The Tangible Side of a Digital World: Don’t Overlook the Inputs

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

In an age when investors obsess over quarterly earnings, AI hype, and the Federal Reserve, it’s easy to overlook what actually makes the global economy tick: the inputs that power, build, and sustain growth.

Capital. Labor. Energy. Raw materials. These are the bedrock ingredients that determine whether companies can make things, move things, and scale profits. And if you want to be a better investor — especially in a world of rising volatility and structural shifts — it’s time to pay closer attention.

1. Global Capital

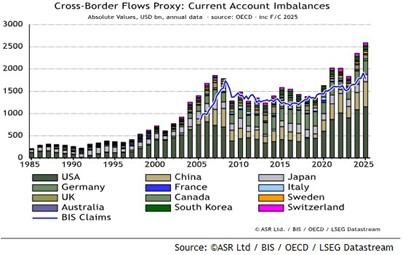

For decades, global capital has flowed like water — fluid, abundant, and largely apolitical. But that era may be quickly coming to an end.

The evolving trend of weaponized trade, including tariffs, industrial policy, and punitive sanctions, is now bleeding into the financial sphere. The result is a rising risk of weaponized capital, where capital flows are no longer purely economic decisions, but strategic ones.

The U.S. has become vulnerable to capital reallocation, repatriation, and contraction of cross-border flows, particularly in response to isolationist tariff and diplomatic policies. According to Absolute Strategy Research, non-U.S. entities owned $14 trillion and $17 trillion of U.S. debt and equity, respectively. Should a global sell-off occur, it could result in financial disaster for the U.S. government and private finances.

The shift toward “self-sufficient production” in trade is accelerating a parallel move toward self-sufficient capital, with countries and regions looking to insulate themselves from foreign financial leverage. Europe, perceiving that the U.S. may no longer be a reliable partner, faces pressure to deepen domestic capital markets or risk losing ground in defense, infrastructure, and tech investment.

In response to these risks, central banks around the world are increasing their gold reserves as a strategic hedge against geopolitical instability, currency volatility, and the weaponization of the U.S. dollar. Gold offers a politically neutral store of value that isn't subject to sanctions, default risk, or foreign policy pressure, making it an attractive form of sovereign liquidity in an increasingly fragmented financial system.

The implications for investors are profound. A reduction in global “portable capital” could mean tighter liquidity, higher volatility, and rising funding costs. If cross-border capital becomes less available, portfolio construction must adapt to a more partitioned financial ecosystem.

2. Labor

The post-pandemic labor market is increasingly defined by structural constraints, not cyclical ones. According to Oxford Economics, multiple forces are weighing on labor supply growth: stricter immigration enforcement, federal job cuts, and weakening wage increases.

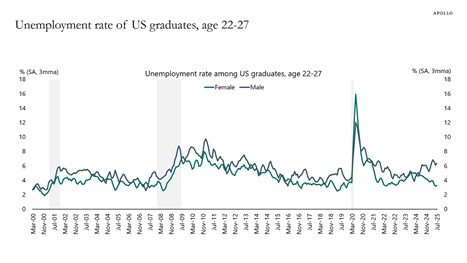

In recent months, consumers’ perceptions of the labor market, especially among those aged 22 to 27, have dropped off a cliff. Per the chart below from Apollo Global Management, the unemployment rate for these workers is hovering between 8% and 10%.

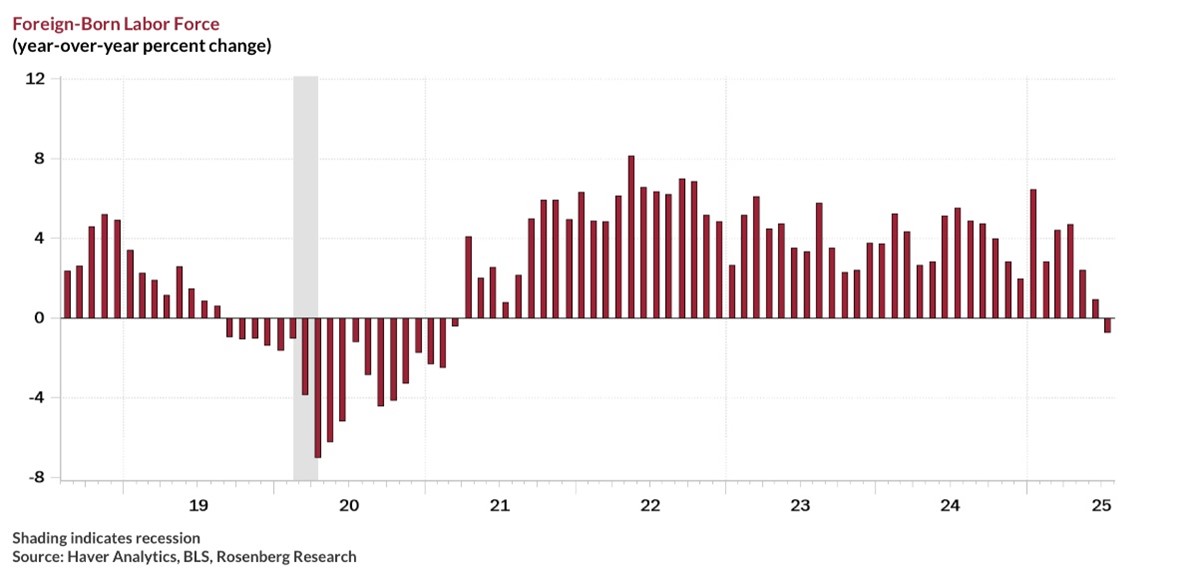

Meanwhile, foreign-born labor supply is also under strain. According to a separate Oxford analysis, stepped-up immigration enforcement has caused a sharp drop in recent immigration to the U.S. While current wage data suggests no immediate inflationary pressure from this slowdown, it’s putting a ceiling on labor supply growth in sectors that rely heavily on immigrant workers: construction, agriculture, and hospitality.

The net result? A labor market that is showing cracks beneath the surface. Participation is under pressure and long-term labor force growth — a key driver of potential GDP — is at risk of stalling within developed economies.

3. Energy

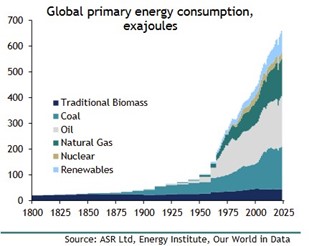

Let’s start with the most immediate challenge: AI’s insatiable hunger for electricity. The buildout of data centers, increasingly designed around compute-heavy workloads, is projected to quadruple global electricity demand by 2035. U.S. AI data center consumption alone is expected to exceed 50 gigawatts by 2028 — nearly double New York City’s current peak demand.

That surge is colliding head-on with aging infrastructure and inadequate grid capacity. Despite a decade of hype around “clean energy transitions,” most of what’s actually occurred is electrification without substitution. For example, fossil fuels still made up over half of the world’s incremental energy demand in 2024. According to Absolute Strategy Research, we’re not seeing a transition so much as an addition — clean energy is being layered on top of fossil consumption, not replacing it.

Meanwhile, our national electrical infrastructure is dangerously susceptible. Transmission constraints, interconnection delays, and underinvestment in storage threaten to bottleneck everything from AI to EVs to basic industrial activity. Grid modernization and storage are now economic imperatives.

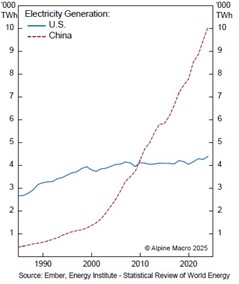

In the geopolitical arena, energy is becoming a key lever of national competitiveness. China is rapidly scaling its generation and grid capacity, with over 90% smart meter penetration, 62 GW of battery storage, and the majority of global renewable projects within its borders. The U.S., quite simply, has fallen behind.

For investors, this shift reframes energy entirely: not as a cyclical commodity play, but as a strategic input whose availability will increasingly determine which companies, sectors, and nations can scale.

4. Raw Materials

Water

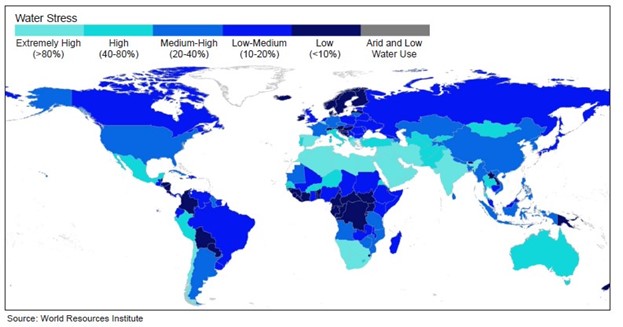

Global water systems are under unprecedented stress. According to Alpine Macro, deferred investment in water infrastructure has resulted in ~$470 billion in economic losses annually. By 2050, water stress could shave 8% off global GDP and up to 15% in low-income countries.

Meanwhile, the U.S. experiences a water main break every two minutes, losing 2.1 trillion gallons annually. India, home to 18% of the world’s population, has just 4% of its freshwater and is “exporting” much of it as virtual water through crops like rice. And don’t look to Europe for best practices — two-thirds of its water infrastructure is in “bad condition.”

AI and data centers are rapidly adding to the problem. One hyperscale facility can consume over 5 million gallons of water per day. We’re entering an era where tech innovation is directly constrained by water availability, and few investors are modeling that risk.

Metals

Parallel to water scarcity is the escalating importance of critical materials, especially metals like copper, lithium, cobalt, and rare earths. These are the lifeblood of electrification, AI hardware, EVs, and energy storage — and the mismatch between demand and supply is intensifying.

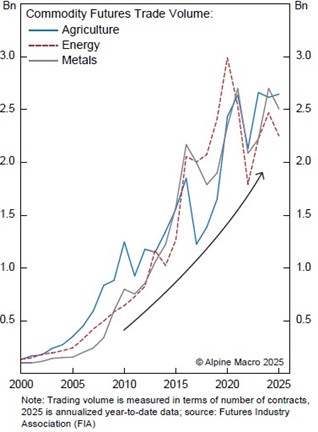

Industrial metals now display tighter correlation with economic cycles than at any time since the GFC. China consumes 60% of global industrial metals, but new supply is increasingly constrained by environmental, political, and logistical bottlenecks.

The global push toward electrification, digital infrastructure, and energy transition is accelerating demand for a wide range of industrial metals. Silver is becoming increasingly vital thanks to its unmatched electrical conductivity, making it essential for solar panels, EVs, and semiconductor components. Meanwhile, copper remains the irreplaceable backbone of power grids, data centers, and industrial machinery. Aluminum, nickel, cobalt, and rare earth elements are also surging in demand across battery technology, wind turbines, and consumer electronics. But while demand is rising exponentially, supply remains bottlenecked by geopolitical risks, environmental regulation, and long development timelines.

Conclusion: Invest Where Inputs Matter

Modern economies are built on ideas, innovation, and intangible assets, but they still run on inputs you can’t digitize away. Labor, energy, materials, water, and capital are the physical and financial infrastructure that supports growth, drives margins, and defines which business models can actually scale.

The future will reward companies and investors that secure inputs, manage scarcity, and invest in physical resilience. Whether it's the miner with copper access, the utility with grid capacity, or the firm rethinking labor strategy, the edge won't come from ideas alone — it will come from those who can build, power, and fund the next phase of real growth.

David Tepp is the founder and managing principal of Tepp Wealth Management, an SEC-registered investment adviser based in Westfield, New Jersey. With over 20 years of experience in wealth management, David provides strategic financial planning and investment advisory services to high-net-worth individuals and families. He frequently writes on macroeconomic policy, fiscal risk, and market strategy to help investors navigate an increasingly complex global economy.

Sources:

Absolute Strategy Return, “From Weaponised Trade to Weaponised Capital:, written by Ian Harnett, April 3, 2025

Absolute Strategy Return, “Controversies, Convictions & Context #4”, written by Ian Harnett and David Bowers, May 8, 2025

Absolute Strategy Return, “Water, Food & Climate: The New Security Imperative”, written by Michael Penn, May 30, 2025

Absolute Strategy Return, “The Critical Metal Catalysts”, written by Michael Hessel, July 4, 2025

Absolute Strategy Return, “Energy Transition: Myths & Realities”, written by Michael Penn, July 22, 2025

Absolute Strategy Return, “Real Asset Revival”, written by Zahra Ward-Murphy, August 8, 2025

Alpine Macro, “Future Water Security Hinges on Innovation”, written by Noah Ramos, November 20, 2024

Alpine Macro, “Adapting Commodity Strategy to Shifting Correlation Dynamics, written by Kelly Xu, August 5, 2025

Alpine Macro, “AI, Energy, And the Grid – A Collision Course”, written by Noah Ramos, August 6, 2025

Rosenberg Research, “Making Uncertainty Great Again: Take Three”, written by David Rosenberg, September 2025

Oxford Economics, “ICE Arrests Proving a Hinderance to Labor Force Growth”, written by Matthew Martin, August 4, 2025

Oxford Economics, “The Young and the Anxious”, written by Ryan Sweet, March 26, 2025

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

DISCLOSURES:

Investment advisory services are offered through Tepp RIA, LLC dba (Tepp Wealth Management), an SEC registered investment adviser. Information pertaining to the registration status of Tepp Wealth Management, a copy of Tepp Wealth Management’s current written disclosure statement discussing Tepp Wealth Management’s business operations, services, and fees is available at the SEC’s investment adviser public information website – www.adviserinfo.sec.gov (CRD# 283899) or from the Adviser upon written request: Tepp Wealth Management, 210 Elmer Street, Westfield, NJ 07090.

The views and opinions expressed represent the author’s judgment as of the date of publication and are subject to change without notice. This is for informational purposes only and is intended to inform the reader about market-related activities which could affect individual portfolios and provide insight on specific relevant topics. It is not intended to recommend or suggest any specific course of action or investment strategy. The reader should not infer the likelihood of any future events. Past performance is not indicative of future results. Investors should always consult an investment professional and/or tax professionals to discuss their unique needs and objectives. Tepp Wealth Management undertakes no obligation to update or revise any forward-looking statements to reflect new information, subsequent events, or changes in circumstances.

The information presented reflects general market commentary and is not intended to provide, and should not be construed as, investment, legal, accounting, or tax advice, or as a recommendation to buy or sell any specific securities or to adopt any particular investment strategies. Please remember that different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment or investment strategy (including those undertaken or recommended by the Adviser), will be profitable or equal any historical performance level(s).

Tepp Wealth Management may discuss and display, charts, graphs, formulas which are not intended to be used by themselves to determine which securities to buy or sell, or when to buy or sell them. Such charts and graphs offer limited information and should not be used on their own to make investment decisions. This information is provided for guidance and information purposes only and is not a solicitation. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All