To Delay or Not to Delay Social Security? That Is the Question

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.

In a provocative piece in the Wall Street Journal, professor Derek Tharp argued in favor of taking Social Security at 62.

The message: Don’t delay. The rationale: You are better off leaving your portfolio untouched for eight years, even at the cost of a lower Social Security benefit for life.

As the author admits, this is not conventional advice: Social Security is a uniquely valuable retirement income option offering what amounts to an inflation-adjusted life annuity — the go-to choice among nearly all academic authorities.

Nonetheless, Professor Tharp comes down firmly on the side of avoiding the early portfolio withdrawals required while waiting for the bigger age-70 Social Security benefit. And he’s far from alone, with this recommendation trending on social media.

We think that’s bad advice.

The Penalty for Taking Social Security Early & the Bonus for Delay

We’ll start with the case given in the article: Joe Retiree’s Full Retirement Age (FRA) benefit at age 67 of $3000/month—$36,000 per year. That’s close to the 90th percentile benefit, indicating a retiree with a high enough income to have accumulated a decent-sized retirement portfolio.

Taking that benefit five years early at 62 imposes a 30% benefit haircut, to $2,100. On the other hand, delaying three years past 67 earns a 24% bonus, to $3,720. All these values increase by inflation each year, which we will assume is a constant 3%.

Wow — giving up an inflation-adjusted life annuity paying out 77% more! It will take a lot to convince us that’s a smart decision.

Professor Tharp’s rejoinder: Since you have to drain your portfolio for living expenses for eight long years, you’re not getting such a sweet deal. Worse, you collect your benefit for eight fewer years.

What are living expenses?

No matter how long you delay taking Social Security, it likely won’t cover all your living expenses. Hence, if you take Social Security early, you still have to withdraw from your portfolio. However, if you claim at 62, the amount taken out will indeed be less in the early years.

If you delay, your portfolio withdrawal will be larger in the early years, since it has to fund all expenses in the absence of any Social Security payment, but lower after age 70 (because so many more dollars come from the delayed Social Security payment, easing the burden on the portfolio after that point).

So the question of whether to delay is indeed complex. Start by estimating living expenses, which drive the portfolio withdrawal amount. Just before retirement at age 61, in Joe’s high income range, the replacement rate for Social Security runs about 40%; his FRA benefit of $36,000 implies an age 61 income of $90,000 ($36,000/0.4).

How much of that $90,000 is living expenses? Now we come to the great white whale of retirement planning: What percent of income must be replaced in retirement?

Our answer: wrong question. Spending at age 62 must continue at the same level as at age 61. Lifecycle theory demands it: Utility must be smoothed. No one willingly dials back on utility (satisfaction, pleasure, reward) just because the paycheck stops — if they have enough money saved.

So how much of the $90,000 was being spent at age 61? Answer: Every dollar that was not saved, plus every dollar spent on any tax that will not continue after retirement.

Joe Retiree has a portfolio; therefore, he must have been saving. At a 15% rate, he would have put $13,500 into savings at age 61. FICA tax stops when wages stop, but health insurance, before Medicare eligibility, will not cost just 1.45% of $90,000 — the Medicare tax Joe paid on his salary. Trust us. And he has roughly four years before Medicare kicks in.

Call it a $4,000 savings from no FICA tax minus the excess cost of ACA health insurance premiums over Medicare tax plus employer health insurance premiums. (Important! Remember not to get sick between 62 and 65: This messes up the scenario.)

So, to cover living expenses in retirement, including income tax, Joe needs taxable income of $90,000 - $13,500 - $4000 = $72,500

(We ignore the slight tax-favoring of Social Security income in the above calculation.)

Bottom Line

If Joe Retiree takes Social Security immediately at age 62, he has to supplement his $25,200 annual benefit by withdrawing $47,300 from his 401(k) account.

If he delays, then the withdrawal from the portfolio must be the full $72,500. Both dollar figures increase with inflation each year.

Moreover, Joe can’t escape from sequence-of-return risk taking Social Security early. If his paycheck stops at 62, he will start withdrawing substantial amounts from his portfolio regardless.

Next: How big a portfolio does Joe have? We can estimate that number by assuming a constant contribution of 15% of salary over 35 years of wages indexed to wage inflation. (You should be as lucky as Joe: He’s a paragon of stable income.) Wage inflation, used by the Social Security Administration to calculate benefits, runs 1% above price inflation, so we divide the age 61 salary of $90,000 by 1.04 to get the age 60 salary, and so forth, back to age 27.

And where did Joe invest these contributions? Who knows. For the scenario, we assume he’s always invested in the 60/40 balanced fund assumed in The Wall Street Journal (that was, after all, Peter Bernstein’s recommended portfolio for life), with an expected nominal return of 8%. In round numbers, that gives Joe $1,000,000 as he hangs it up on his 62nd birthday and either takes SS early or delays.

That portfolio will stay invested as withdrawals are made and will continue to earn 8% every year.

Whoa! Wait a minute: a risk-free (unvarying) return of 8% every year for 60 years straight? Hey, why not? Ivory tower economists have a license to make stuff up. As we’ll soon see, those who argue for taking SS early need every unrealistic assumption they can find:

- Inexpensive individual pre-65 health insurance;

- Persistently low inflation;

- A decades-long 8% risk-free portfolio return; and

- Salary that started at about $24,000 35 years ago that increased by 4% per year, and contributions of about 15% of salary that compounded at 8%, yielding a nearly $1 million portfolio by age 62.

Guess what: Under these assumptions, the numbers do pencil out: Do not delay Social Security! Take it right away.

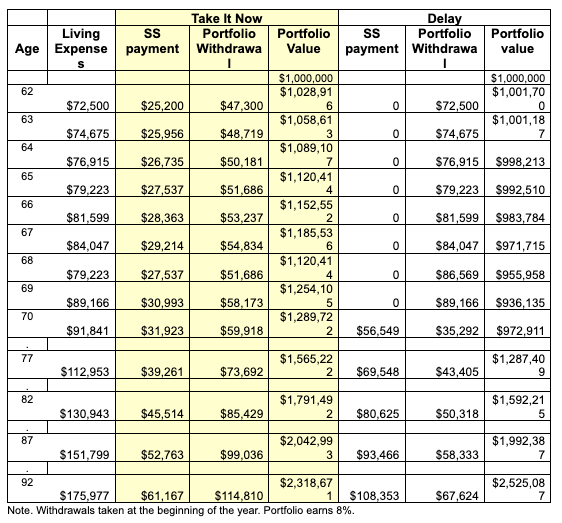

The table below shows portfolio values through 92 under the take-it-now and delay-to-70 scenarios.

In short: The first eight years of heavy withdrawals under the delay case, compared to the smaller withdrawals under the take-it-now case, drain the portfolio to such a degree that it takes a long, long time for the smaller withdrawals after age 70 to overcome the initial hit. On his 70th birthday, Delay Joe has $300K less wealth than Take-it-now Joe.

Only if Joe lives to age 89 does he do better by delaying Social Security. For context: Life expectancy at age 62, for the healthy and well-educated, runs about 25 years. Everyone who dies before 89, which will be rather more than half the population, does better not delaying.

So much from the ivory tower view. We recommend that you step outside it before making life-altering decisions. Let’s challenge these unrealistic assumptions one by one in the following sections:

Don’t Confuse Risky With Risk-Free Returns

Do not, we repeat, do not assume high-returning risk-free stock investments along with low and stable inflation — especially not when in comparison to a lifetime guaranteed inflation-adjusted payday from a money-printing sovereign.

Wait for Medicare Eligibility

The sane person who does not have their back to the wall does not retire until Medicare eligibility is in reach — typically, age 63.5, when COBRA can take you through. Avoiding half years, we reevaluated the question of delay assuming a choice between starting Social Security at 64 or delaying it six years to age 70. Living expenses are higher by two years of inflation, and the starting portfolio size stays at $1,000,000.

Bingo! That one tweak reverses the outcome. The portfolio values now cross over at age 81, well before life expectancy. Six years of big withdrawals are easily overcome by our risk-free, pays-8%-forever portfolio. At age 92, Delay Joe has $750K more wealth than Take-it-now Joe.

Suppose Joe Has Less Money

One problem with even the tweaked scenario: Delay or no, Joe manages to fund 30 years in retirement and still has twice as much money as when he started. That sounds … unrealistic. Or unrepresentative.

Let’s rerun the scenarios with lower starting portfolio sizes. Assume that the first Revised Joe got that smaller portfolio because he only earned 7% while saving; the second earned 7% and only saved for 30 years. These two versions of Joe Retiree also earn only 7% after retirement (a 40/60 portfolio, perhaps). These small changes — while retaining the unrealistic assumption of a high-return, risk-free rate — have a substantial effect.

This scenario starts Joe out with only about $800,000. Take-it-now Joe runs out of money at age 87. All he’s got thereafter is his reduced SS benefit, about 1/3 his living expenses. We’re talking cat food. Meanwhile, Delay Joe sees his portfolio last 6 more years to 93. His enhanced SS benefit will be 61% of hoped-for living expenses — think mobile home park, not cat food. Or maybe he’s slowed down by 93 and, given a good rocking chair, 61% is enough income.

At $600,000 saved? Shudder. They both exhaust their portfolios about 79. But again, Delay Joe has remnant SS income 77% higher. For the rest of his life.

Then Inflation Pops

Okay, back to a portfolio of $800,000.

In this next run, we spike inflation to 10% for three years, at ages 65, 69, and 74. That’s not hyperinflation—these three hiccups only take the 30-year annualized rate up to 3.73%.

Take-it-now Joe runs out of money at 81 and Delay Joe one year later. For the rest of his life, Delay Joe’s benefit is 77% larger.

Now Give Joe an Actual Balanced Fund

Keeping the inflation pops and the $800K portfolio, we’ll next substitute the actual record of the Vanguard Balanced Index fund from December 1999 through 2024, potentially taking Joe out to age 89.

Whoop! Joe exhausts his portfolio at age 76 under either plan. As before, Delay Joe spends the rest of his life with 77% more social security income than Take-it-now Joe. (For two decades, if Joe makes it to the age of Ed’s father-in-law.)

Outside the ivory tower, the early 2000s were a bad stretch for the 60/40 portfolio, with a nominal annualized return of but 3.3% through Joe’s 76th birthday.

What part of “risk portfolio” do you not understand?

Oh, and one more thing: We almost forgot to tell you that Joe is married. You do know that Social Security gives you a free spousal benefit, right? If both Mr. and Mrs. Joe are of average health, at age 62 their joint life expectancy is 91. But, of course, their high income increases that by a few years. And if neither of them smoke, there’s a 10% chance one of them — likely Mrs. Joe — makes it to age 100, at which point a 77% larger benefit will likely save their kids and grandkids a tank car of grief.

Conclusion

In a fantasy world of high risk-free returns, always-controlled inflation, no worries about health insurance, no spouse to worry about — particularly a female one — and a precisely scheduled death, you might, possibly, do better by taking social security at age 62 rather than delaying to 70.

In the real world, where your risky portfolio may not return much, inflation is unruly, you prudently wait for Medicare, and then either your or your spouse happen to reach a ripe old age — delay is a powerful strategy for putting a high floor under your income for as long as you live, regardless of what happens to your portfolio.

That faint whooshing sound you hear up in the attic is the ghost of Blaise Pascal trying to warn you about asymmetric consequences — in this case Delay Joe’s risk of leaving some stock money on the table versus Take-it-now Joe’s risk of an impoverished old age — for himself and his spouse.

Wait, Joe, wait: That’s our advice.

Postscript: A married couple, given spouses with different ages and income histories, faces much more complicated claiming choices. We recommend Mike Piper’s Open Social Security site as a place to begin.

Edward F. McQuarrie, Ph.D., is professor emeritus at Santa Clara University. He writes about financial history and its implications for retirement planning. Working papers describing his research can be downloaded here.

William J. Bernstein is a neurologist, the co-founder of Efficient Frontier Advisors, an investment management firm, and a writer with several titles on finance and economic history. He has contributed to the peer-reviewed finance literature and has written for several national publications, including Money Magazine and The Wall Street Journal. He has produced several finance titles, and four volumes of history, The Birth of Plenty, A Splendid Exchange, Masters of the Word, and The Delusions of Crowds about, respectively, the economic growth inflection of the early 19th century, the history of world trade, the effects of access to technology on human relations and politics, and financial and religious mass manias. He was also the 2017 winner of the James R. Vertin Award from the CFA Institute.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All