Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

- Stock market valuations are driven more by investor risk appetite, as reflected in the P/E ratio, than by earnings growth alone.

- The current market P/E of 30 is historically high, indicating strong investor willingness to take risk for future earnings streams.

- Even with high earnings growth, returns could be negative if P/E ratios contract toward historical norms, highlighting the risk of overpaying.

- Return expectations should focus on potential P/E expansion or contraction, not just projected earnings growth, as investor sentiment is crucial.

I’ve been reading a lot lately that the stock market is priced just right because earnings growth is expected to be high, growing at double digits. But earnings growth is not the sole determinant of stock price. Investor preference for risk versus return is the primary determinant, as reflected in the price/earnings (P/E) ratio.

Setting a P/E Ratio

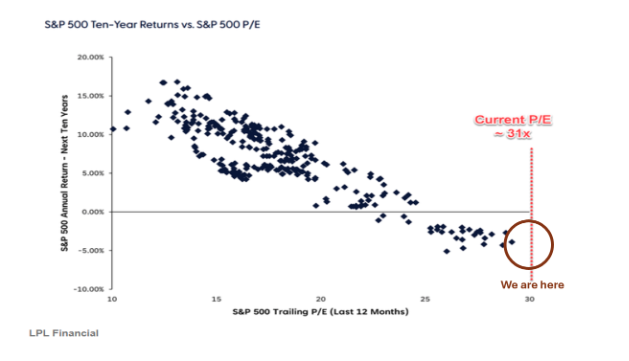

P/E is the price you’re willing to pay for each dollar of earnings. The P/E on the stock market is currently 30, meaning that investors are paying $30 for each dollar of current earnings. Why would anyone pay $30 in order to get $1 back? Because investors are buying the stream of future earnings. That $30 buys participation in all future earnings, with high expected growth on key stocks shown as follows.

Sure, expected growth is high. But how do we know that $30 is the “right” price to pay? We need to estimate what our return will be based not just on earnings growth but also on changes in P/E, whether expansion or contraction. P/E reflects investor appetite for risk. The current P/E is very high relative to history, implying high willingness to take risk. However, if investors become more cautious, P/Es will contract.

Expected Returns

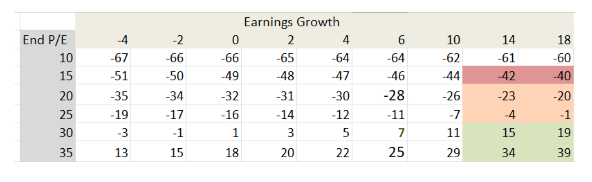

The following table shows next year’s returns for various combinations of earnings growth and ending P/E.

Let’s focus on the high earnings growth columns on the far right, growing between 14% and 18%. If P/Es remain at 30 or expand to 35, the 2026 return on stocks will range between 15% and 39% — very good. But if P/Es contract down to 25 or 20, stocks will decline between 1% and 23% — not good — despite high earnings growth.

If P/Es decline all the way down to their historical level of 15, stocks will lose 40% even though earnings are growing nicely. Simply put, high earnings growth will not save the day.

Ben Graham

Ben Graham said: "Our basic recommendation is that the stock portfolio, when acquired, should have an overall earnings/price ratio—the reverse of the P/E ratio—at least as high as the current high-grade bond rate."

Using an AA yield of 4.53% (from The Wall Street Journal) and P/E of 30, the stock market earnings yield of 3.33% is below Graham’s minimum; Graham would view the market as rich by his rule. P/Es would need to decline below 22 (E/P = 4.53%) to indicate a fair price, resulting in a 20% loss.

Graham’s rule is a simple, conservative screen. It's a useful starting point, but not the whole decision. He would likely advise either waiting for valuations to compress, shifting to higher-yielding/cheaper stocks, or insisting on a margin of safety in other forms (strong balance sheets, stable earnings) before committing to stocks at current levels.

Conclusion

The point is that high expectations for earnings growth do not justify high P/Es. Investor behavior determines P/Es. Our return expectations need to hinge on our expectations for P/E expansion or contraction, rather than earnings growth. Which do you see happening? Will P/Es contract or expand?

Ron Surz is president of Target Date Solutions, developer of the patented Safe Landing Glide Path and Soteria personalized target date accounts. He is also co-host of the Baby Boomer Investing Show. Surz’s passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book, “Baby Boomer Investing in the Perilous 2020s,” and he provides a financial educational curriculum.

For anyone who relies on TDFs — or advises those who do — Surz’s new book is a must-read guide to understanding the risks, solutions, and future of a secure retirement.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Ron Surz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.