How to Help Clients Budget for Long-Term Care

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

One of the most difficult expenses to plan for in retirement is long-term care (LTC). As …

- our population ages;

- our family sizes shrink;

- costs for LTC continue to outstrip inflation; and

- qualified caregivers become harder to find

… planning for this expense is likely to become more important both for advisors and clients.

Successful planning for future LTC expenses involves helping clients answer some or all of the following questions:

- Who in the household will need LTC?

- When will it be needed?

- What kind of care will be needed?

- Who will provide the care?

- How long will care be needed?

- How much will the care cost?

- What family assets will be used to pay for the care?

Most retirees self-insure or do not fully insure their future long-term care costs. Therefore, most retirees must set aside sufficient assets prior to retirement, or during retirement, to pay for such care when needed.

These funds will frequently be in addition to the funds set aside to cover the household’s expected essential and discretionary expenses during retirement, or desired amounts to be left to heirs after retirement. Therefore, funds dedicated to funding future LTC costs will generally reduce the amount the household can spend on other items (or leave to heirs). It is important, therefore, to address future LTC costs when developing a retired household’s overall decumulation plan.

In this article, I will discuss the process financial advisors can follow to help their clients determine how much they should initially set aside for LTC and how to periodically monitor whether the amount their clients have set aside (the reserve) continues to be sufficient in the future.

Background

According to a 2024 Northwestern Mutual report, of those needing LTC, the following is true:

- Many will need assistance for fewer than three years.

- Twenty-two percent will have a care need for more than five years.

- The average duration of care is higher for women (3.6 years) than for men (2.5 years).

- Among women, 64% are likely to develop a significant disability that requires daily help, and 26% of these women will need care for at least five years.

Because of the uncertainty with respect to LTC needs and durations, prudent planning for future LTC is similar to planning for a longer-than-expected lifetime in retirement. In both cases, the future is uncertain, and therefore, it will generally be necessary to plan conservatively.

On my website, HowmuchcanIaffordtospendinretirement.blogspot.com, I encourage financial advisors to periodically compare the present value (PV) of their client’s retirement assets with the PV of their spending liabilities to measure the household’s funded status.

Unlike other planning approaches that may ignore LTC costs or assume these costs will be met through insurance or from other assets, the actuarial approach encourages users to estimate the present value of these future uninsured expense liabilities just like any other expected future retirement expenses, include these amounts in the client’s annual spending liabilities and recalculate them periodically (generally annually).

Helping a client determine an estimate of the amount of their LTC reserve involves the following steps:

- Discussing with the client their goals and best-estimate answers to the LTC planning questions outlined above. This step may involve having the client engage in conversations with family members or others who may be future caregivers.

- Making assumptions about future LTC needs consistent with the client’s input and their tolerance for risk.

- Calculating the current reserve (PV) of the client’s LTC needs based on the first two steps.

- Periodically revisiting this process in subsequent years to ensure that the client’s reserve for LTC continues to be adequate

I will illustrate these steps with an example.

Example

John and Mary are both age 65, live in California, are in excellent health and are considering retirement. They meet with their financial advisor, Sally, to develop a spending plan/budget for retirement. They have two adult children and currently own a home with about $200,000 in equity. They currently have no LTC insurance and don’t have any assets specifically set aside for their LTC. Under the default assumptions in the actuarial financial planner (AFP), John’s lifetime planning period is 29 years and Mary’s is 31 years.

To start the discussion of relevant LTC planning questions, Sally shows them the Median Cost Data Tables at the Genworth Cost of Care website. This site shows median costs for various types of LTC for each of the states. They find that, for 2025, the median annual cost for assisted living in California is $88,200 and the median annual nursing home cost for a semiprivate room is $140,343.

John and Mary tell Sally that they would prefer to avoid relying on their children for as much of their LTC as possible, and they assume Mary will be the primary caregiver for John during his final years of life. With Sally’s help, John and Mary decide that they will plan on LTC consisting of two years of assisted living and one year of nursing home care (semiprivate room), which they assume will occur during the three years at the end of Mary’s lifetime planning period.

Based on the data for California care from the Genworth study, the average annual cost for two years of assisted living and one year of nursing home care (in today’s dollars) would be $105,581, but they expect that their annual recurring essential and discretionary expenses would be reduced during this period, so that the net annual cost would be about $70,000 (in today’s dollars) for the three-year period, which they assume will be just prior to Mary’s demise.

Sally, with input from John and Mary, agrees to assume that future LTC costs will increase by 4% per year (1% per year above the default inflation assumption), so today’s net expense of $70,000 will be expected to be $209,909 in future dollars 28 years from now, when they expect care to commence.

Sally enters the following amounts into row 41 of the actuarial financial planner for married couples:

The assumed cost starting in year 29 (the $209,909 annual cost in future dollars shown above) is determined by increasing the average current net cost of $70,000 estimated above with Sally’s estimate of annual increases in LTC costs of 4% per year for 28 years ($70,000 X 1.04 **28). The annual rate of increase of 4% entered in the spreadsheet applies for the years once payments are assumed to commence.

They determine, for their planning purposes, that these LTC expenses are not expenses they can simply reduce or eliminate if they choose to (i.e., nondiscretionary), so they classify them as “100% essential.” This choice affects the aggressiveness of the investment of their LTC reserves (relatively safe) and the discount rate used in the PV calculations (a 5% discount rate).

The AFP determines the present value of this assumed stream of payments under the default assumptions and the information inputted to be $159,100 (with the result found in the PV calcs tab of the AFP spreadsheet).

John and Mary’s LTC reserve of $159,100 is based on:

- Their ages

- The level of LTC they chose to fund

- The assumptions they and their financial advisor selected

Varying any or all of these items would produce a different reserve value.

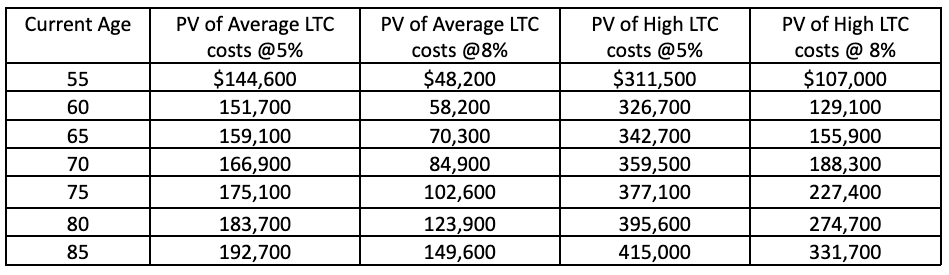

The table below shows different reserve values for females of different ages and for different levels of LTC coverages based on the following assumptions. Again, current costs are derived from the Genworth Cost of Care Survey 2025 Median Cost Data Tables for California.

Assumptions for the table:

- Medium Cost: Two years of assisted living and one year of nursing home care (semiprivate room) during the three years prior to assumed retiree demise.

- High Costs: Two years of assisted living and three years of nursing home care (semiprivate room)

- Net average annual cost for the three years prior to assumed death equal to $70,000 per annum in today’s dollars. Net cost represents average LTC cost for the three or five years in today’s dollars less assumed reduction in annual household recurring expenses (about $35,000 annually) for the period during LTC.

- Assets set aside to fund LTC expenses earn either 5% per annum and are relatively safely invested, or earn 8% per annum and are invested in riskier assets, consistent with the default investment return assumptions in the AFP.

- LTC expenses are assumed to increase by 4% per annum, 1% greater than the assumed default rate of annual inflation in the AFP.

- No LTC insurance.

The PVs below represent how much a retired female should theoretically currently have set aside as a separate dedicated asset “reserve” today to fund her future LTC expenses based on her current age and the above assumptions.

Table 1: PVs of Average and High Future LTC Costs by Age

As shown in the above table, five years of LTC is expected to cost more than three years of LTC. If assets set aside to fund LTC costs are more aggressively invested and earn an annual 8% rate of return, the amount of assets currently needed to fund the LTC will be less than if they earn 5% per annum. It should be remembered, however, that more aggressive investing involves greater risk.

It should also be remembered that assumptions and pricing of long-term care can and will change from year to year, and the above PVs are expected to increase from year to year and should be periodically reestimated to see if assets set aside for this purpose continue to be sufficient. I recommend that this calculation be revisited annually as part of an annual client meeting to remeasure the client’s funded status and discuss other issues of importance to the client.

Additional Thoughts on Assets

If your client does not have LTC insurance, or their insurance is not expected to be adequate to fully cover their LTC needs, the client should generally be encouraged to set aside funds to pay for future LTC. Ignoring the issue will generally not make it go away, and will increase the amounts necessary to fund LTC later on.

Assets used to fund LTC can come from many sources — home equity, savings, bequest motives, etc. It is important, however, to make sure that sufficient assets are earmarked for this purpose and are not used for some other purpose. It is also important to consider tax implications of possible sales of assets in the future to pay for LTC.

Some clients may wish to start with a relatively low estimate of LTC costs in the early years of retirement and plan on building up their reserve in the later years of retirement during the “slow go” or “no go” years. Other clients with limited sources of assets to fully fund LTC may plan on using the Medicaid LTC program in their state as a backstop. Still others may wish to look into LTC insurance rather than self-fund. It will be important for their financial advisor to guide them on these decisions.

Summary

Not everyone will need LTC. For planning purposes, it is generally prudent to assume that such care will be needed and should be anticipated to some degree in the household’s spending liabilities. If you use the 4% Rule, or some other simple withdrawal approach for your clients, or you are ignoring long-term care costs when determining the probability of your client being able to spend $X per year, you might want to look into determining a separate reserve for your client’s uninsured long-term care costs, or simply switch to a better approach, like the Actuarial Approach, that considers all your client’s liabilities and assets in retirement.

Ken Steiner is a retired actuary with a website titled, "How Much Can I Afford to Spend in Retirement?"

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All