The oil market, like nature, abhors a vacuum. It’s got one anyway, and a big one at that.

Roughly 15 million barrels a day of oil supply, 15% of global demand, are bottled up in the Strait of Hormuz. You can also think about that number as the total amount of oil that’s been drawn from global stockpiles to bridge the disruption: Roughly 500 million barrels so far, estimates Goldman Sachs Group Inc. At the current pace, that could hit a billion barrels by June, maybe even Memorial Day.

As Bob McNally, who heads consultancy Rapidan Energy Group, said this week at a conference hosted by Columbia University’s Center on Global Energy Policy, these missing barrels are like a vacuum; a giant deficit that will move through the global oil system for some time, even if a peace deal opens the Strait.

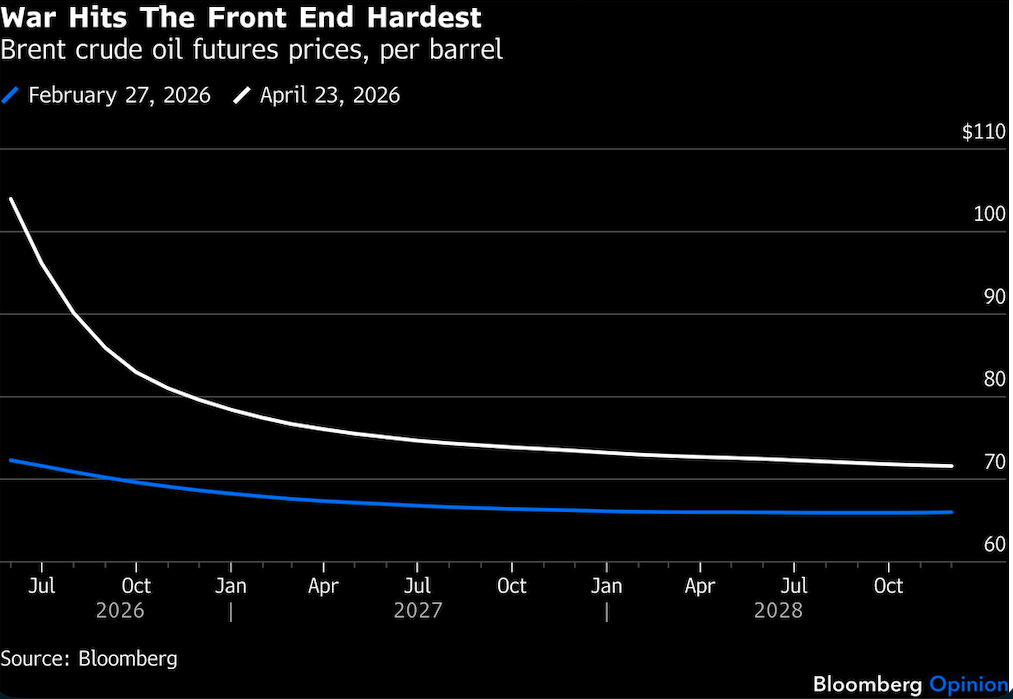

Brent crude oil futures are back above $100 a barrel but, relative to the scale of the disruption, the market seems strangely sanguine, especially in longer-dated futures, from which oil producers take their cues on drilling. Prices for 2027 are up 17% compared with 43% for front-month contracts. On that, Kaes Van’t Hof, chief executive of Diamondback Energy Inc., one of the larger shale operators, said from the same stage as McNally: “The back end of the curve is lying to us.”

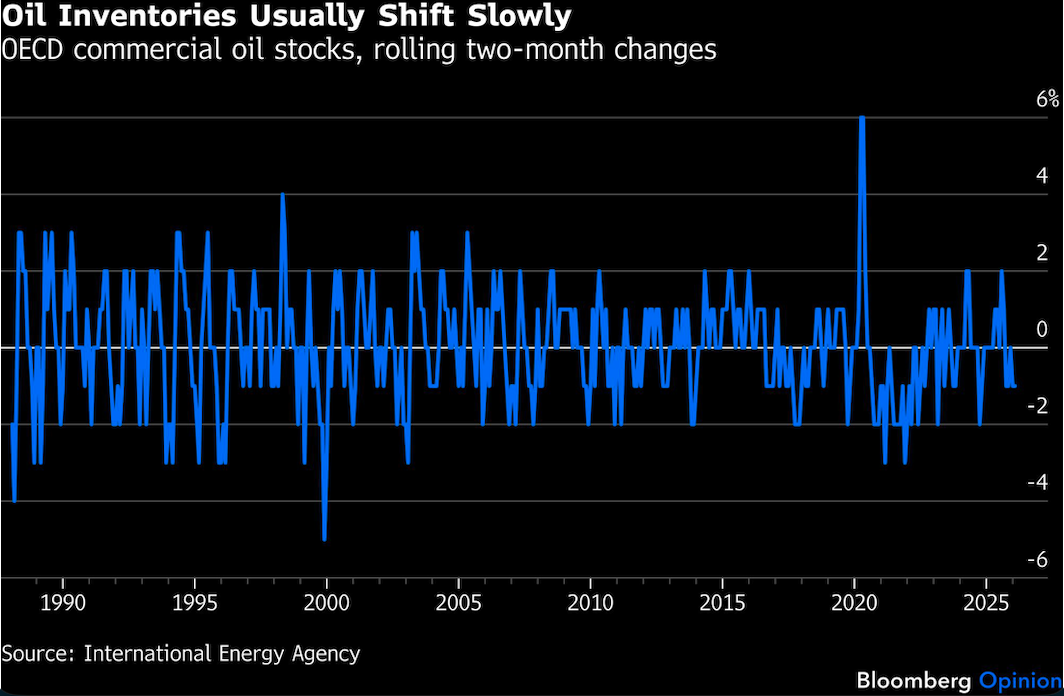

This is the biggest disruption of the oil market since another one fed by hubristic expectations of a quick victory in the Middle East: the Suez Crisis in 1956. The roughly 500 million barrels drawn over the past two months are equivalent to about 6% of global observed inventories (these are estimates since not all oil stocks are reported). To put that in perspective, consider the history of movements in OECD inventories, the most transparent subset of global stocks, where 6% would already represent the sharpest two-month decline in data going back to 1988. By June, we could be looking at more like a 10-12% drop in global inventories, way beyond the scope of prior declines.

Tapping inventories is the physical manifestation of a tight oil market, where supply isn’t covering demand, and futures prices should rise concomitantly. They have sold off since their peak in early April, however, even as stocks have kept falling with the Strait effectively closed. Intuitively, this suggests a certain optimism that the current ceasefire will resolve into a durable peace, and an open waterway for tankers, relatively soon.

Technical factors have also played a prominent role, argues Ilia Bouchouev, former head of derivatives trading at Koch Global Partners, in a recent paper for the Oxford Institute of Energy Studies. He observes that hedge funds, who entered the year without much exposure to oil, piled into the front end of the curve when hostilities broke out, initially exacerbating the surge in near-term futures prices. The spread between the 1st and 6th month contracts surged from about $2 a barrel in late February to about $35 by early April. However, the volatility induced by a number of factors — not least the release of strategic stocks and the whiplash updates delivered from a certain Truth Social account — forced many to then sell to manage risk, or simply take profits. This “shock absorber” effect may not last, he warns, particularly if things re-escalate in the Persian Gulf.

Even if conditions stay just as they are, the rapid drop in inventories, unless arrested, will trigger another bout of buying. In the most optimistic scenario, where Hormuz opens immediately, it would still take months to first clear the backlog of blocked tankers, then clear local oil in storage and finally bring shut-in wells back into production — all while clearing mines laid by Iran, something that could take months to do. While the pace of inventory draws would ease, they would still be running down the tanks.

And we remain far from the optimistic scenario with Iran, Israel and the US trading threats, and two blockades in place. US oil executives canvassed by the Federal Reserve Bank of Dallas in an unusual interim survey released Thursday concur. Four-fifths of them don’t expect traffic through the Strait to resume normal levels before August; 40% think it will be November or later. In addition, a majority implicitly concur with Van’t Hof’s comment about the lack of an adequate price signal to boost output, expecting relatively little growth in US oil production this year and next.

The bigger the vacuum becomes, the longer it will take to refill those inventories whenever whatever passes for normality finally arrives. Oil prices along the curve would need to rise accordingly to encourage excess production — or, conversely, achieve the same outcome by destroying demand.

We cannot know the exact threshold that might trigger another round of panic buying in the futures market: A billion barrels gone? Two billion? Looking back to a different kind of disruption, the outbreak of Covid-19, ClearView Energy Partners notes how the oil market still hadn’t internalized that looming catastrophe as late as February 2020, weeks before the Nymex price went negative as demand cratered. Realization didn’t so much dawn as go supernova. Almost exactly six years on from that day, the gap between physical flows and financial markets looks as wide as the Strait is narrow, and widens by the day.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.