The housing market has been in the doldrums for three years, so it’s easy to assume there’s nothing new to the weakness there. That’s a mistake. The deterioration in housing has taken a fresh turn in recent months with important implications for the economy, particularly given growing skepticism within the Federal Reserve about a interest rate cut in December.

I noted after the Fed’s September meeting that mortgage rates at 6.25% were not sufficient to fix the housing industry’s woes. Some 1.5 percentage points of easing over the past year or so hasn’t resurrected demand enough to stabilize homebuilder profit margins or reduce the incentives they need to offer buyers. The companies are responding by reducing construction, land purchases and headcount.

This continued sluggishness is something of a surprise. Mortgage rates are higher than buyers would like, but they’re toward the lower end of the range we’ve seen since 2022. In that time, income growth has generally outpaced home-price growth, leaving affordability by most measures somewhat better across much of the country.

The new wrinkle has been a weakening labor market, where job growth slowed dramatically in the middle of the year. Federal Reserve Governor Christopher Waller believes that employment likely fell between May and August, something that will be clearer once the data is revised next year, he said Monday. We also learned this week that notices of impending mass layoffs surged in October to one of the highest levels in the past 20 years.

Surveys show that workers are more negative about the labor market than an unemployment rate of 4.4% would suggest, perhaps signaling worries about the next round of layoffs. People who aren’t confident about their employment prospects don’t buy houses, even if affordability has improved a bit.

An additional factor that might be holding some buyers back is the broadening out of home price declines. Zillow put out research this week showing that 53% of homes have lost value since last year, the highest percentage since 2012. Buyers want homes to be more affordable, but they don’t want to invest in something that’s likely to decline in value. It might make sense to wait now for prices to stabilize in the same way as buyers waited for lower mortgage rates.

A bad chicken-and-egg dynamic is at play here. A sluggish labor market has made people reluctant to buy homes, even as affordability improves; while poor homebuying demand is leading builders and other housing-linked companies to lay off workers, further weakening the labor market.

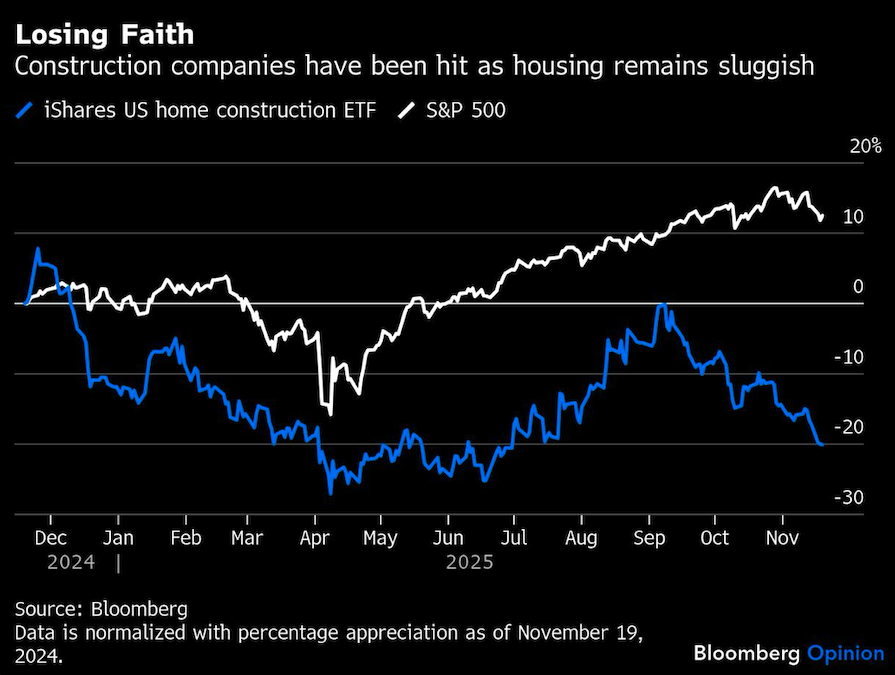

The construction industry shed jobs in June, July and August, and the increase in September is unlikely to be sustained or could be revised lower given the downbeat commentary during recent earnings updates. Stocks have responded accordingly.

Executives at Beazer Homes USA Inc., the most recent homebuilder to report earnings, said last week that they have been able to rebid material and labor costs over the past year to save about $10,000 per home — meaning their suppliers and trade partners have had to eat costs to stay busy. The company also cut headcount.

The one bright spot for construction workers is the boom in data centers, driven by the demands of the artificial intelligence industry. But for many workers there’s going to be a mismatch between where housing demand exists and where data centers are being built. For instance, Meta Platforms Inc.’s $27 billion Hyperion data center is in rural northeastern Louisiana, not somewhere a laid-off construction worker in Florida or Georgia might want to move.

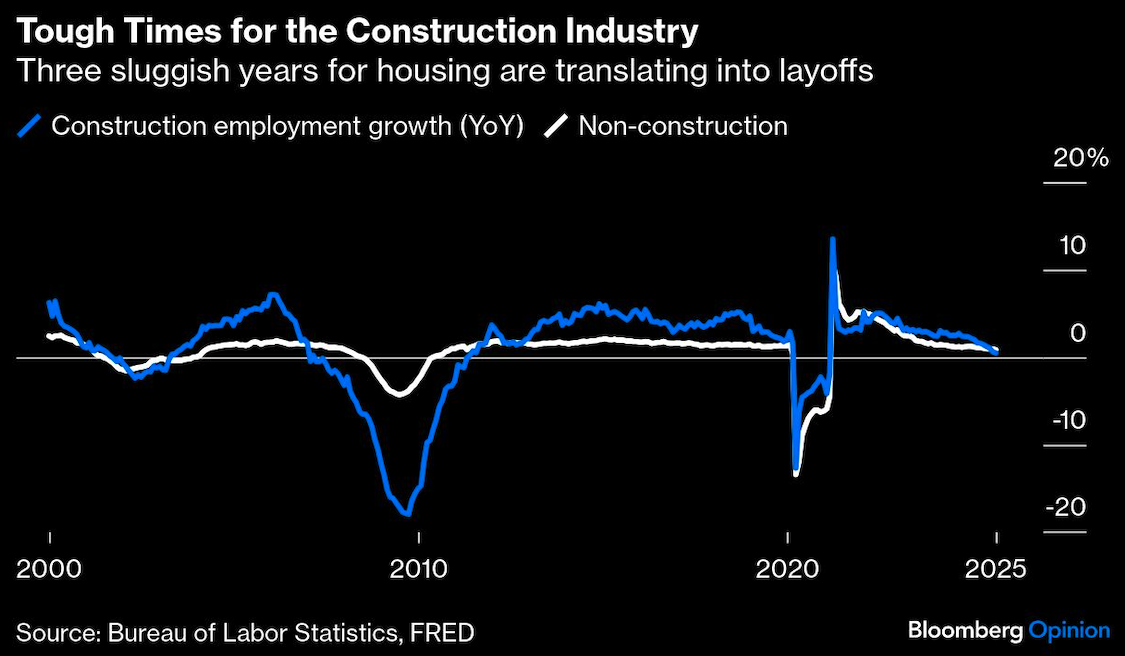

Historically, construction employment tends to lead trends in the broad labor market because it’s highly cyclical, with increases or decreases in construction employment an early indicator of budding strength or weakness elsewhere in the economy. For instance, construction represents just 5% of US employment but accounted for 10% of all job growth between 2011 and 2019.

Housing demand also typically lines up with worker sentiment — a new job or healthy wage prospects will give a household the confidence to take on a mortgage. From that decision flows the need to furnish and perhaps renovate, boosting employment in all sorts of other industries. It’s hard to see the labor market overall remain resilient with headwinds in housing picking up.

There’s also a readthrough from these dynamics to inflation, which remains a concern for many Fed policymakers. Home prices are under pressure and apartment rents, too, have had a slower-than-expected autumn, which over time should continue to push the shelter-related components of the official inflation data lower. As for tariffs, a new working paper from the Federal Reserve of San Francisco shows that historically, tariffs end up lowering inflation by raising unemployment, which is the outcome we’re trying to avoid.

It’s understandable that the Fed is losing patience with frameworks that suggest inflation will continue to moderate when measures of core inflation have not cooled as quickly as expected. Some policymakers may be waiting for a smoking gun from the labor market data to act. But the stresses in the housing and labor markets continue to build and feed off each other, and the pain is only going to broaden out in 2026 if the Fed is slow to act.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Conor Sen