One of the highest-profile bets on artificial intelligence just came from a most unlikely place. Berkshire Hathaway Inc., led for six decades by value-conscious investor Warren Buffett, disclosed last week that it had taken a sizeable stake in Alphabet Inc. in the third quarter, despite all the handwringing about an AI bubble.

It’s a decidedly un-Buffett-like move to buy a company, even one as well established as Alphabet, whose future relies on yet unproven technology. Never invest in a business you cannot understand, Buffett often warns, a principle that shielded Berkshire from the internet bubble in the late 1990s, and the resulting crash. AI is orders of magnitude more complicated than selling books or pet food online.

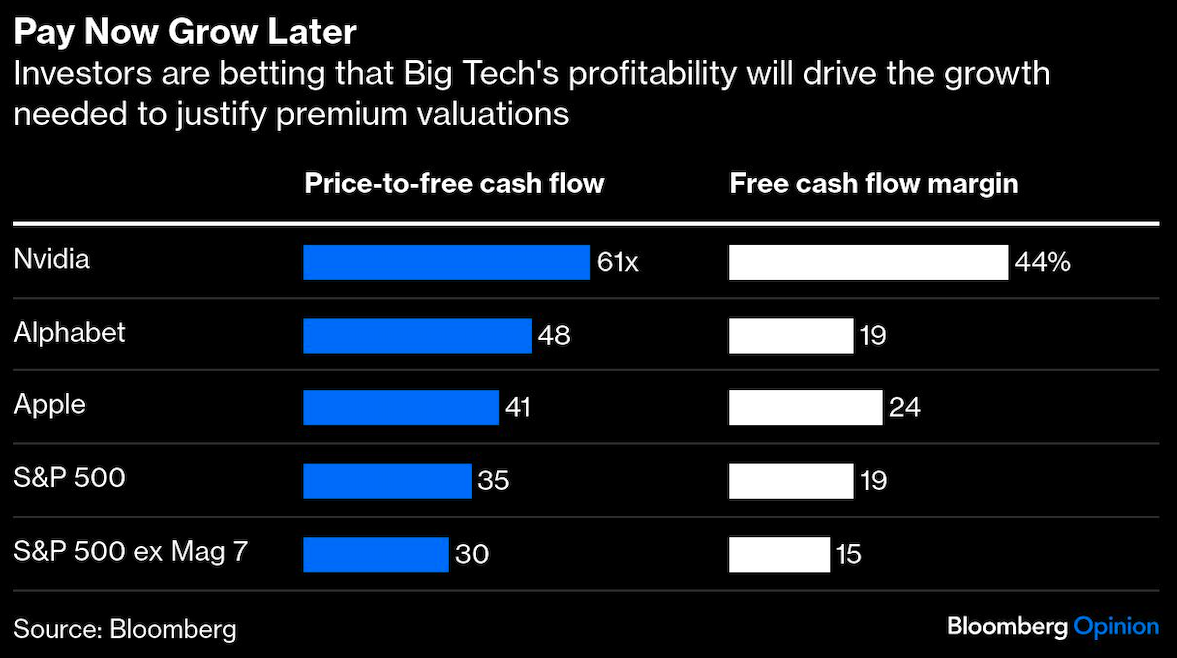

Combine opaque technology with premium valuations, and you’re sure to lose Buffett. Berkshire paid roughly 40 times trailing one-year free cash flow for Alphabet’s shares, which, for perspective, compares with an average FCF multiple of 26 times for the S&P 500 Index since 1991. (Looking at free cash flow, rather than earnings, accounts for the massive capital expenditures tech companies are pouring into AI.) That’s a bigger premium than Buffett typically likes to pay. With Berkshire’s Vice Chair Greg Abel set to lead the company in a few weeks, one gets the impression he may already be making the investment calls.

If so, it previews a very different approach than Berkshire’s shareholders are used to – notably, a new willingness to pay more now for potentially higher growth down the road, a chance Buffett rarely took, if ever. The wager is at the core of the current debate about whether the AI trade is overdone, an argument that intensified this week in anticipation of Nvidia Corp.’s latest earnings announcement on Wednesday.

For good reason. The hype around AI has made Nvidia, the leading provider of AI-related processors, the world’s most valuable company. At more than 60 times free cash flow, a 27% premium to Alphabet, it will have to produce big growth in the years ahead to justify the price.

How big? To land at a multiple that resembles the market’s long-term average, Nvidia will have to grow free cash flow by 33% a year over the next three years or 19% over five years, depending on how much runway investors give it. The company’s blockbuster third quarter results and rosy forecasts certainly point in the right direction.

But the reason Nvidia has a fighting chance to grow into its valuation is not because it says so but because the company is already hugely profitable, even after accounting for its considerable ongoing AI investments. Profitability drives growth, and growth is the difference between promise and payoff, which is why it’s hard to call Nvidia a bubble. Nvidia’s free cash flow margin was 44% for the 12 months through September, and Wall Street expects a margin of 50% in the year ahead. A FCF margin of 20% is considered elite; Nvidia’s profitability is otherworldly.

Even so, some investors are not optimistic. Billionaire Peter Thiel’s hedge fund and Masayoshi Son's SoftBank Group both dumped their Nvidia shares. More broadly, in a recent Bank of America survey of institutional investors, 45% said an AI bubble is the biggest risk to markets. Translation: Never mind profitability, don’t count on growth to bail you out.

That’s the risk with high valuations. Alphabet, too, will have to deliver growth to repay investors, although less than Nvidia given its lower valuation. Free cash flow growth in the range of 13% to 23% over the next three to five years should bring Alphabet’s multiple back to a reasonable level. The tradeoff, though, is that Alphabet has less profitability to work with. Its FCF margin was closer to 19% last year, and Wall Street expects roughly the same this year.

With those numbers in mind, compare Nvidia and Alphabet today with Buffett’s decision to buy shares of Apple Inc. in early 2016, still Berkshire’s largest investment. Back then, Apple traded at 9 times free cash flow yet boasted a FCF margin of 27%. With such a favorable ratio of valuation to profitability – one rarely encountered that low, particularly for a company of Apple’s size and quality – it was exceedingly likely that Apple would leverage its profitability into enough growth to lift its valuation substantially.

Berkshire, in other words, was all but guaranteed to make money. And it did. Apple has returned 28% a year since 2016, including dividends. Half of it came from valuation expansion – Apple now trades closer to 41 times free cash flow – and the rest from earnings growth and dividends.

That makes Apple a totally different proposition today – one that probably wouldn’t interest Buffett. Like Nvidia and Alphabet, Apple’s future returns will have to come from growth given its stretched valuation. If it doesn’t, investors could face a valuation contraction, a scenario Buffett didn’t have to worry about in 2016 when Apple was already dirt cheap.

So, while the AI behemoths may not be a bubble, deciphering which of them will produce enough growth before investors get jittery is certainly a gamble. Abel, if he is indeed behind the decision to buy Alphabet, seems game.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Nir Kaissar