A small circle of investment consultants played a central role in the multi-trillion-dollar push into private markets, steering US pension funds toward private equity, real estate and hedge funds, according to a new study.

The shift over the past two decades was driven less by changes in pension fundamentals than by the recommendations of these advisers, researchers at Harvard University and Stanford University found. Portfolios moved because consultants encouraged pensions to chase higher returns in alternatives.

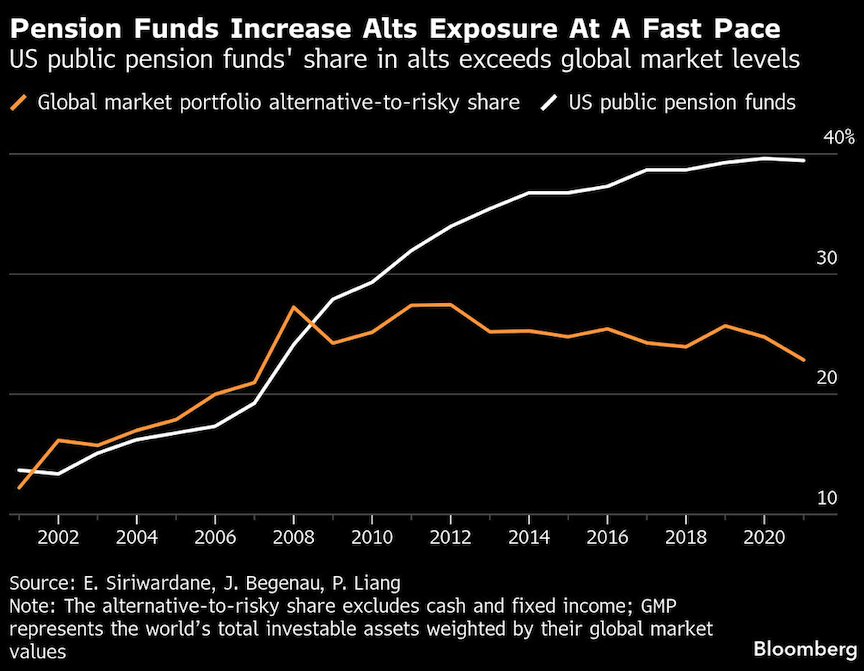

From 10% of total investments at the start of the century, the share held in alternatives has tripled in the years since, underpinning a golden era for professional money managers who operate outside public exchanges.

In short, the impact has been sweeping — rarely have so few influenced the retirement destinies of so many, the argument goes. And while no one is suggesting the guidance is based on anything other than a good-faith estimate of where markets are headed, the consequences of being wrong would be far-reaching.

“A key risk is whether these beliefs are justified — and whether pensions can actually pick the best managers,” said Emil Siriwardane, a Harvard researcher who coauthored the paper. “If not, they’re potentially misallocating trillions of dollars of retirement money and paying billions in excessive fees.”

For years, consultants were the quiet voices behind the curtain. Not the fund managers drawing billion-dollar fees or the chief investment officers signing off on exotic strategies, but outside advisers hired by endowments and foundations for guidance, industry insight and sober advice. Meketa, NEPC, Wilshire — along with several others — rarely made headlines. Yet their forecasts — specifically, what they believed alternative assets were worth — quietly reshaped trillions in public retirement money.

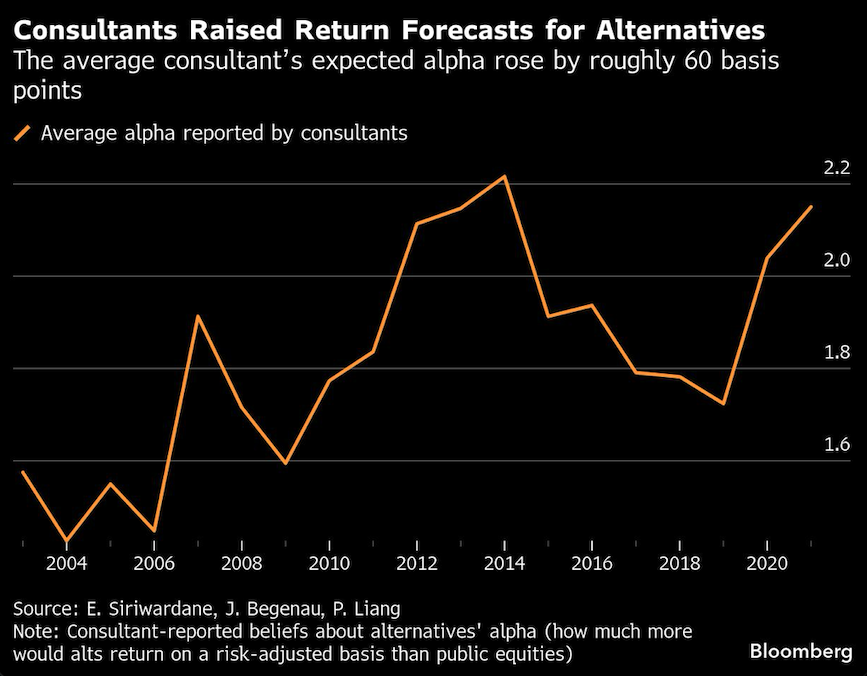

Beginning in the early 2000s, consultants steadily raised their return forecasts for alternative assets. Between 2001 and 2021, the average consultant’s expected alpha — how much more they thought alternatives would return on a risk-adjusted basis than public equities — rose by roughly 60 basis points, the study found.

That’s a significant gain in institutional finance, where every decimal point can move billions. At the same time, consultants didn’t view alternatives more useful for diversification. The beta assigned to alternatives — a measure of how closely an asset moves with the stock market — hasn’t really changed, meaning these private assets were expected to behave more like equities. In effect, consultants were advising pensions to buy more of something that looked like stocks, but still promising it would outperform stocks.

In short: consultants didn’t view alternatives as a hedge. They viewed them as a source of extra return. And that perception — encoded in their capital-market assumptions — became a driver of trillions in asset allocation. Who a pension fund hired could explain a large share of how much they allocated to private assets.

The consulting business is easy to miss next to the swagger of Wall Street’s money-management brigade, but its influence is vast — and increasingly focused alternative investments. The study draws on public pension data compiled by the Center for Retirement Research. Those filings show that plans that identify Wilshire as their consultant report allocating about 34% of assets to alternatives as of 2021. Clients of Meketa and NEPC report roughly similar levels — about 32% and 33%. The three firms together advise funds managing around $5 trillion.

The pace at which pension funds have increased their allocations far outstrips that of the broader investing universe. By 2021, US public pensions were overweight alternatives-to-risky assets by 17 percentage points relative to the global market portfolio — a clear divergence from a neutral asset-allocation stance. Preqin estimates industry assets were about $17 trillion at the end of 2023, rising to $29 trillion by 2029.

According to Harvard’s Siriwardane and coauthors Juliane Begenau and Pauline Liang of Stanford, the best predictor of how much a pension fund allocates to alternatives isn’t its funding ratio or return target — it’s the consultant it works with.

Inside the consulting world, there’s debate over how much sway these advisers truly exert. Steve Foresti, chief investment officer emeritus at Wilshire, argued consultants weren’t the dominant force but helped guide the shift — particularly for plans that could manage illiquidity. He said the move into alternatives reflected more than forecasts: it was a post-crisis world where cash returned zero, traditional portfolios fell short, and funds had little choice but to take on more risk, complexity and illiquidity.

“I’d say consultants have played not the dominant role but have certainly contributed to that trend,” said Steve Foresti, chief investment officer emeritus at Wilshire. “CAPMs are important. They’re obviously a critical input to the process, but reactions to changes in the capital market assumptions are both somewhat muted and then somewhat delayed.”

That view — incremental, cautious, and rooted in institutional pacing — stands in contrast to how some critics see the process. Dan Rasmussen, founder of hedge fund Verdad Advisers, argues capital market assumptions don’t just reflect institutional risk appetites. They shape them.

“Capital market assumptions are not just inputs; they are persuasive tools,” wrote Rasmussen, the founder of hedge fund Verdad Advisers, in an essay about the academic findings. “They define the language of risk, frame the boundaries of plausibility, and legitimate allocation changes.”

In other words, these aren’t just academic observations. They describe how public pensions allocate risk in the real world. And that approach now looks vulnerable — not just to market shifts, but to the slow-motion revision of consultant expectations.

Wildly different estimates exist across academia and finance as to whether alternative assets provide superior returns, and the past is no guarantee of the future. The paper’s authors are agnostic on the wisdom of the consultants’ return forecasts. At the same time, they note, there’s scant evidence pensions with the highest allocation to alternatives outperform their counterparts.

“The big risk of what’s happened is that a lot of pensions invested in these assets on the belief that they were going to deliver really high returns,” said Siriwardane. “And if those beliefs were overly optimistic, then that’s going to hurt both funding and liquidity.”

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.