Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

- Target date funds (TDFs) need modernization. Their set-it-and-forget-it approach limits participant engagement, and most TDFs expose investors to excessive risk near retirement.

- Integrating academic lifetime investing theory with personalized risk tolerance offers a superior framework, enabling investors to adjust as they age and as preferences change.

- Investors should actively assess their risk tolerance, compare the associated model in this article with TDF allocations, and consider shifting to more personalized allocations if misaligned.

Yaqub Ahmed is Global Head of Retirement, Workplace & Wealth with the FIRST Organization (Franklin Innovation Research Strategies Technology). Discussing his research with the National Association of Plan Advisors in 5 Trends Shaping the Future of Retirement he "claimed the industry created somewhat of a monster with target-date funds, with its ‘set it and forget it’ mindset, thereby limiting participant engagement." He also explained that:

Some may argue that it’s a better approach, but we believe participants are far from disengaged [. . .] They want to be involved—they just don’t know where to start. The real issue is that we’re not effectively activating those engagement levers.

TDFs are crying for improvements, and those changes are just beginning to coalesce. This article is about contemporary models that enable personalization. These improvements apply to both retirement savings plans and IRAs — in other words, to all tax-deferred savings. Most of all, this article is about substantive prudence, which is doing what is best and what is right.

Better Models

Investment models are ubiquitous. Investors can get them from just about any money manager — using that manager’s funds, of course.

In this article, I present a framework for investment models that integrates personal risk tolerance with academic lifetime investing theory that guides risk as the investor ages.

To keep things simple, I use just two types of assets — a well-diversified portfolio of risky assets and a safe asset like T-bills. Ibbotson Associates labeled this approach the “Separation Principle.” You can identify the model that is best for you and implement it with your favorite risky and safe portfolios, potentially with the help of an investment advisor.

Framework

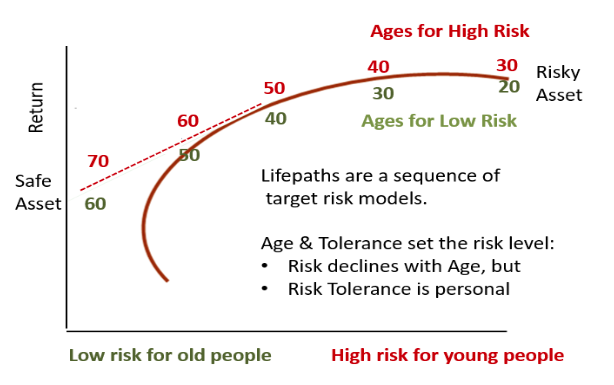

My models are a sequence of target risk models along the efficient investment frontier such that your position on the frontier is a function of your age and your risk tolerance, as shown in the following graphic:

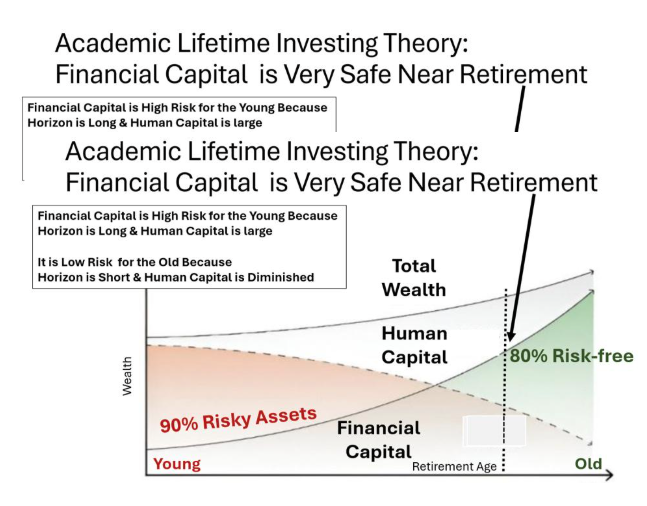

Academic lifetime investment theory sets the risk level based on age. It integrates human capital with investment capital as follows:

As our human capital depletes, we become increasingly dependent on our investments, so theory indicates that our investments can be risky when we’re young, but we should become less risky as we age. As we are near retirement, theory suggests very low risk levels, as shown in the following graphic:

We all have personal feelings about risk that influence our risk preferences. Behavioral scientists tell most of us that we are risk averse — we just don’t like it. But some people are risk takers, and they want their money to work really hard. Academic theory sets the standard for the risk-averse majority, but an individual can override theory. Hence, the red ages in the efficient frontier graph above.

This theory can guide the investor into retirement, at which point, I turn to a different theory.

Investing in Retirement

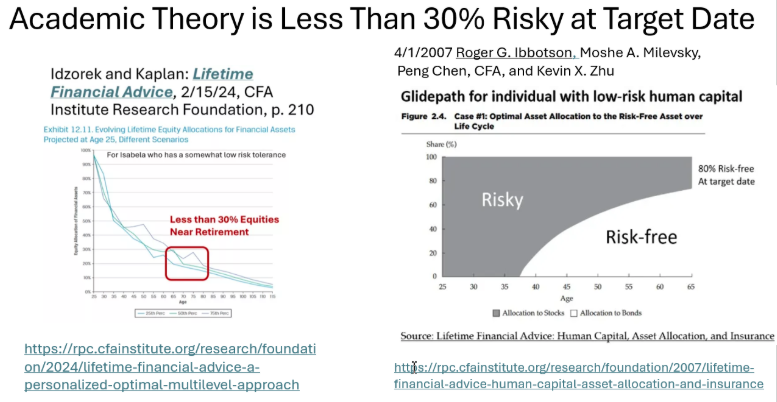

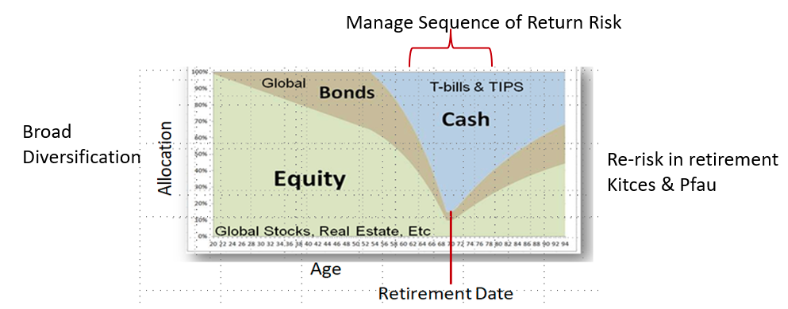

The academic theory for investing in retirement was introduced in Kitces and Pfau’s 2013 paper, “Reducing Retirement Risk with a Rising Equity Glide-Path.” Kitces & Pfau make a very persuasive case for entering retirement with low risk and then re-risking in retirement. We all pass through three stages of investing. The second stage encompasses the transition from working life to retirement, and during that phase, assets should be very safely invested.

Connecting with pre-retirement theory, the pre-retirement glidepath needs to end safely so that it leads into a post-retirement path that starts safely but gradually re-introduces risk, creating a U shape as shown below.

Implementation

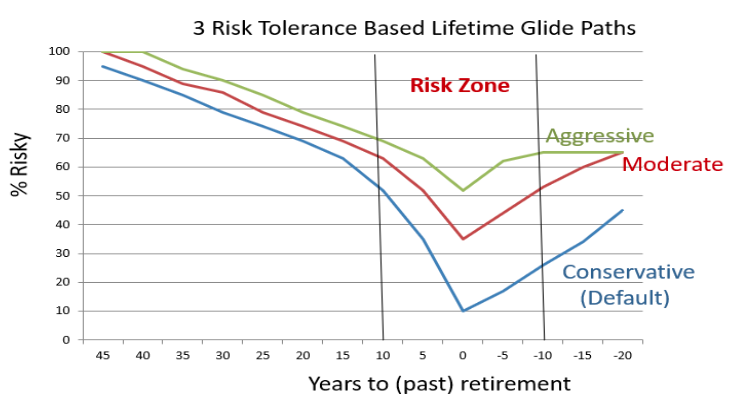

Acknowledging different levels of risk tolerance requires several lifetime glidepaths, as shown in the following:

Investors can blend these glidepaths, and they can change their risk tolerance at will. This provides a framework for investment models.

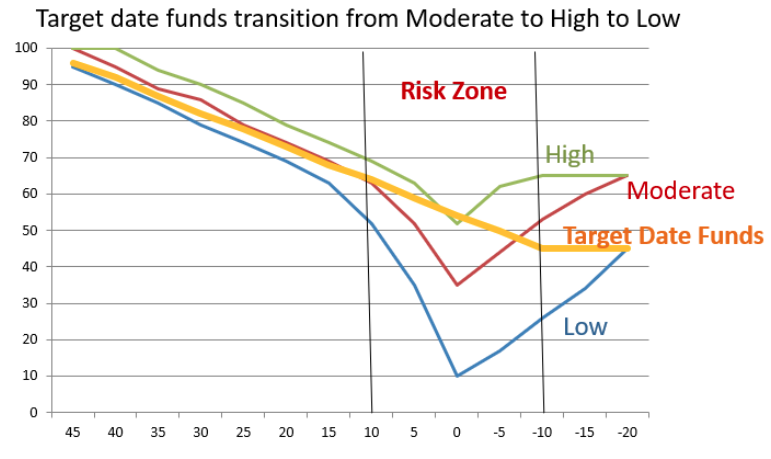

How Do One-Size-Fits-All TDFs Fit in This Model?

TDFs are all very similar and fit into my model framework as shown in the graphic below:

The Risk Zone is the 5 years before and after retirement, and re-risking begins as you leave the Risk Zone. The graph shows that TDFs take moderate risk until they reach the Risk Zone, when they become high risk, and then in retirement they become low risk.

Note that participants in the Risk Zone are taking high risk. They don’t know it, but they will when the stock market crashes. A crash will be a “good” thing because it will expose this high risk, opening the door for improvements. Substantive prudence will morph into procedural prudence.

Conclusion

Albert Einstein said that everything should be as simple as possible, but no simpler. Here is a simple universal investment framework to implement as you move through the stages into retirement.

- Think about your risk tolerance. Most of us have low risk tolerance, but you might be different.

- Find your risk tolerance path (low, middle, or high risk) in the last graph above and locate yourself on the horizontal axis by finding the number of years that you are away from retirement, and then look to the left for an allocation to your diversified risky portfolio.

- Act.

a. Is the answer similar to your current portfolio? This will either confirm or call into question what you’re currently doing.

b. If you’re invested in a target date fund, how close is your answer to that TDF? If it’s not close, consider getting out of your TDF, especially if it’s riskier than your answer.

Ron Surz is president of Target Date Solutions, developer of the patented Safe Landing Glide Path and Soteria personalized target date accounts. He is also co-host of the Baby Boomer Investing Show. Surz’s passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book, “Baby Boomer Investing in the Perilous 2020s,” and he provides a financial educational curriculum.

For anyone who relies on TDFs — or advises those who do — Surz’s new book is a must-read guide to understanding the risks, solutions, and future of a secure retirement.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Ron Surz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.