The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.

These days, it’s all stocks all the time, with reputable authorities calling on small investors to put everything they have saved into equities — a broad, low-cost index fund, of course — holding aside only a speck of emergency cash. Your grizzled authors are reminded of the mantra so common in 1999: “Every penny you don’t have invested in stocks will hurt you.”

More than a generation ago, financial historian Peter Bernstein (sadly, no relation to Bill) wrote about investors’ “memory banks,” the market experience that accumulates in their hippocampi over their investing lives and molds their investment strategy. As he put it, looking back on the 1990s: “Most of the new participants in the market had no memory of what a bear market was like.”

And here we are today, almost seventeen years into a great bull market. Rather like 1999, also seventeen years into a long-term bull market, or 1966, once more seventeen years. Or 1873, sixteen years in, or 1837, eighteen years in, or 1893, twenty years in — to name a few of the notable tops over the past two centuries. Just long enough to produce empty memory banks in just enough investors.

Savvy Investing or Youthful Indiscretion?

Nowhere is today’s zeitgeist better captured than in a recent Economist piece entitled “Investing like the ultra-rich is easier than ever,” which describes a highly leveraged strategy espoused by Barry Nalebuff and Ian Ayres in their 2010 book “Lifecycle Investing.” The star of the Economist piece is a pseudonymous “Mr. Street,” who has embraced the Nalebuff/Ayres strategy. While 200% equity was difficult to manage when they wrote the book in 2010, Mr. Street can now execute it with cheap margin loans from the likes of Interactive Brokers.

Trouble is, while the Economist piece focused on how inexpensive margin loans made leveraged investing so much easier, it buried the lede: Mr. Street, it turns out, is in his early 30s.

Need we say the quiet part out loud? Mr. Street, poor baby, has never personally experienced a long-term bear market as an established investor, and his memory banks are devoid of the damage wrought by the Grim Reaper of equity risk. Let’s be generous and assume he’s read his market history and knows that stocks can lose money — sometimes, a lot — and take months, if not years, to recover. There’s a difference, though, between being told that markets can fall by more than 50% and having it burned into your memory banks by seeing your net worth halved in real time as the economy careens towards the precipice.

Aviation provides no end of fruitful metaphors for investing: To pilot an aircraft is to learn over and over the importance of building in a margin of safety and then building more safety on top. Moreover, while flight simulators are useful training tools, especially for complex aircraft, they are in no way a replacement for real-world experience. It’s one thing to plug an aircraft fire into the sim, and it’s quite another to actually wrestle with the controls as real flames lick the cockpit.

In the same way, running a back test in your spreadsheet or a Monte Carlo simulation and being comforted that 90% of the time your portfolio didn’t crash isn’t the same as actually investing through the March 2020 COVID panic or the longer 2007–2009 financial crisis.

Short Memories Meet Unwarranted Confidence

We all like to believe we’re Star Trek’s hyper-rational Mr. Spock, but as Captain Kirk might have phrased it, there are no sentient beings in this quadrant of the galaxy who can tolerate, over their two or three decades of youthful human capital dominance, 200% equity exposure.

Let’s put it a different way: That much risk only seems tolerable after, say, seventeen years of a great bull market — when enough investors have forgotten about bear markets. The memory banks of the young Mr. Street contain nothing but eau de Magnificent Seven. No wonder he’s such a brave lad!

Back to Peter Bernstein (who passed in June 2009, at the end of the Great Recession): Once enough investors’ memory banks are devoid of real-life bear market agita, caution gets thrown to the wind. As a result, the notion of holding all stocks, even in retirement — heck, why not 200% stocks when young? — starts to seem perfectly logical. Come to think of it, why not put 50% down on one of those 3X leveraged ETFs like SPXL or UPRO to lever up to 600% equities?

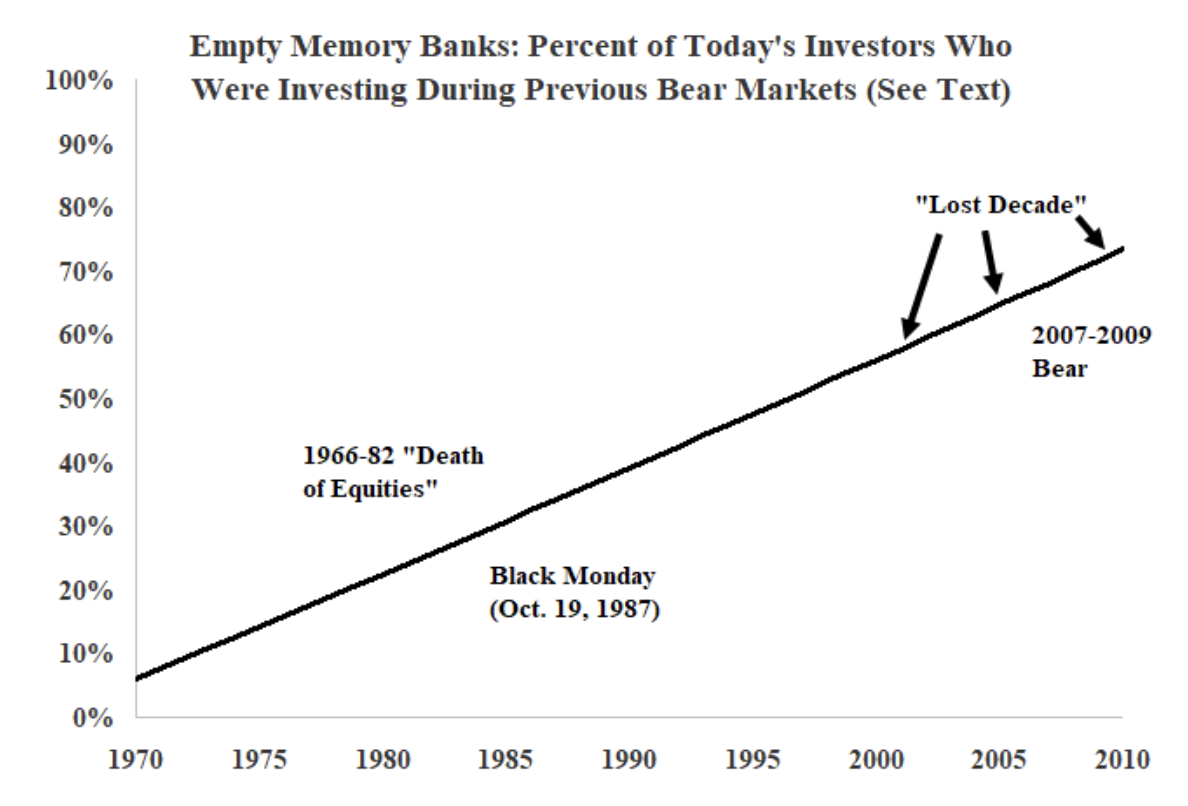

Let’s stipulate that you have to be 30 or older to be a member of the investor population. Likewise, only bear markets experienced while 30 or older are likely to get engraved on investor memory. Given those definitions, for any market event, at any distance in the past, we can use census age distribution data to estimate what percentage of today’s investors — everyone over 30 — has a lived experience of that event.

Take Peter Bernstein’s example of 1999, 17 years after the end of the last awful bear market in 1982. If you were just old enough to experience that bear at age 30, then you were born in 1952, which made you 47 in 1999, at which point roughly a third of those over 30 had bear-market-less memory banks. Call it the Peter Bernstein Rule: When more than 30% of investors have no memory of the last bear market, look out!

So were Peter with us today, he’d surely want to know how many of today’s investors have any lived experience of investing through 2007–2009, when Mr. Street was likely not out of his teens. He might have had a play account at that age, but he wouldn’t have any real money at risk. Only individuals born before 1978, who are now in their mid-40s or older, have 2008 in their memory banks.

Experiences Waiting to Happen

Mr. Street didn’t live that decline: Those fraught years, when the survival of the entire economy was in some doubt, are not in his memory banks. Today, after some years of employment, possibly as a professional, with years of contributions, he does have enough money at risk. When — not if — stocks plunge, whether it’s next month or in the next decade, his memory banks will look a lot different, especially after Interactive Brokers margins him out at 100% leverage.

In short, seventeen years down the road, only investors age 47 or older have that burning memory of 2008. That’s but 70% of the investor population as defined above — about at Peter Bernstein’s danger point.

For the dotcom bust, you had to be born in 1970 or earlier to have a lived experience of the decline that began in 2000. That’s just 56% of today’s investor population — well beyond Peter Bernstein’s danger point.

Remember, in some respects the 17-month bear market of 2007–2009, by itself, was just turbulence. More importantly, it capped a 10-year bear market that began in 2000 and saw investors burned by a negative real equity return over the decade between early 1999 and early 2009, also known as the “lost decade.”

Still not impressed? How about the 17-year period between 1966 and 1982, which saw a real stock return of zero — assuming that you could invest in the fully diversified S&P 500 index fund with three basis points of expenses, which of course you couldn’t. Only about 39% of the investing population has that excruciating drought etched in their memory.

Below, we’ve plotted the percent of today’s investors who experienced the above bear markets at age 30 or above. (Kudos to Mark Higgins, author of Investing in US Financial History, for the concept behind this graph.)

Calculations by authors based on data from census.gov

So here we are in late 2025, with rampant speculation in crypto, private equity, leveraged single-stock ETFs and leveraged private lending, to say nothing of stratospheric capex on AI infrastructure that depreciates faster than ice cream on an August afternoon. At the same time, the bear-market memory bank gauges of an ever-increasing percent of the population are now bouncing off empty: What could go wrong?

William J. Bernstein is a neurologist, the co-founder of Efficient Frontier Advisors, an investment management firm, and a writer with several titles on finance and economic history. He has contributed to the peer-reviewed finance literature and has written for several national publications, including Money Magazine and The Wall Street Journal. He has produced several finance titles, and four volumes of history, The Birth of Plenty, A Splendid Exchange, Masters of the Word, and The Delusions of Crowds about, respectively, the economic growth inflection of the early 19th century, the history of world trade, the effects of access to technology on human relations and politics, and financial and religious mass manias. He was also the 2017 winner of the James R. Vertin Award from the CFA Institute.

Edward F. McQuarrie, Ph.D., is professor emeritus at Santa Clara University. He writes about financial history and its implications for retirement planning. Working papers describing his research can be downloaded here.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by William Bernstein, Edward McQuarrie

The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.