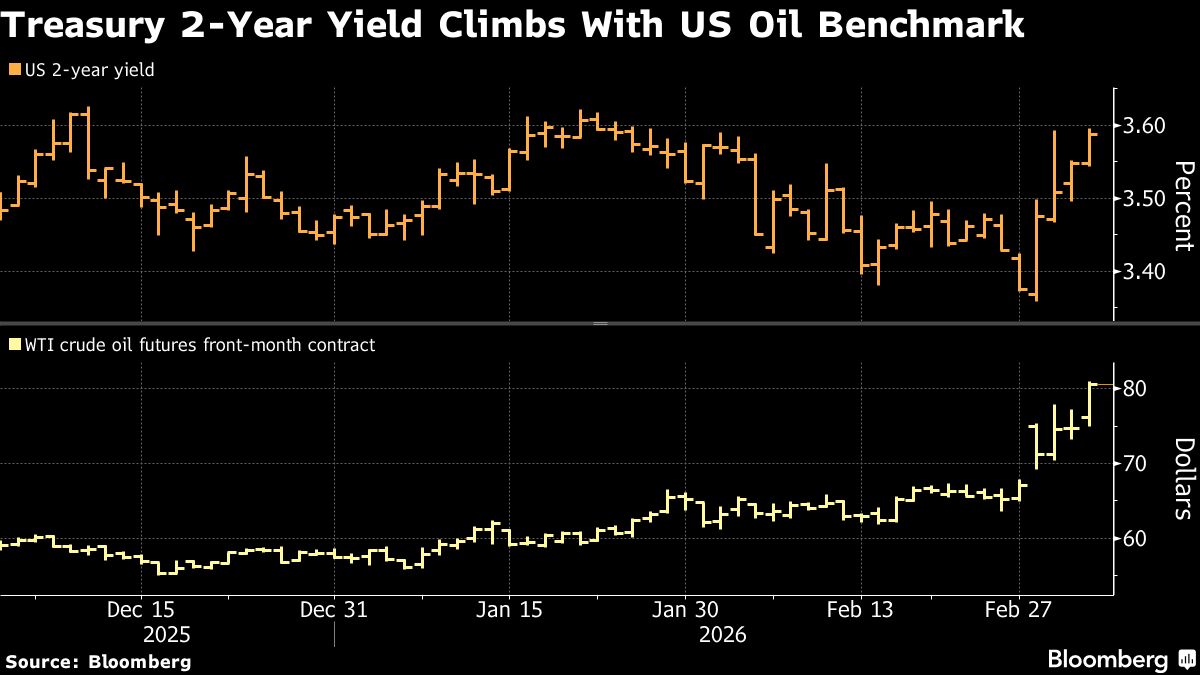

Treasuries fell for a fourth day — lifting yields to the highest levels in several weeks — as rising oil prices ignited inflation expectations and dented the outlook for Federal Reserve interest-rate cuts.

Yields for most tenors were three to four basis points higher as the US benchmark crude oil futures contract topped $81 a barrel for the first time since mid-2024. It’s climbed from under $70 this week after the US attacked Iran on Feb. 28, leading traders to wager on a later start to any Fed cuts this year.

Short-term inflation expectations soared, and traders abandoned wagers on more than one quarter-point rate cut by the Fed this year. As recently as the end of last week, two cuts were fully priced in. Also, data compiled by the Fed’s Atlanta branch indicated the market-implied odds of no move this year were about 25%, up from 17% on Friday.

“In the short term, rising oil prices feed through to higher bond yields,” said Noah Wise, a senior portfolio manager at Allspring Global Investments. “It does complicate things for the Fed.”

The one-year US inflation swap rate — representing the expected annual growth rate of the consumer price index — jumped more than 10 basis points to about 2.75%, the highest level since November. The CPI rose 2.4% over the 12 months through January.

Fed policymakers, who cut interest rates three times last year in response to a softening labor market, paused in January, with several expressing the view that inflation remained too high to lower rates further in the short term.

While the selloff stalled amid declines in US equities and a flurry of buying in Treasury futures, it was backstopped by the US government’s weekly tally of new jobless claims. The initial claims figure was slightly lower than economists estimated, a sign of labor-market strength and another challenge to wagers on Fed interest-rate cuts that benefit bonds.

“The market is not going to trade on economic data today,” said John Brady, managing director at RJ O’Brien. “It remains about the widening war in the Middle East and the energy markets.”

Meanwhile, the February US employment report to be released Friday is expected to show deceleration in job growth, potentially reviving the case for Fed rate cuts.

Yields on two-year notes, more closely tied than longer tenors to Fed rate changes, rose as much as five basis points toward 3.60%, the highest since Jan. 28. They’re about 20 basis points higher on the week, the biggest increase since April. The 10-year yield was around 4.13%, the highest since Feb. 12.

Swaps markets are currently pricing in about 35 basis points of rate cuts by year-end, compared with 60 basis points at the end of last week. At the time, a quarter-point cut was fully priced in by July. That shifted to September, and confidence in a move before October is slipping.

Speaking Thursday, Richmond Fed President Tom Barkin said inflation risk stemming from fuel prices had policy implications, and that the trend in consumer prices “certainly puts pause to any conclusion that we’re done fighting this.”

Adding to upward pressure on Treasury yields, sales of new corporate bonds were set to be heavy again, with 18 borrowers in the arena, the most in two months. Wednesday’s $17.7 billion haul by five issuers began to clear a backlog that developed over the previous two days as the onset on Middle East hostilities eroded risk appetite.

The corporate borrowing surge was accompanied by strong demand to receive long-dated US interest-rate swap rates, driving them lower relative to corresponding Treasury yields and further collapsing the spreads between them.

Many other government bond markets suffered steeper losses than Treasuries, particularly European markets, where most 10-year yields ended the day at least nine basis points higher.

Oil benchmarks extended their advance after reports China told its largest oil refiners to suspend exports of diesel and gasoline due to the escalating conflict in the Persian Gulf. Brent crude exceeded $85 a barrel, extending this week’s gain to more than 15%.

“Higher oil, especially for longer, is going to pressure nominal yields higher,” said Kenneth Crompton, senior fixed-income strategist at National Australia Bank Ltd. “And Treasury yields, in our view, were too low to start with before hostilities began.”

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Ye Xie and Michael MacKenzie