Stablecoins are promising to be the 21st century’s most exciting innovation in payments technology. But do they have a future as everyday money? The answer may lie in a 200-year-old past.

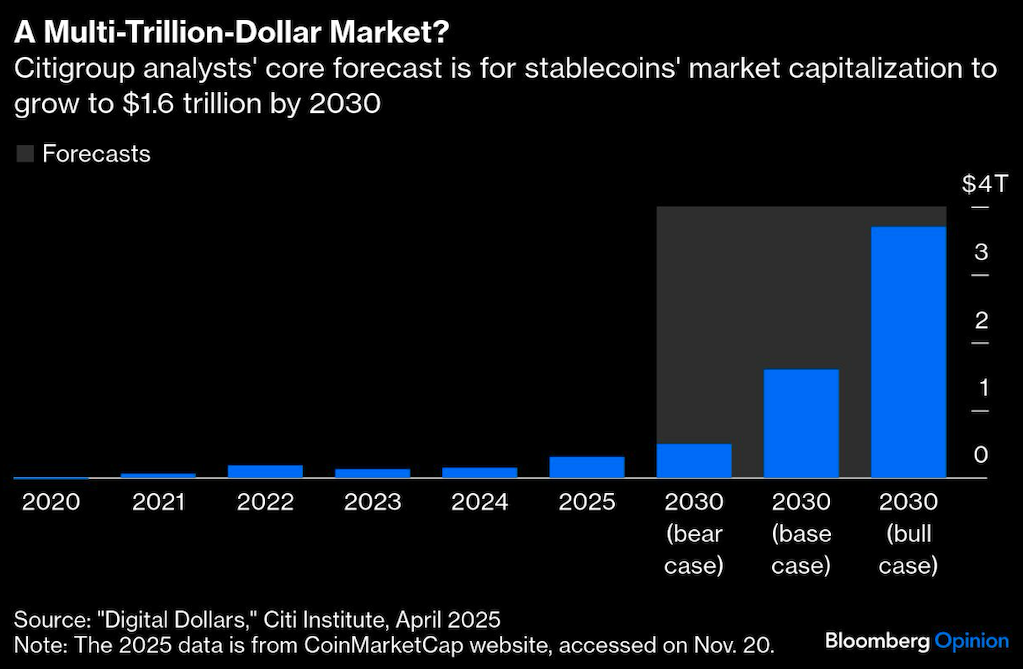

Speculative interest in crypto assets like Bitcoin and Ether waxes and wanes — this year’s surge is fading fast. But in a separate corner of tokens changing hands on the blockchain, coins pegged to fiat money are on the cusp of steadily growing into a mainstream payment instrument worth trillions of dollars.

Those who believe in that optimistic future and those who disagree often cite the same historical evidence: the free-banking era from 1837 to 1863 when commercial lenders — and even railroads — printed their own banknotes.

In 1863, President Abraham Lincoln established the Office of the Comptroller of the Currency and restricted the power to issue legal tender to chartered national banks under quarterly supervision. This ended the chaos that prevailed when, for example, notes circulated by a lender in Tennessee would be discounted by 20% in Philadelphia. Trust in these loosely supervised IOUs’ purchasing power, in terms of how much gold or silver they could buy, was missing. Counterfeiting was rampant, and nobody could be sure if banks had enough assets to cover their liabilities.

Two centuries later, Tether’s USDT, Circle’s USDC, First Digital’s FDUSD and PayPal’s PYUSD aren’t all that different from the private money in circulation before the American Civil War: They claim their tokens are the exact equivalent of the dollar, but in a paperless form. So how can they have a better fate than their 19th-century predecessors? The key may lie in regulation.

In their 2021 paper, Taming Wildcat Stablecoins, Yale School of Management professor Gary Gorton and former Federal Reserve attorney Jeffery Zhang gave a historical account of just how inefficient paper money was in the 1850s. Merchants would employ professional “detectors.” They would scrutinize every bill presented by the customer to see if was dirty and worn — proof of long and successful circulation — and had small holes, further reassuring their owners that it had been through enough banks where slender pins were used to stack them. People relied on specialized weeklies published in major cities to know the discounts on various payment instruments.

To Gorton and Zhang, this violates the basic idea that money should not require due diligence. Its circulation ought to be NQA — no questions asked. Drawing lessons from that history, the scholars discussed various policy considerations for modern-day money, including mandatory 1:1 backing of stablecoins and a new law that would regulate their issuers as banks. They also floated a third option: a central bank digital currency, or CBDC, that would compete against the private sector.

That last alternative, which the Biden administration seemed to favor, went out the window earlier this year. President Donald Trump issued an executive order banning any efforts by a government agency to develop a dollar CBDC. But while handing over the entire profit from digital money to private issuers reprises the free-banking era, the recently passed Genius Act has introduced some important differences.

Regulated stablecoins have to be backed 100% by short-dated, safe assets like Treasury Bills. By prohibiting direct interest payments to token holders, the lawmakers have effectively turned issuers into so-called narrow banks that will focus solely on facilitating payments and won’t take the same risks as commercial lenders.

These are sensible guardrails. Unlike bank deposits, even regulated stablecoins will be uninsured. For people to trust them to hold their value in times of stress, issuers’ behavior has to be strictly monitored. In fact, the support for such controls also comes from the free-banking era.

A new working paper by researchers at the Washington-based Andersen Institute for Finance and Economics argues that 19th-century private money wasn’t all bad. For instance, in 1842, Louisiana required its banks to only hold precious metals or very short-term money-market instruments to back their notes. They also were required to post a weekly summary of their financial statements. In that way, the southern state’s lenders avoided much of the financial panic that plagued that free-banking era.

With similar protections, can Genius-compliant tokens become no-questions-asked money? The answer will depend on how they navigate a real-life run, when coin holders scramble to redeem their tokens for dollars, and the issuer has no option except to raise money by dumping Treasury Bills in a fire sale. The Andersen Institute paper draws a parallel with the 2023 collapse of Silvergate Bank, a crypto industry-focused California institution whose balance sheet resembled a stablecoin.

How will stablecoins manage a similar depositor exodus? At least formally, the Genius Act doesn’t envision a backstop, and there will be howls of protests if the Fed, while making the token holders whole, also bails out private shareholders of the coin issuers. The irony of using public funds to rescue a cryptocurrency, a movement born out of techno-libertarian angst against the role of large custodial institutions in the 2008 Financial Crisis, won’t be lost on market participants.

With far fewer information gaps between issuers and currency holders, money in today’s digital economy may behave very differently from the 19th century. On the flip side, redemptions are also a lot faster now with internet banking. The biggest lesson from a messy history is that after much trial and error, politicians back then decided that money worked best as a public utility. Trump is yet to prove that Lincoln and his successors were wrong.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Andy Mukherjee