation indicates bad times for the average investor. In other words, if positive shocks to inflation signal weaker future economic growth, protecting against inflation shocks within equity portfolios should be costly. This reflects investors’ willingness to pay more, and therefore accept lower expected returns, for stocks that offer protection against bad times.

Regarding headline inflation, our results suggesting the absence of a cost are in line with arguments made in other recent papers. Headline inflation does not reliably signal weak future economic growth. On the contrary, the relationship between inflation and future growth varies over time. Consequently, we do not expect to find an average cost when tilting a portfolio towards stocks with a favorable inflation sensitivity in the first place.