The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.

A fear appeal motivates the client by highlighting bad things that might happen if no action is taken.

A time-honored example: the tax hit that awaits the widowed survivor. As everyone knows, most tax brackets for singles are half as wide as those for married couples.

It follows that the widowed survivor will pay twice as much in tax and live only half as well if something is not done.

Perhaps a Roth conversion? Maybe a life insurance policy whose payout will be tax-free? Mr. Client, you have got to get ahead of this looming tax hit. It will be too late after your demise. Your poor widow will suffer needlessly.

Does this fear have a rational basis, or is it just a sales pitch, cleverly designed to tap into client emotions, exploit the human incapacity to do the math, and leverage the widespread innumeracy of our age?

This is gendered territory, for this fear targets husbands, of the traditional breadwinner cast, who are its preferential target. Our numerical analysis will be gender-neutral, but that doesn’t change the social facts about how and against whom this fear appeal is deployed.

Math errors

Twice as much in tax? Live half as well? Really? It is true that single tax brackets are half as wide as the (lower) Married Filing Joint brackets. But to get a doubling in tax requires much more.

Let the tax rate in each successive bracket be twice as high — say 10% at the bottom, 20% at the next bracket, and 40% at the top bracket. Second, assume all brackets are the same width in dollars, with single brackets half as wide. Given those criteria, if a married couple was at the bottom of the 20% bracket, then upon the demise of one member, with no change in income, that would put the survivor at the bottom of the 40% bracket. And for a married couple in the middle of the 10% bracket, the demise of one member would leave the survivor in the middle of the 20% bracket. Ouch.

But that rubric does not describe the U.S. income tax system circa 2025. Relative to that clean model with equal bracket sizes and rates increasing two times per bracket, the actual U.S. income tax structure is a hot mess. Brackets vary in width. Tax rates in adjacent brackets increase in highly irregular amounts: +2% here, +10% there.

That means we have to calculate, case by case, the increment in tax paid by the widowed survivor. It will vary according to the couple’s income level and how much income disappears on the first death; overlays like IRMAA and the Social Security tax torpedo complicate the picture. No simple rubric suffices to estimate how much more tax the survivor might have to pay.

Case Study

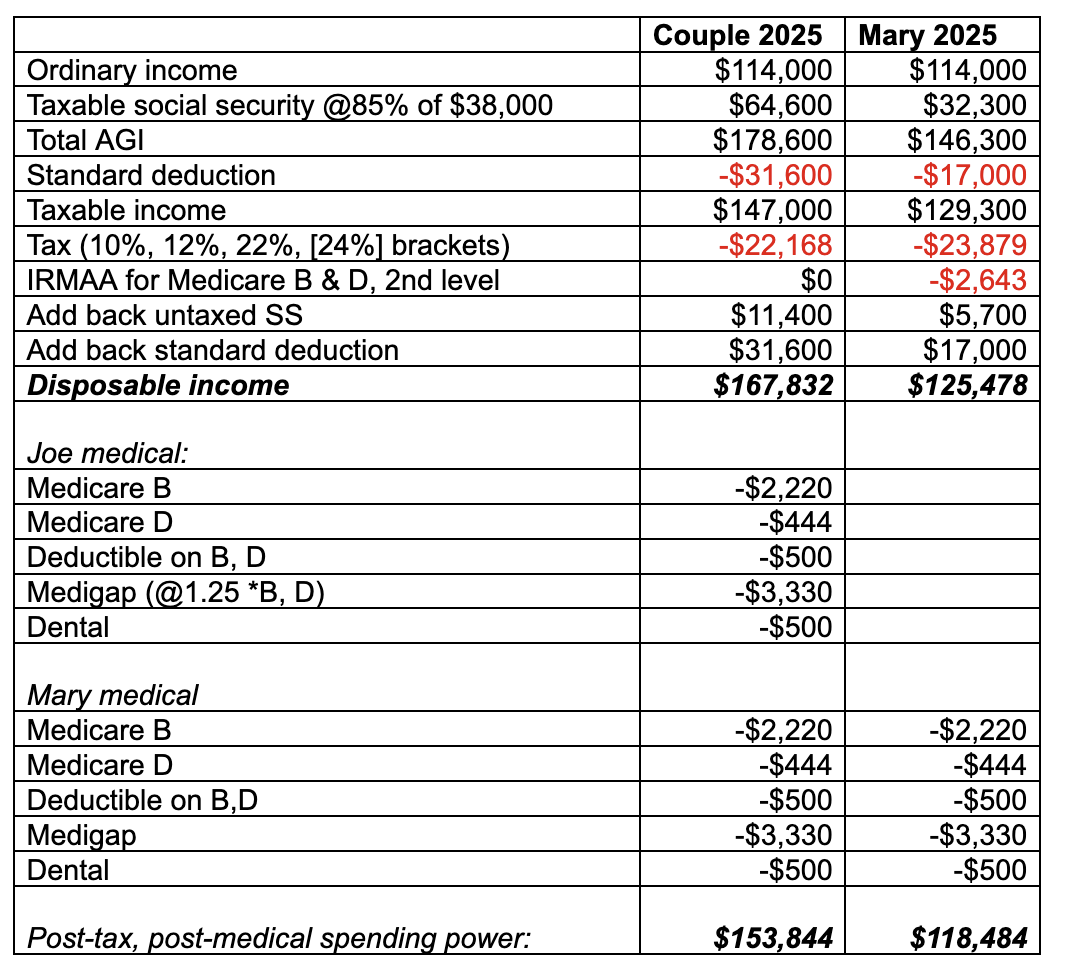

Allow us to introduce Uncle Joe, married to our blessed Aunt Mary. Joe is a paragon of thrift beyond anything you can imagine. He owns two coarse woolen robes and a pair of sandals made out of recycled tires that he replaces once a year. He does not drink, smoke, or use caffeine. He takes a small helping each meal of whatever Mary eats; she purchases no food for him. He’s bald and uses whatever bar of soap he finds in their shower to bathe. He has no hobbies, never travels, never drives. He reads what Mary reads and watches what Mary watches. Joe spends literally nothing on a daily basis. He’s busy meditating.

With one exception: Joe has Medicare B, Medicare D, a supplemental Medigap policy and a dental plan. Also, Joe was not always a monk in a robe. He receives the same Social Security income from past employment as Mary, and their two SS payments together account for 40% of family income, with the rest coming from RMDs and other ongoing income not dependent on the life of either.

If Joe dies first, we have the pure case of the tax transition from couple to single: No spending goes away upon Joe’s death other than medical outlays, and the drop in income is modest, no more than Joe’s Social Security. Mary retains 80% of the couple’s income while 100% of the discretionary lifestyle spending continues — it was all hers anyway, except for Joe’s medical expenses.

How much of a tax hit does Mary suffer upon Joe’s demise?

Tax Before and After Joe

Currently a good Social Security payment at full retirement age might be about $38,000. Their two SS payments adding up to $76,000 were stipulated to be 40% of income, making total income equal to $190,000. After Joe’s demise, and the removal of his Social Security benefit, Mary’s gross income will be $152,000.

Note how affluent we’ve made these two, with tax-deferred accounts about $2.5 million (to get the $114,000 of income not dependent on either life, corresponding to RMDs at about age 78).

Here is the income tax statement for the couple while Joe is alive and for Mary with 80% of the income after Joe passes. For simplicity we’ve used 2025 rates (pre-OBBB) for both cases, even though Mary won’t be taxed as a single until the following year.

Even better: The couple was not subject to IRMAA, but Mary will be. Tax hit gone wild!

Except not. Mary pays a grand total of $1,711 more in income tax, consequent to being in the next tax bracket up, at 24%. Plus she pays over $2,600 in extra Medicare taxes, having traversed the IRMAA # 1 and IRMAA #2 thresholds. Arggh!

But with Uncle Joe no longer with us to have medical expenses, she saves about $7,000.

Without Joe’s Social Security she’s lost $38,000 of income, but her post-tax, post-medical income has dropped by a bit less than $35,000. There’s certainly a loss of income for Mary after Joe’s demise — but where is the “tax hit?” Mary will have to tighten up a little bit, with a single discretionary income of $119,000 versus the previous $154,000. But that’s lost income, not some diabolical element of the current tax structure.

Uncle Jerry

Aunt Mary resolved to divorce Joe the day he came home wearing those recycled tire sandals. She’s currently married to a fellow named Jerry, with identical financials. Where Joe was a paragon, Uncle Jerry is a pretty normal guy. He drinks wine, dines out, and still has most of his hair. He likes to grill steak and salmon on the back deck, and is fond of fine cheese, fresh berries, and artisan bread. He doesn’t spend much on clothes, but he does have a laptop, a smartphone, a tablet, and headphones, which he updates regularly. He and Aunt Mary like to travel.

Aunt Mary will miss Uncle Jerry — a bon vivant and a gentle soul — terribly when he’s gone. But she won’t have to fund his discretionary spending anymore, which looks like this:

Food at home $5,000; wine at home $5,000; lunches and dinners out, Jerry share $3,500; amortized phone and gadgets $1,500; personal care $1,000; clothing $1,000; Jerry’s cost, one vacation, $3,000.

That’s $20,000 not spent on Jerry’s demise, with another $10,000 in amortized costs for the Toyota Camry he replaced every five years.

With her lost income balanced by absent spending, Aunt Mary will have almost as much discretionary income after Jerry’s passing as before. Where’s the tax hit?

***

The suspicious reader (the best kind!) will wonder whether we have carefully cherry-picked one of the few income combinations where the widow tax hit does not bite. Perhaps it spares only the affluent middle?

Elsewhere you can see how we investigated the tax hit at a selection of higher and lower income levels than for Jerry and Mary. We could not coax the tax hit to appear in any of those cases, either. At higher incomes, there was less likely to be a substantial increase in IRMAA for the single, or none at all; in the top brackets, there was as likely to be a widow bonus, because of the configuration of the highest single and married brackets.

At lower incomes, down in Social Security tax torpedo territory, there is no IRMAA for couple or single, and the absolute dollars paid in incremental tax are small, even as the dollar cost of medical insurance remains the same. No question but that some widowed survivors will struggle at these lower income levels, but the problem is always the sheer loss of income, not high tax rates.

It seems likely to us that there must be some corner case where the hit does occur, but we could not find one across a range of plausible scenarios. On the other hand, all our scenarios involved Social Security and Medicare B and D. Outside those two constraints — some state and local government employees do not pay Medicare B or receive Social Security — there may well be cases where there is a tax hit. However, these will be rare exceptions.

How Did the Widow Tax Hit Ever Become a Thing?

Behavioral finance teaches that humans depart from rational behavior in predictable ways. Notably, people are easy prey for the availability heuristic. Information which is salient, but perhaps partial and biased, drives reasoning. Single tax brackets below the top two are half as wide as married brackets. The availability heuristic pushes us to the incorrect belief that taxes must be twice as high on the single. And as we saw in the example, the widowed survivor did pay tax income tax at a higher rate, 24% not 22%.

Humans are cognitive misers: The ease of heuristics leads us away from the more difficult analysis of the expenses that disappear at death, most notably medical insurance, but also all the living expenses of a normal human spouse like Uncle Jerry.

Takeaway

Financial planners perform a valuable service by discussing with married clients what will happen if the income of one of them disappears upon death. But the focus should be on the adequacy of the remaining income to the spending needs of the survivor — not the change in tax rate from married to single.

William J. Bernstein is a neurologist, the co-founder of Efficient Frontier Advisors, an investment management firm, and a writer with several titles on finance and economic history. He has contributed to the peer-reviewed finance literature and has written for several national publications, including Money Magazine and The Wall Street Journal. He has produced several finance titles, and four volumes of history, The Birth of Plenty, A Splendid Exchange, Masters of the Word, and The Delusions of Crowds about, respectively, the economic growth inflection of the early 19th century, the history of world trade, the effects of access to technology on human relations and politics, and financial and religious mass manias. He was also the 2017 winner of the James R. Vertin Award from the CFA Institute.

Edward F. McQuarrie, Ph.D., is Professor Emeritus at Santa Clara University. He writes about financial history and its implications for retirement planning. Working papers describing his research can be downloaded here.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Edward McQuarrie, William Bernstein

The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.