Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Offerings for private investments have changed dramatically in recent years. Access to private markets is typically provided through a drawdown vehicle, where limited partners (investors) commit a certain amount of capital to a private fund and the general partners (portfolio managers) call or invest the capital over time, as opportunities arise.

The investment period is usually three to five years, though a drawdown strategy, and the full life span of the fund is normally 10 to 12 years. At the the end of that period, the general partners start selling private investments in their portfolio and distributing the proceeds back to investors.

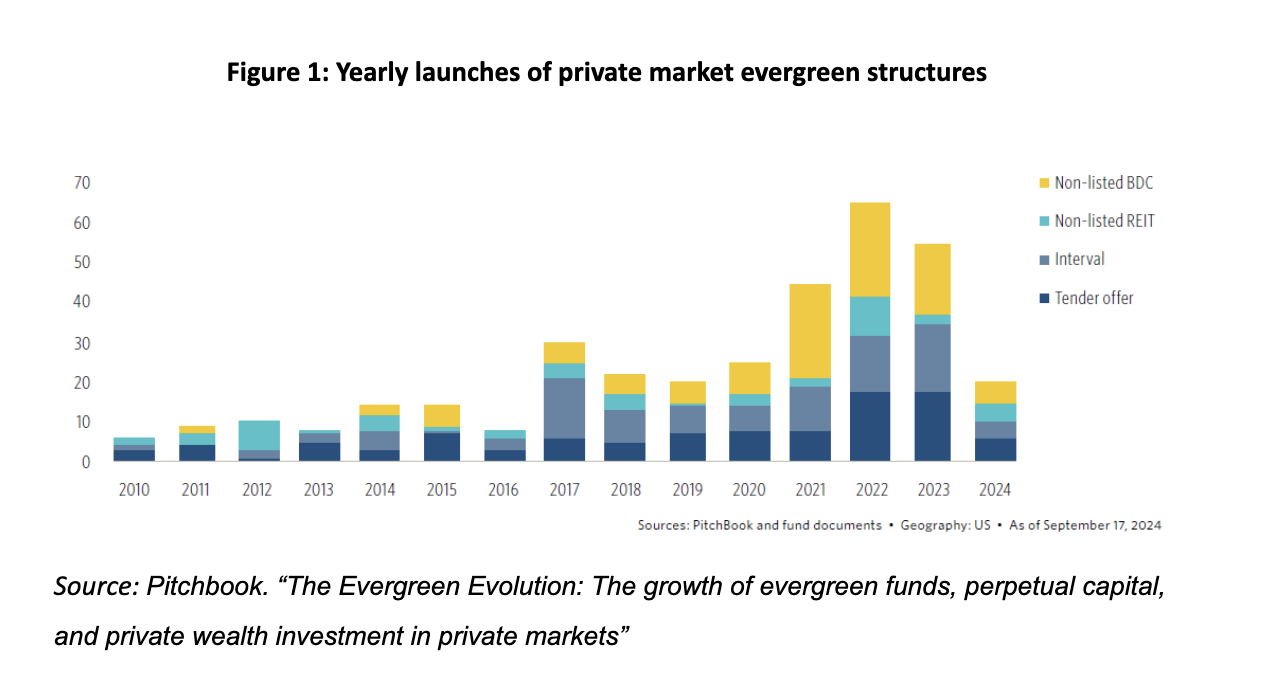

More recently, the growth of private market evergreen funds — which raise capital, invest, and distribute returns without needing to wind down or liquidate after a fixed term — has provided a new avenue to get immediately allocated to private markets. Since 2019, there have been more than 200 evergreen funds launched. Those products now manage close to $400 billion in assets.1

These evergreen products help general partners avoid common issues with irregular fund launches and end-of-life liquidations. For limited partners, these funds provide an easier way to make private investments such that investors can get more substantially allocated and potentially benefit from strong long-term compounding returns.

There are issues that must be considered when deciding to invest in an evergreen strategy. It is important to monitor the potential advantages and disadvantages of evergreen vehicles, especially if they are part of your greater asset allocation.

Evergreen Fund Advantages

There are several advantage to an evergreen fund wrapper:

Immediate allocation to private markets: Through an evergreen fund, an investor can purchase shares in a product at its current net asset value (NAV). These funds usually provide exposure to a diversified pool of private assets, which not only minimizes risks but also offers the potential to generate robust returns relative to public markets.

Flexibility: Most evergreen funds offer periodic redemption windows (e.g., quarterly or semiannually). These intervals allow investors to redeem a portion or all of their investment without waiting for distributions, which, in some cases, can take 10 or more years to occur. Also, it eliminates the need to raise cash from other parts of a portfolio to meet capital calls.

Reduced J-curve effect: The J-curve — a concept showing how returns to private investors are often negative in the early years due to fees and initial costs — may be smoother with evergreen funds, since many hold mature positions and recycle distributions.

Ongoing reinvestment: Like a mutual fund, the proceeds from exits or income-generating private assets (e.g., private debt) can be reinvested automatically. This can assist in compounding returns without having to recommit to a new drawdown fund.