The scariest portmanteau in macroeconomics is making a comeback in market discourse: stagflation.

The US-Israeli conflict with Iran has effectively halted tanker traffic in the Straight of Hormuz, a critical chokepoint for the global supply of energy commodities, sending Brent crude prices above $100 a barrel for the first time since 2022. The events stand to exacerbate inflation that’s been stubbornly elevated for five years and hit an economy that, according to data released Friday, expanded at just a 0.7% annualized pace in the fourth quarter. Meanwhile, the US labor market looks brittle and susceptible to any hit to consumer confidence.

You can understand why people might be nervous. But are we really at risk of stagflation?

At least from the US perspective, stagflation has become synonymous with the 1970s — a macroeconomic dumpster fire that bears no resemblance to today’s economy. That decade saw average inflation of 6.4%1 and two recessions even before a forceful monetary policy response precipitated a third downturn in 1980. Stocks, bonds and cash all lost ground in inflation-adjusted terms, and the big outperformers of the era were gold and energy commodities.

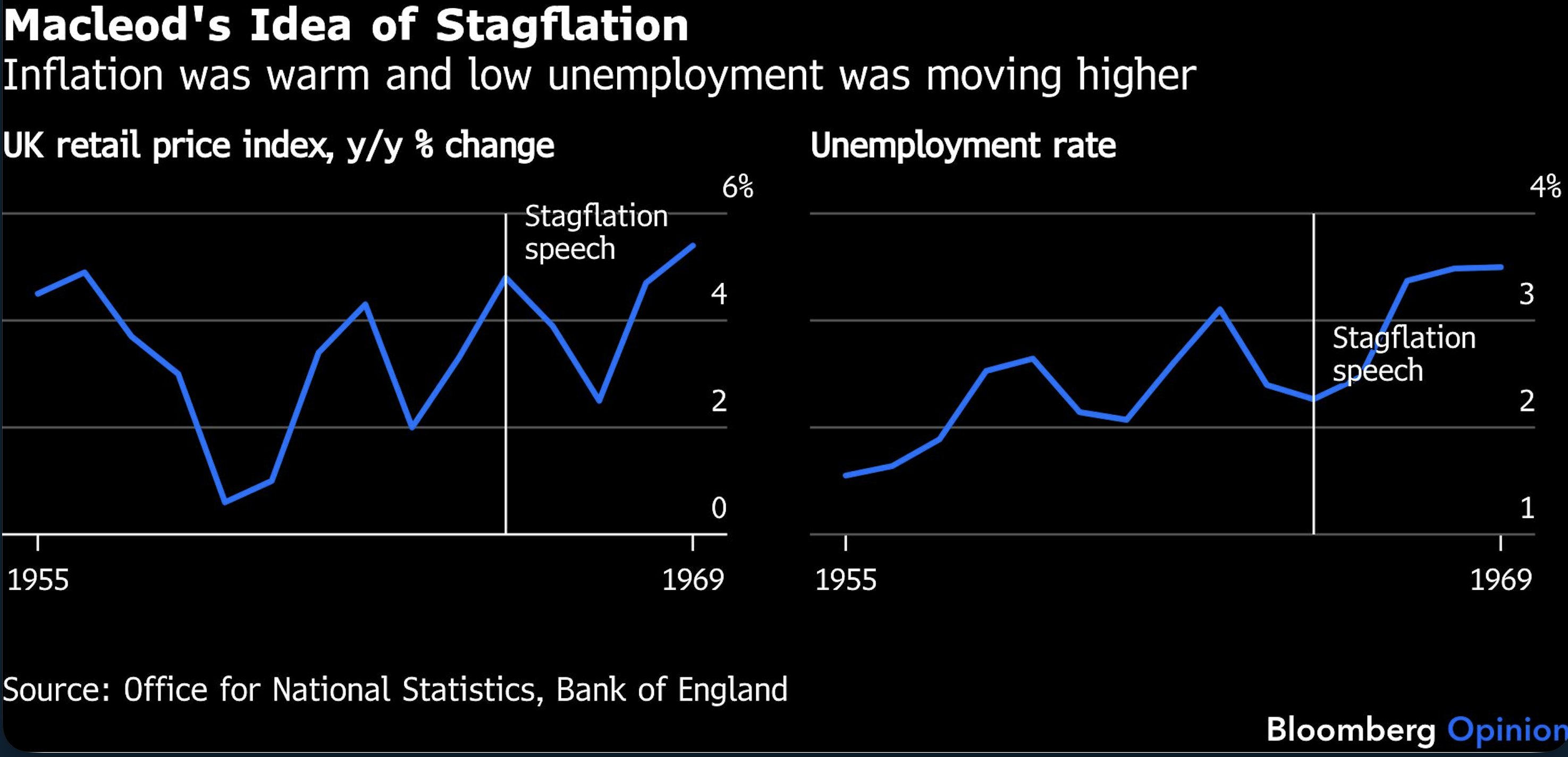

But stagflation didn’t always describe such abysmal circumstances. The term seems to have debuted in a 1965 speech on the UK economy by Tory Iain Macleod in the House of Commons. According to the Bank of England, Macleod was speaking at a time when inflation was running at a warmish 4.8%, real gross domestic product was expanding at a middling 2.1% and unemployment was just 2.3%. “We now have the worst of both worlds — not just inflation on the one side or stagnation on the other, but both of them together. We have a sort of “stagflation” situation,” he said.

Macleod, who was in the opposition2, certainly intended the term as an insult, but this was decidedly not the hair-on-fire stagflation that Fed Chair Paul Volcker battled stateside more than a decade later. Actually, it was quite a bit more like what we see today: Inflation was a bit too high for comfort, and growth was slowing. It was more a “slowflation” situation. That’s the best way to think about the economy and asset allocation today — challenging for policymakers and investors, though not insurmountable.

So what actually works in slowflation environments? Instead of histrionic comparisons to the disco era, consider more recent periods of US history that, like the UK in 1965, actually bear some resemblance to the current moment.

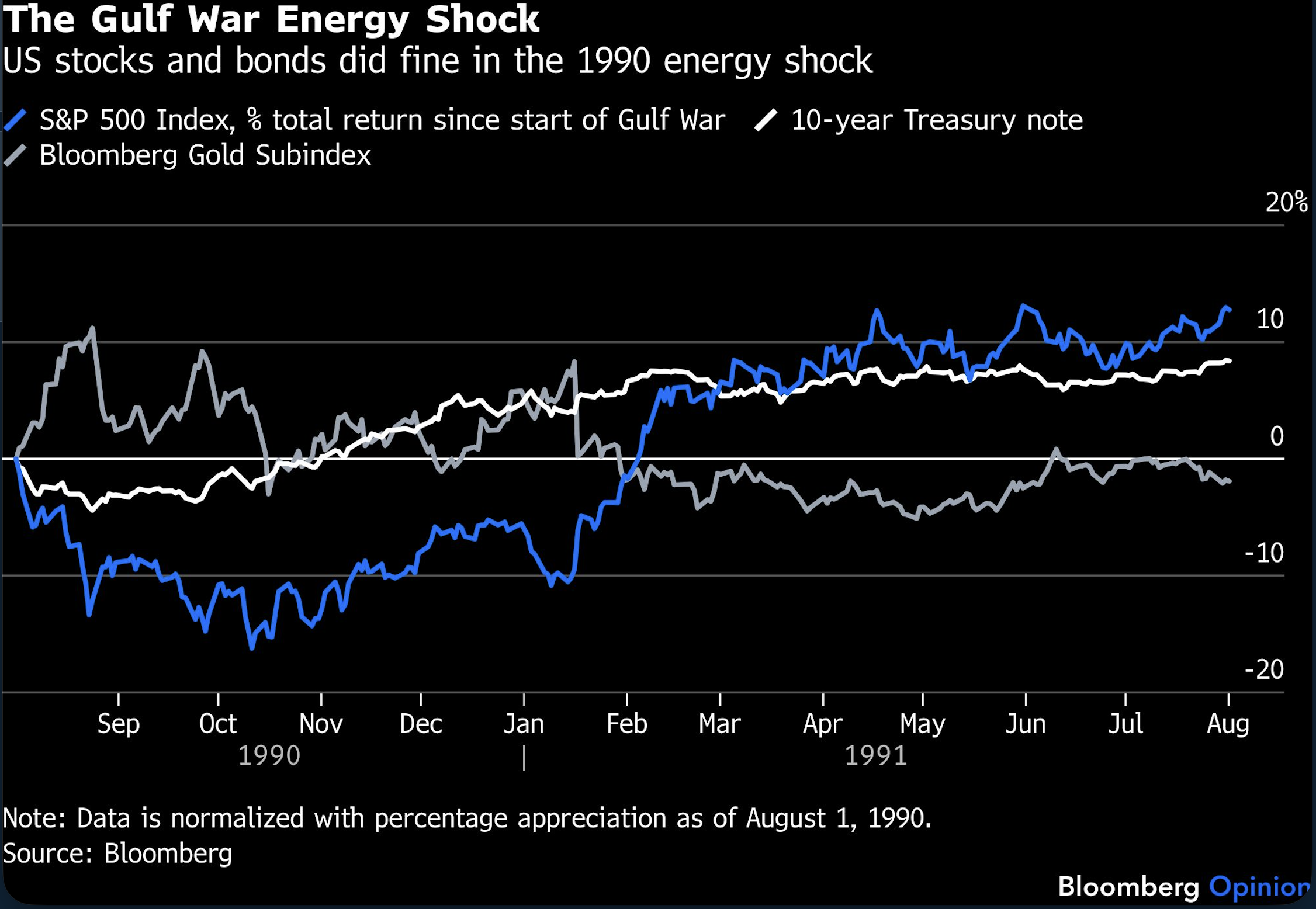

1990-1991: The Gulf War

Iraq’s August 1990 invasion of Kuwait briefly sent Brent prices up around 150% (compared with about 50% today), pushing headline inflation to 5.2%, as measured by the personal consumption expenditures deflator. Although the US ultimately dipped into recession in the second half of that year, it was short and shallow by the standards of the 1970s.

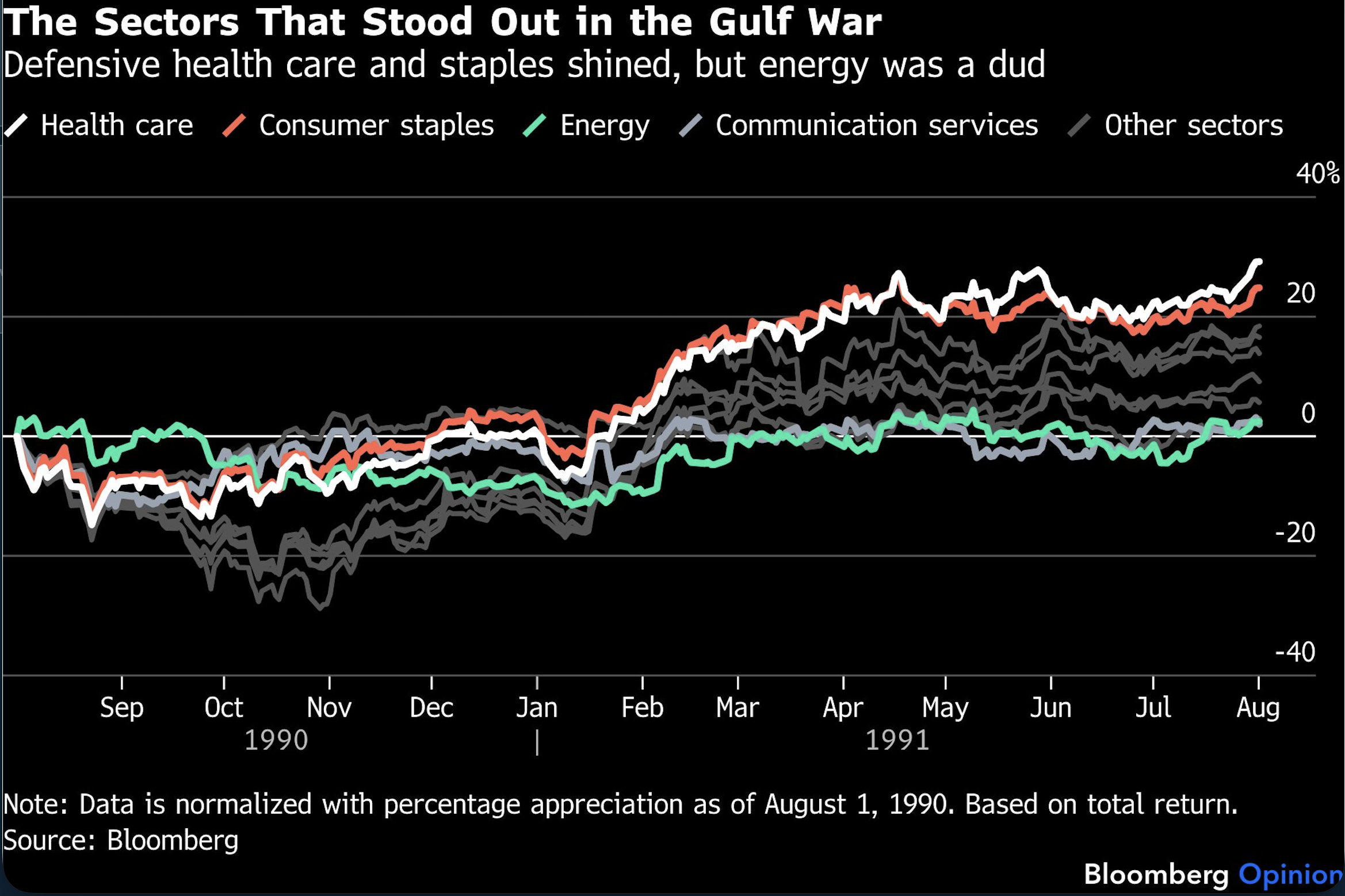

It was a volatile period for stocks but not a terrible one. If you count from the day the conflict started on Aug. 2, 1990, the S&P 500 Index saw a maximum short-run drawdown of about 17%3, with the index bottoming that October. By February, it had made up all its lost ground and, a year after the conflict began, it had returned almost 13%. And gold? The Bloomberg Gold Subindex retreated over the period. Among defensive plays, the precious metal was crushed by 10-year Treasuries. So much for the idea that stagflation (or slowflation, in this case) is bad for nominal bonds with duration.

Granted, it paid off (slightly) to build defensive tilts into equity portfolios: The best-performing sectors in the year after the outbreak of war were health care and consumer staples. Cyclical areas held their own, too. The surprising disappointment was energy. By the time the war actually started, energy stocks were already peaking, and the inevitable supply response led the sector to tread water for the next year, making it one of the biggest underperformers.

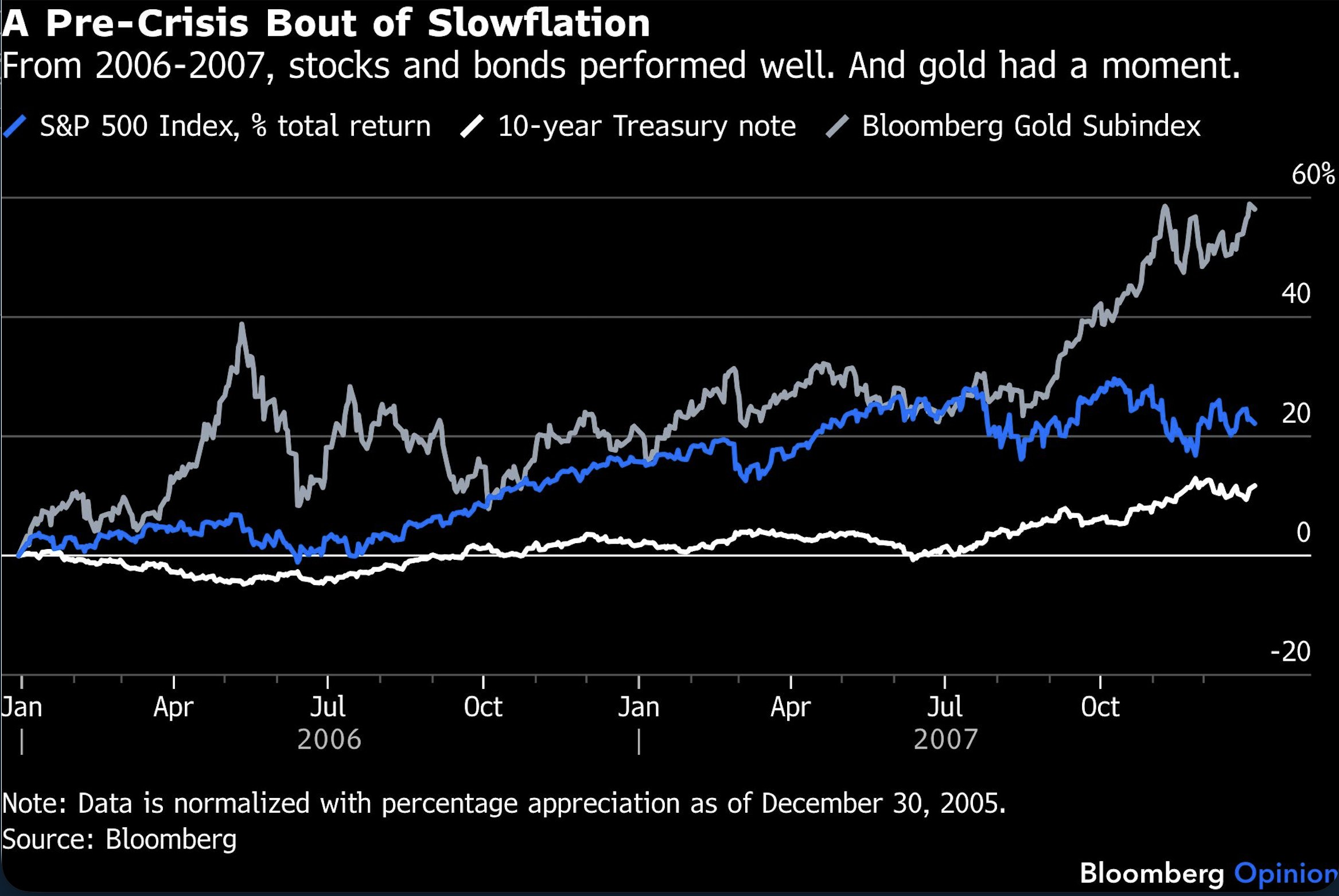

2006-2007: The Calm Before the Financial Crisis

The years prior to the financial crisis offer another example. A steady drumbeat of geopolitical developments had contributed to an insidious uptick in energy prices. Among other things, Israel fought a 34-day war with Hezbollah in Lebanon, and Iran’s nuclear program was being viewed with mounting concern on commodities’ trading desks.

But unlike the Gulf War period, no single major “shock” defined the price action. Rather, the period was marked by durably strong energy demand from China and other emerging markets against the backdrop of the ongoing Iraq War. Brent cost about 49% more on average in the 2006-2007 period than in the prior two years. Headline PCE inflation averaged a too-warm-for-comfort 2.7%, yet economic growth was decelerating and unemployment inching higher.

Still, it was a perfectly reasonable time to stay invested in large-cap US equities (notwithstanding the implosion that would unfold in 2008.) In the two calendar years, the S&P 500 delivered almost 11% annualized returns, and 10-year Treasury notes did fine. The Bloomberg Gold Subindex performed very well, but you had to time the trade perfectly: Most of the gains were realized in the back half of 2007.

The best performers were energy and communication services stocks, and financials did the worst.

But there was no obvious benefit to trying to get cute with equity portfolios — no common asset-allocation lesson that united this period with 1990, aside from the realization that staying invested and diversified is usually a good idea.

All told, it’s hard to be wildly enthusiastic about economies like this. In addition to Friday’s uninspiring GDP update, investors learned last week that inflation-adjusted consumer spending increased just 0.1% in January from the prior month. And on a year-over-year basis, PCE inflation stood at a too-high 2.8%, even before the energy shock.

Times like these might reasonably fall under the broad rubric of “stagflation,” at least as Macleod originally meant the term, but it’s important to distinguish them from the much more dire disco days. It’s absurd to conclude that rising oil prices necessitate shifting portfolios into gold bars and energy shares, just because that worked once — a period that should be remembered as the most extreme of all episodes. Slowflation markets require something much closer to “normal” asset allocation. A historical aberration is a poor model for the “meh” economy of today.

1. This is based on the personal consumption expenditures deflator.

2. It's worth remembering that the term "stagflation" comes to us from politics rather academic economics. A lot of the people that use it are exaggerating on purpose.

3. This is in price terms. On a total return basis, the maximum loss at any period was about 16%.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.