The US Federal Reserve will soon face a crucial decision: What to do with the vast portfolio of securities it has amassed in its efforts to manage the economy?

The best and safest approach would be to stop the shrinkage known as quantitative tightening very soon. That’s what I expect it to do.

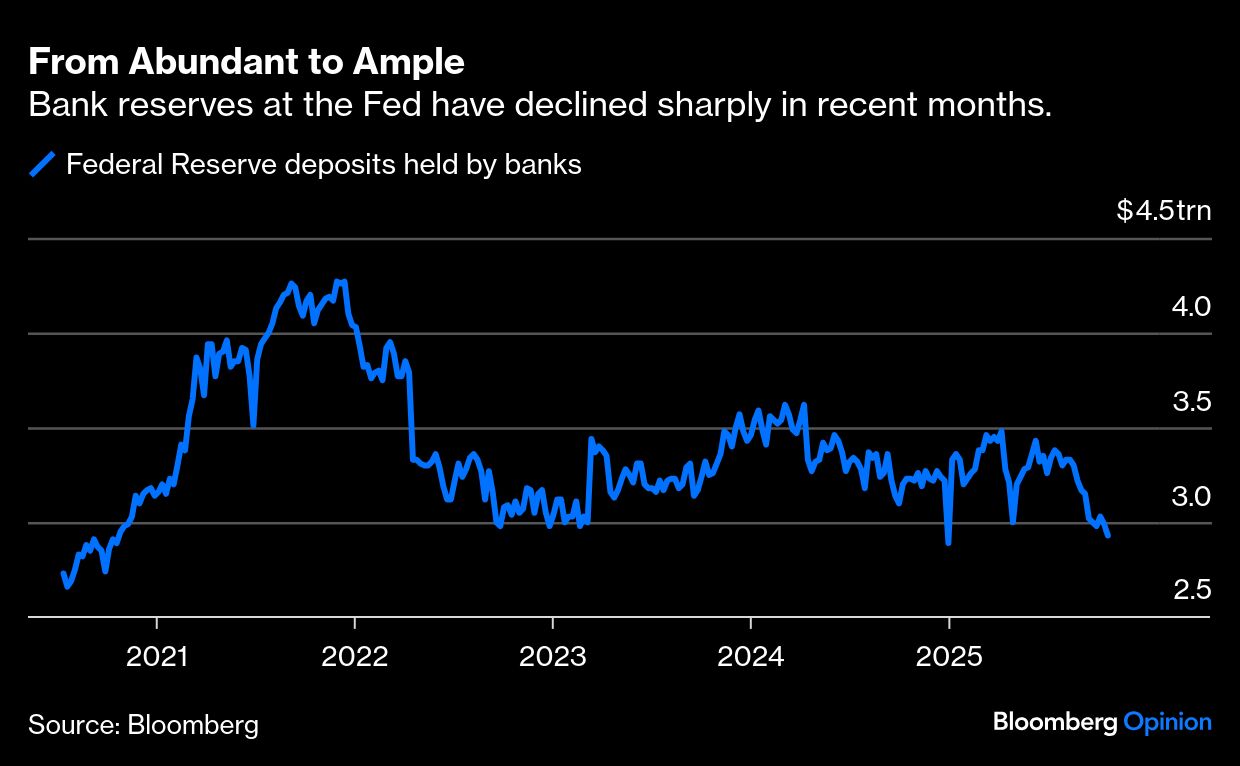

After the 2008 financial crisis, and again during the global Covid pandemic, the Fed purchased large amounts of Treasury and agency mortgage-backed securities — a policy known as quantitative easing. This was to provide additional monetary stimulus at a time when short-term interest rates were already near zero. By March 2022, this pushed banks’ reserves at the Fed up to more than $4 trillion. As economic growth rebounded and inflation soared, the central bank reversed course, raising short-term interest rates and shrinking its securities portfolio.

Since then, the Fed has been seeking to move from an “abundant” to an “ample” reserves regime. In the latter, banks have enough cash to meet the market’s needs most of the time, and the Fed stands ready (via its standing repo facility) to lend more cash against high-quality securities in certain circumstances — say, when Treasury debt auctions or corporate tax payments cause reserves to temporarily decline below what banks demand.

The Fed is now close to striking this delicate balance. Bank reserves have fallen sharply, to less than $3 trillion, as the Treasury has rebuilt its cash balance at the Fed in the wake of the summer debt-ceiling standoff. The decline in reserves has pushed the effective federal funds rate up by a few basis points, to 4.11% from 4.08% a month earlier. Banks have occasionally turned to the Fed’s standing repo facility when securities financing rates have briefly climbed above 4.25% rate on offer at the facility.

So should the Fed stop here, with a securities portfolio of more than $6 trillion? Some think not. Fed Vice-Chair Michelle Bowman, for example, argues that the central bank should minimize its “footprint in the money markets and Treasury markets” as much as possible. In this “scarce” reserves regime, she says, the market would provide more timely signals of stress or functioning issues, banks would more actively manage their cash balances, and the Fed would have more leeway to mitigate future shocks “without worrying whether there is enough room to expand the balance sheet.”

I disagree. Why risk a repeat of the money-market turmoil of September 2019 when this is entirely unnecessary? Pushing the market to the brink of stress, or requiring banks to rely on less secure sources of funding, would be more alarming than reassuring, and would increase the cost of borrowing. The Fed has unlimited capacity to expand its balance sheet, either by purchasing high-quality securities or by lending against them. In doing so, it provides banks with an asset – reserves - that has no liquidity, settlement or interest-rate risk. This makes the system more stable and monetary policy operationally simpler than in a scarce-reserves regime.

Others worry that even the transition to an ample reserves regime could destabilize financial markets, at a time when the travails of subprime auto lender Tricolor Holdings and auto-parts supplier First Brands Group are already signaling trouble. I doubt it’ll prove important. When reserves were abundant, the excess liquidity mostly just sat at the Fed. Banks held more reserves than desired and the central bank invested them in Treasury and agency mortgage-backed securities, with this demand resulting in slightly lower longer-term yields and mortgage rates. The interest rate on reserves, set by the Fed, determined money-market rates and the amount of private-sector credit activity.

I expect the Fed to end quantitative tightening very soon, perhaps as soon as this month. The $5 billion of Treasury securities that the Fed was allowing to run off each month, as well as prepayments of mortgage-backed securities — slightly more than $15 billion a month — will now be reinvested into newly issued Treasuries. Most likely, the reinvestment will focus on shorter-term Treasury bills, which currently account for only $195 billion of the Fed’s $4.2 trillion Treasury portfolio. Over the longer term, the Fed will have to increase its Treasury holdings, so that the supply of reserves keeps pace with economic growth.

Even though the transition from QT will likely go smoothly, the Fed still has some explaining to do. For one: Have the benefits of its balance-sheet policies outweighed the costs? The pandemic-era quantitative easing program will likely cost between $500 billion and $1 trillion in foregone interest income. The Fed’s losses, shown as “earning remittances due to the US Treasury,” exceed $240 billion and are still accumulating. As part of its monetary policy framework review, the Fed should develop an explicit cost-benefit analysis to guide the future use of quantitative easing and tightening — and clearly differentiate between asset purchases designed to provide monetary stimulus versus those aimed at supporting market functioning during times of stress.

Beyond that, the Fed should lay out in greater detail how its balance sheet is likely to evolve under its “ample” reserves regime. What, for example, is the desired composition of the Fed’s securities holdings in terms of type and duration? How will it get there? Will it sell off mortgage-backed securities to speed up the transition to the desired all-Treasury portfolio?

Even when quantitative tightening ends, the Fed’s work will be far from done.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Bill Dudley