he US economy looks amazingly resilient on the surface. Notwithstanding the two-month Covid-19 recession of 2020, the US hasn’t experienced a downturn since the end of the financial crisis in the middle of 2009. Recently, the streak has elicited a wave of commentary, with smart analysts drawing different conclusions about what it all means for markets. My two cents? Even if the nature and frequency of recessions is changing a bit, it’s dangerous to assume that’s made equity investing any less risky.

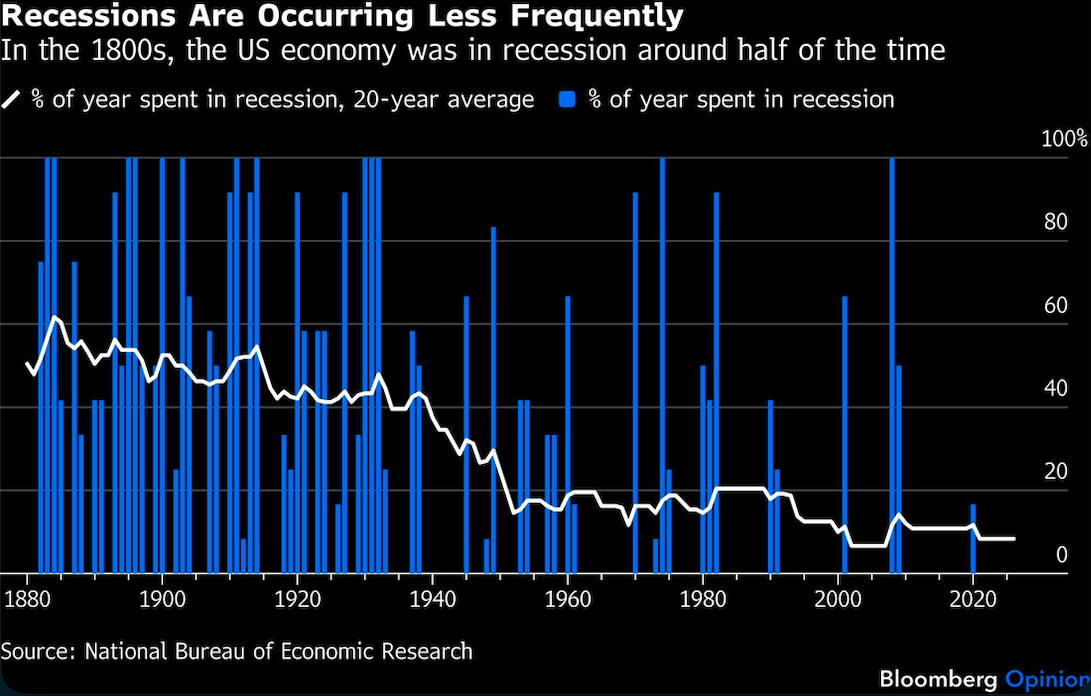

The empirical evidence itself is hard to argue with. Looked at through rolling 20-year windows, the US economy spends very little time in recession these days1, whereas it used to be in downturns around 50% of the time in the late 19th and early 20th centuries.

The first big drop-off occurred from the 1930s to the 1950s. We can logically link this to innovations including deposit and unemployment insurance, and the growing power and sophistication of the Federal Reserve. The frequency of recessions declined again from the 1980s to the early 2000s, potentially tied to further improvements in central bank credibility, including the 1951 Treasury-Fed accord and the 1977 creation of the “dual mandate.” (It was then that Congress formally charged the Fed with promoting “maximum employment” and “stable prices.”)

Since then, it’s less clear from the data whether the frequency of recessions has really continued to drop, suggesting that the newfound enthusiasm to relegate recessions to the past might not stand up to scrutiny.

The US has spent about 8% of the past two decades in recession. While that’s very low, the same statistic stood at under 7% in the pre-crisis 2000s. In a now infamous 2003 address to the American Economic Association, the University of Chicago’s Robert Lucas declared that the field of macroeconomics had succeeded — mission accomplished, folks! — in curbing the risk of macroeconomic disaster. “Its central problem of depression prevention has been solved, for all practical purposes, and has in fact been solved for many decades,” he said. While the financial crisis that followed several years later wasn’t technically a depression, it was indeed the worst downturn since the 1930s. So are we at risk of making another such mistaken assumption? Maybe.

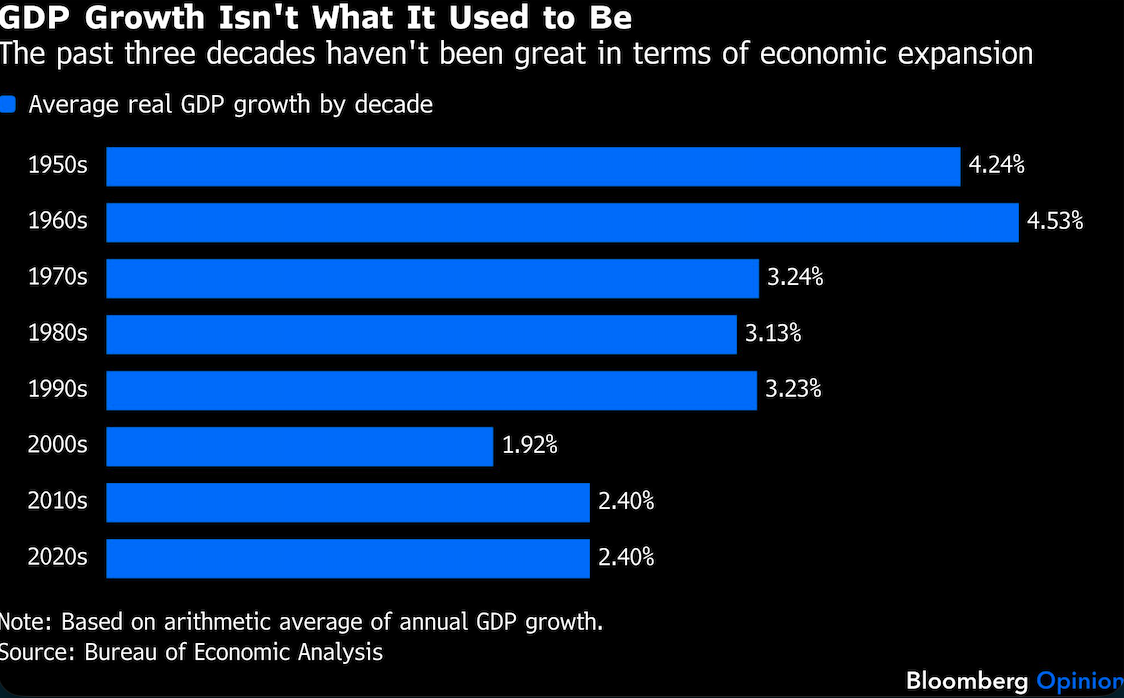

While recessions are less frequent, growth isn’t what it used to be, either. Even without the downturns, the US economy tends to expand at about half the pace it used to on average. To some extent, we’ve traded faster growth for fewer recessions.

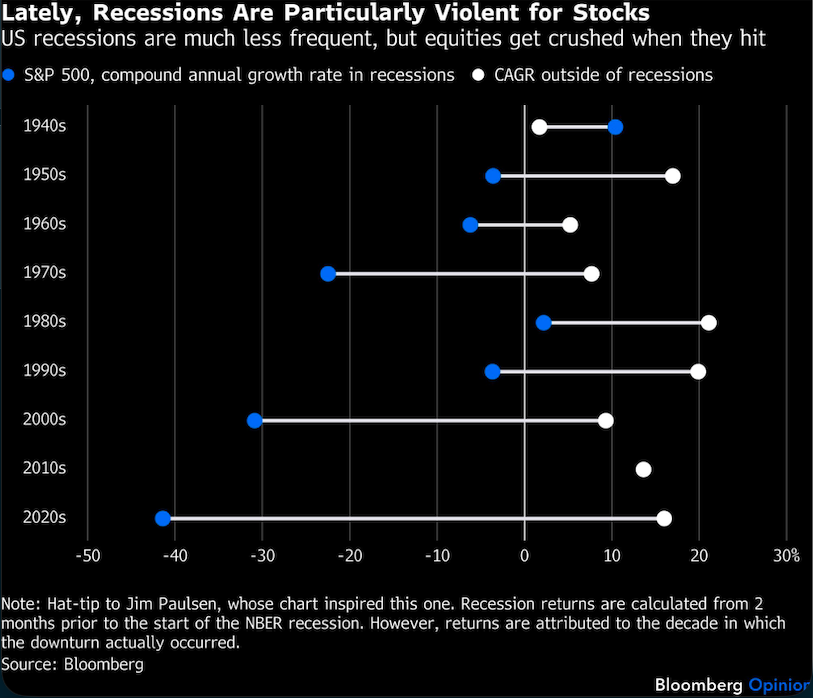

As far as stocks are concerned, the rare recessions are playing out more violently in capital markets. Even if you believe that recession risk is receding, you must acknowledge that those rare events can still be quite brutal — perhaps more so today.

In the graphic below2, I’ve displayed the S&P 500 Index’s state-dependent (recessionary and non-recessionary) compound annual growth rates by decade. What’s striking is that the spread has gotten significantly wider. Yes, returns have been very strong during expansions, but they’ve been very horrible during the infrequent recessions. It’s possible that long expansions — greased by accommodative monetary or fiscal policies — allow systemic risks to build up and valuations to become bloated, leading to a stunning unraveling once the downturn eventually hits.

Over time, it’s hard to conclude that stocks are permanently less risky in this environment. Consider the Sortino ratio, a measure of equity market returns divided by downside deviation, a proxy for risk.3 Historical data show that downside volatility has been broadly similar for decades, despite the declining number of recessions, and there’s been no discernable improvement in the returns for each unit of risk.

Why? For one thing, the market has experienced plenty of severe drawdowns that didn’t correspond to recessions (the 1987 Black Monday crash, the 2022 bear market, the “Liberation Day” equity crash). If policy is indeed cutting down on recessions, those long periods of macroeconomic tranquility are still interspersed with periods during which investor complacency and excessive risk-taking blow up in spectacular fashion.

Certainly, the economy and markets seem to be on a roll right now, but streaks can deceive us, just as they deceived Robert Lucas in 2003. Moreover, the operative question is whether a world of fewer recessions would really change the calculus for investing in the US stock market anyway. My answer is a resounding ‘no’: The balance of evidence suggests that equity market volatility is here to stay, no matter how long we happen to go between downturns. And the next one is always potentially around the corner.

1. If you look at the period since the financial crisis, the US has only been in recession 1% of the time! Then again, it's somewhat unusual to measure trends in rolling 16-year periods. Obviously, the conclusions will change based on the window that you choose.

2. I got the concept for this chart from a Jim Paulsen note in Paulsen Perspectives titled, "With far Fewer Recessions, Why Not Invest More in Stocks?" For an alternative take on this issue, I highly recommend Jim's piece and its companion, "Addendum to U.S. Recession Frequency."

3. Conventionally, many people measure risk adjusted returns using the Sharpe ratio, which divides excess returns by the standard deviation. The Sharpe ratio is hit by both upside and downside volatility. For these purposes, I prefer the Sortino ratio, which only penalizes "bad" volatility.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.