When I can’t listen to a podcast without someone trying to sell me gold, when money managers tell me clients are jonesing for the shiny metal, and when friends call to ask what I think about buying it, I know without looking at a single chart that the price of gold has gone vertical and that FOMO has set in.

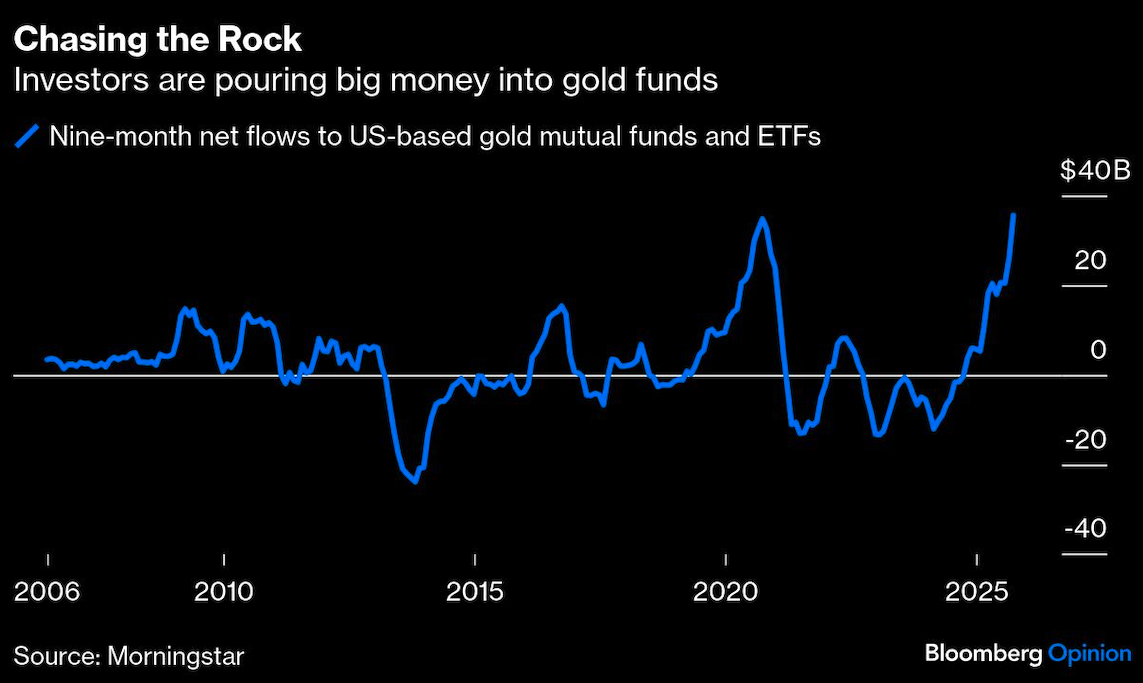

And wouldn’t you know, the price of gold has skyrocketed this year, in one of the biggest rallies since its price began to float freely in 1968. Predictably, Google searches for “how to buy gold” are at a record high. Net flows to US-based gold mutual funds and exchange-traded funds have topped $35 billion this year through September, according to Morningstar Inc., the largest nine-month haul since at least 2005.

Which begs the question: Should investors own gold? I have no doubt that Wall Street, which never misses an opportunity to peddle a hot asset, suddenly thinks so. Morgan Stanley’s Mike Wilson has suggested that investors in a traditional 60/40 stock/bond portfolio move half the bond allocation to gold, rejiggering their portfolio into 60/20/20 stock/bond/gold.

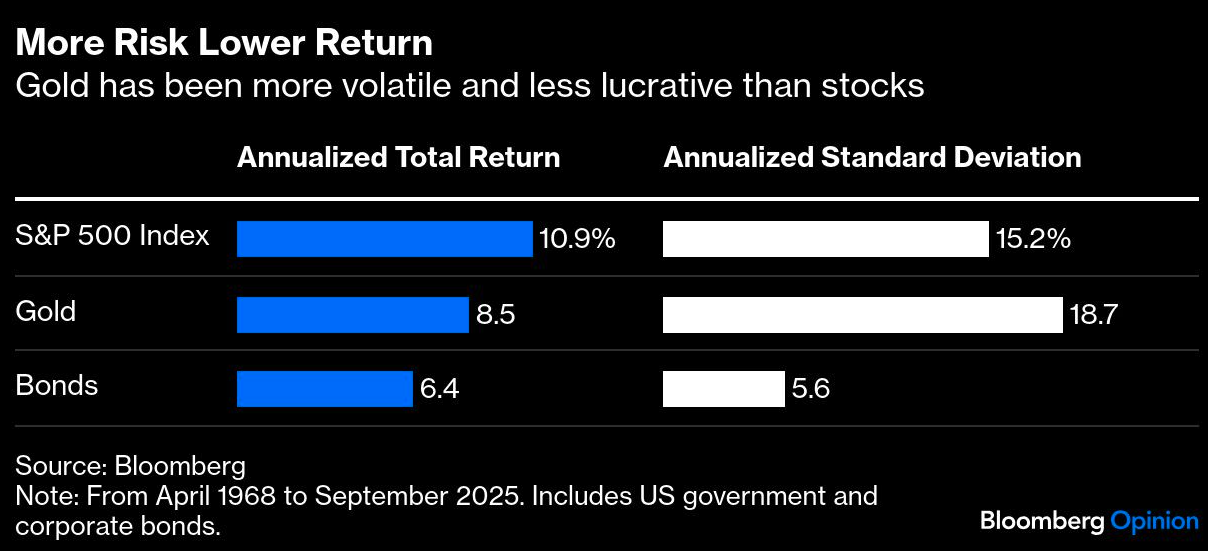

At first glance, this looks like an upgrade. The gold-infused portfolio would have beaten a 60/40 comprised of the S&P 500 Index and a basket of US government and corporate bonds by 0.7 percentage points a year from April 1968 through September, including dividends.

But there are devils in the details. For one, gold and bonds are not interchangeable. Gold was more than three times as volatile as bonds over the past six decades, as measured by annualized standard deviation. Gold paid investors 8.5% a year over that time, 2.1 percentage points better than bonds for its additional volatility. Investors who swap bonds for gold can expect higher returns but should also brace for a bumpier ride.

Gold resembles stocks more than bonds in terms of risk, although stocks have been better performers. Since 1968, gold has been about 20% more volatile than the S&P 500 while trailing it by 2.3 percentage points a year. Investors looking to boost their 60/40 portfolio with gold can do just as well — and possibly better — by allocating more to stocks instead.

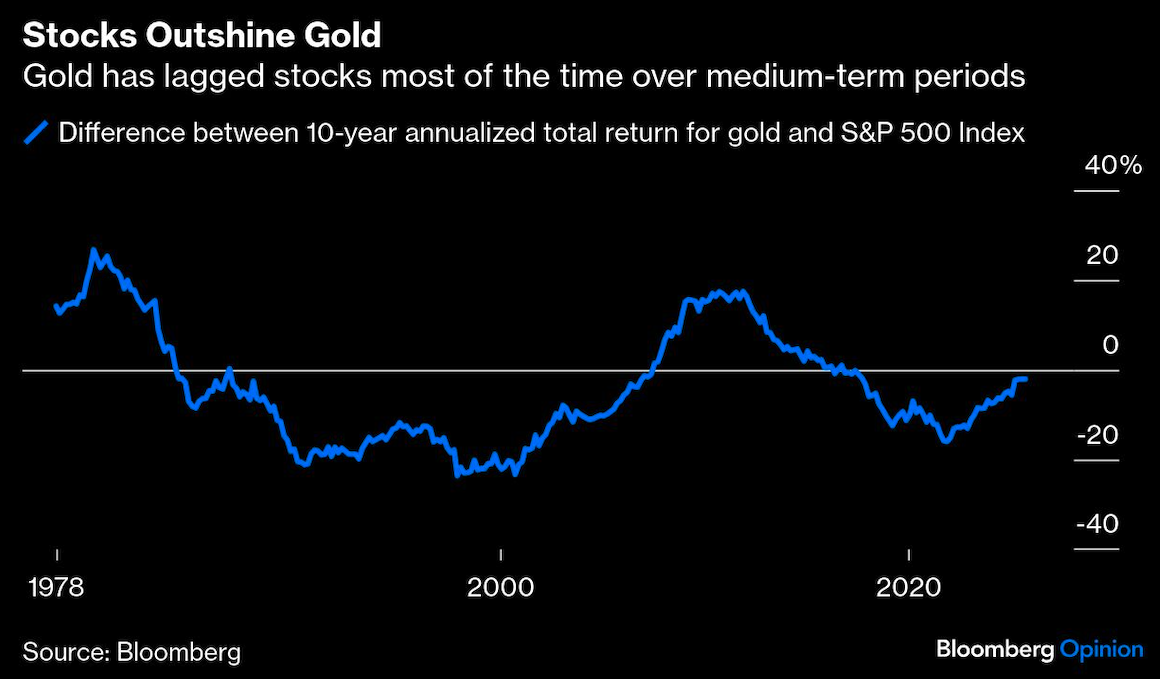

Stocks have another advantage over gold: They are more reliable performers. Most investors don’t have six decades to invest, so what happens in shorter periods is often more consequential. This is where gold loses its luster.

Over rolling 10-year periods, stocks and bonds have beaten gold most of the time. That’s because, unlike stocks or bonds, gold has experienced long lulls — the price of gold was the same in 2007 as it was nearly three decades earlier in 1980 — interrupted occasionally by quick bursts, like the one now underway. In that regard, gold has more in common with its digital alternative Bitcoin than traditional assets.

Of course, not everyone buys gold based on cold calculation. Many gold bugs are famously motivated by fear. Leaving aside the strange fact that a metal more volatile than stocks is widely viewed as a safe haven, it’s worth examining how previous fear-inspired gold trades have turned out.

In the past two decades, flows to gold funds spiked around the 2008 financial crisis, President Donald Trump’s first inauguration in 2016 and the 2020 Covid pandemic. Each time, the gold rally fizzled when fears subsided, and stocks ultimately kept pace or outperformed, even after accounting for gold’s recent surge.

This time, many gold investors seem to fear a tariff-induced collapse of the dollar and higher inflation. Bond markets don’t share those inflation concerns, at least for now. Treasury yields have declined this year, and inflation expectations remain anchored around the Federal Reserve’s 2% target.

And even if the dollar is set to decline, it’s not obvious that gold will offset those losses. There’s been a relatively weak inverse correlation between gold and the US dollar since 1968 (-0.29 counted monthly). There were only three big dollar declines in that time, and gold’s record is mixed. It surged when the dollar declined during the 1970s and in the years leading up to the financial crisis, but it was mostly flat from 1985 to 1992.

A surer way to hedge against a declining dollar is to own a broad basket of non-US currencies. This is where stocks come in handy yet again. A globally diversified portfolio of companies allows investors to simultaneously profit from growing businesses while gaining exposure to every currency in the developed world and those of many developing countries.

I suspect the fears now driving gold will pass and that this rally will fade with them. But go ahead and buy gold if you want. Just don’t expect a windfall. The time for that was before this rally started.

A message from Advisor Perspectives and VettaFi: Stay ahead of market changes with our daily updates on key market and economic indicators. Visit the AP Charts and Analysis site for our expert insights.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Nir Kaissar