Private credit losses from borrowers defaulting remain low — so has everyone just “lost their minds” and the press got “hysterical” about the risks, as Apollo Global Management Inc. Chief Executive Officer Marc Rowan says? Not entirely.

The lack of transparency is one reason that investors, and journalists, could be more fearful than is warranted by historical performance, as I’ve written plenty about. But there’s illuminating data, too, from analysts and ratings companies that show the outlook for repayment problems and bankruptcies isn’t great. In fact, it’s getting worse.

To be clear, I’m talking about junk-rated loans made by private credit funds to mostly midsized companies — often used to fund private equity buyouts and similar to the leveraged loans that banks underwrite and sell to investors. This direct-lending market is different to what Rowan is talking about when he defends the sector. He’s concerned mostly with private investment-grade debt in various forms that his firm creates as assets for its life insurance business.

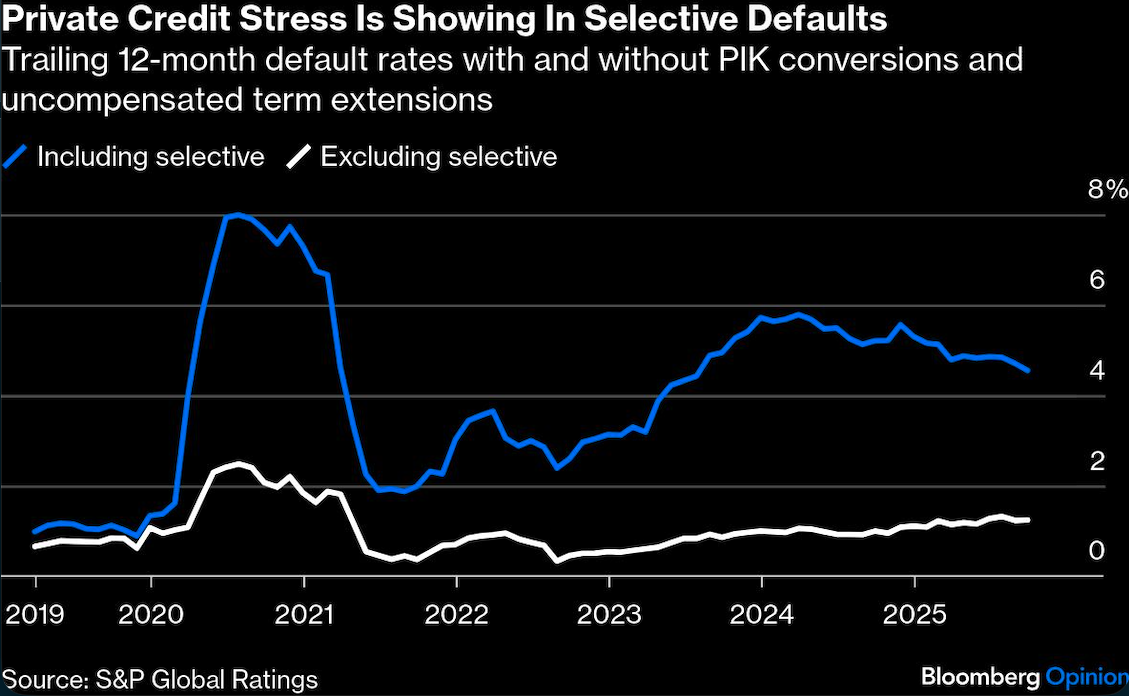

Defaults among junk-rated private borrowers have climbed steadily since US interest rates began rising late in 2022. The trailing 12-month default rate hit 1.3% of all loans this summer, up from less than 0.5% in August and September 2022, according to S&P Global.1 For comparison, default rates were as high as 2.5% during the peak of Covid-19 in summer 2020, and were pushing 15% during the financial crisis in 2009. In short, it’s still pretty low.

But that’s only part of the story. S&P also tracks “selective defaults,” where loans don’t go completely bad but borrowers change the terms to give themselves breathing room. In private credit this mainly involves adding interest to the value of the loan, rather than paying it with cash (turning the debt into a so-called Payment-in-Kind, or PIK, loan). Or companies extend maturities without paying compensation to the lenders.2

Add in this stuff and the default rate is a much higher 4.6%. That’s better than a recent peak of near 6% in March last year and the 8% of summer 2020. There’s no data for 2009 because S&P didn’t monitor selective defaults back then.

Selective defaults are a bad sign. These companies can’t pay the interest on their debt or meet looming maturities out of their income. Lenders haven’t lost real money yet, but their borrowers are definitely in trouble. And more businesses are heading in this direction. About 15% of private credit borrowers aren’t generating enough operating profit to cover interest costs, according to Goldman Sachs Asset Management in its 2026 investment outlook. “Rate cuts can marginally alleviate stress for distressed borrowers, but we expect their overall impact to be limited,” the firm wrote.

The health of many borrowers has deteriorated over the past couple of years, especially in the retail and chemicals industries, according to the Kroll Bond Rating Agency. Credit downgrades have outpaced upgrades for seven quarters in a row, KBRA said this week. That leaves a record number of borrowers with KBRA’s weakest ccc-minus rating, the last stop before a default. So there’s about $14 billion of debt teetering on the brink.

Hard-pressed companies are having to cope with falling revenue, rising leverage, cash shortfalls and upcoming maturities, which could all worsen if the economy softens further, or other policies like tariffs shrink profit margins. “These and other borrowers under stress are likely to face increased refinancing difficulties and elevated risks of default that we believe will force a reckoning for some,” KBRA wrote. It’s expecting defaults to pick up in 2026.

Private credit has grown massively in recent years and lots of people are worried about whether some fund managers have expanded too fast and taken too many underwriting risks.

Not everyone is in trouble. Companies that borrowed before interest rates plunged at the turn of the decade, and when traditional leveraged-loan markets were shuttered, ought to be in a better position. Many have been able to refinance at lower rates since banks got back into the game over the past year or two.

But a lot of borrowers who took on debt in 2021 and 2022 just before interest rates jumped are likely to be enduring severe pain. Many more of them will likely succumb next year — and investor fears about private credit will become undeniably more real.

1. The private-credit ratings behind this data are done by S&P Global for managers of collateralized loan obligations (CLOs), vehicles that invest in this debt. They aren't the same as private letter ratings paid for by borrowers.

2. Private credit doesn’t have the creditor-on-creditor violence – or liability management exercises – that have become a regular occurrence in leveraged loan markets.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul J. Davies