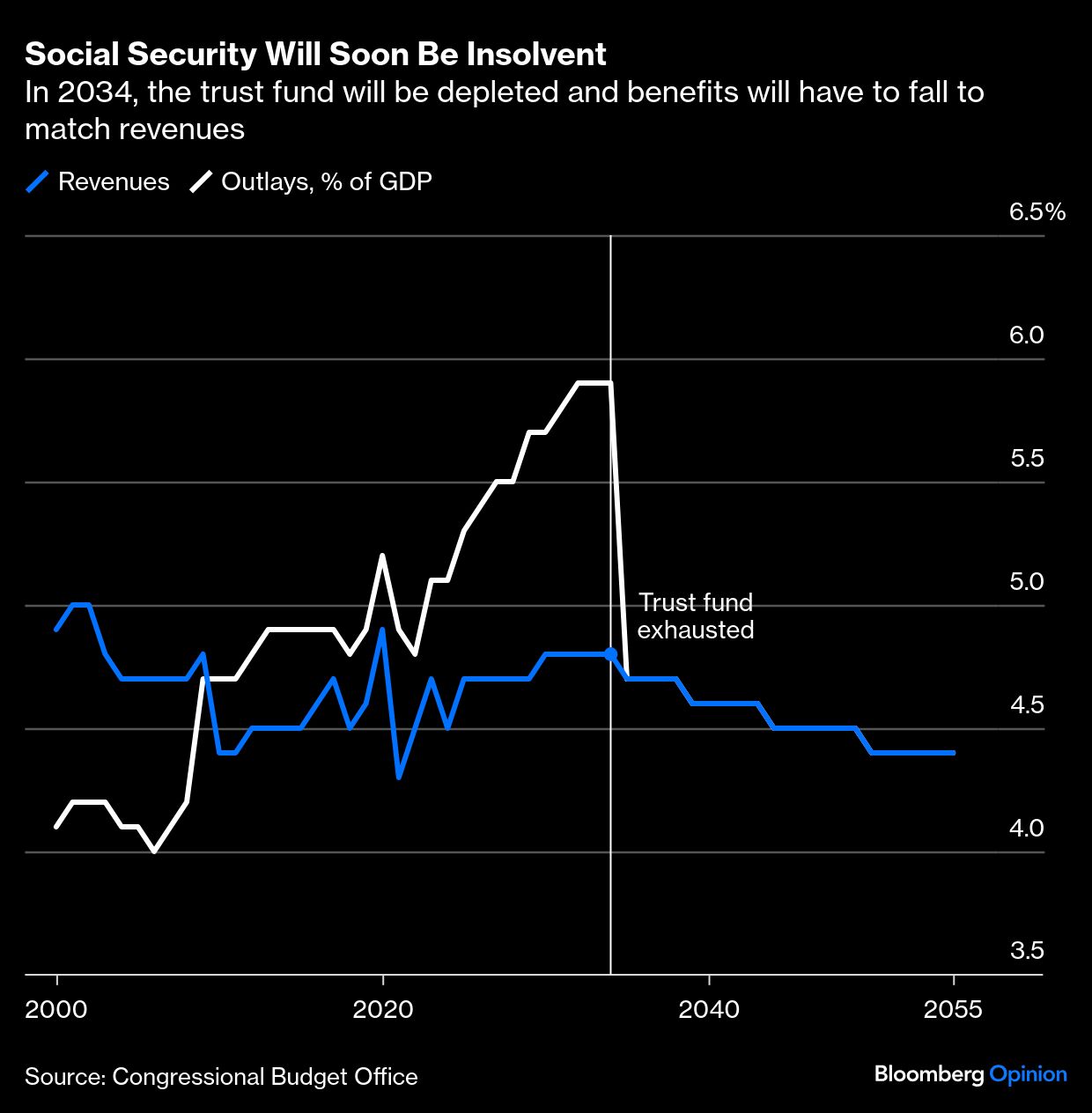

If there’s one thing Democrats and Republicans have agreed on in recent years, it’s to ignore the rapidly deteriorating finances of Social Security and keep its unsustainable benefits intact. The longer they dither, the worse the problem will get.

The system’s two trust funds — one for the elderly, one for the disabled — are both on course to be depleted by 2034, at which point automatic benefit cuts of about 20% are supposed to kick in. That compressed timescale means there’s no easy fix. Tweaks that phased in gently while protecting current beneficiaries could’ve balanced the books by now if they’d been done many years ago. Starting from here, they won’t suffice to avoid the programs’ imminent insolvency.

What’s needed is a combination of short-term action to stave off insolvency and technical fixes to bolster the system’s finances over the long haul. The most obvious longer-term reform would be to gradually raise the full retirement age (from 67 to 69, say) and then link it to changes in life expectancy. This would close about a third of the shortfall over 75 years.

Another valuable change — discussed for years but never implemented — would be to use a different measure of prices when updating benefits for inflation. At the moment, the system uses the standard measure of consumer price inflation. According to the Bureau of Labor Statistics, that figure will rise by 2.8% next year.

Yet this method is flawed: It ignores changes in what people buy when some prices rise faster than others. The so-called chained CPI was designed to correct for this. Since the 2017 Tax Cuts and Jobs Act, it’s been used to index tax brackets. Over time it tends to rise more slowly than the normal CPI. Using it for Social Security would cut the long-term funding gap by another fifth.

Both those changes would make sense even if the system weren’t about to go bust and would be fiscally helpful over the long haul. But avoiding the imminent crunch will require changes to spending or revenue that work much faster.

The simplest such reform would be to increase the payroll tax (currently 12.4%, split equally between workers and employers). An increase of 3 to 4 percentage points would delay insolvency for decades and go far toward eliminating the long-term shortfall. But a much higher payroll tax would hit those in the lowest incomes hardest — and would be especially challenging politically.