What do the Federal Reserve and the US oil industry have in common? In today’s war-torn market, both are the supplier of last resort. One provides dollars; the other barrels. But that’s where the similarities end. The central bank can print the currency at ease; the drillers cannot.

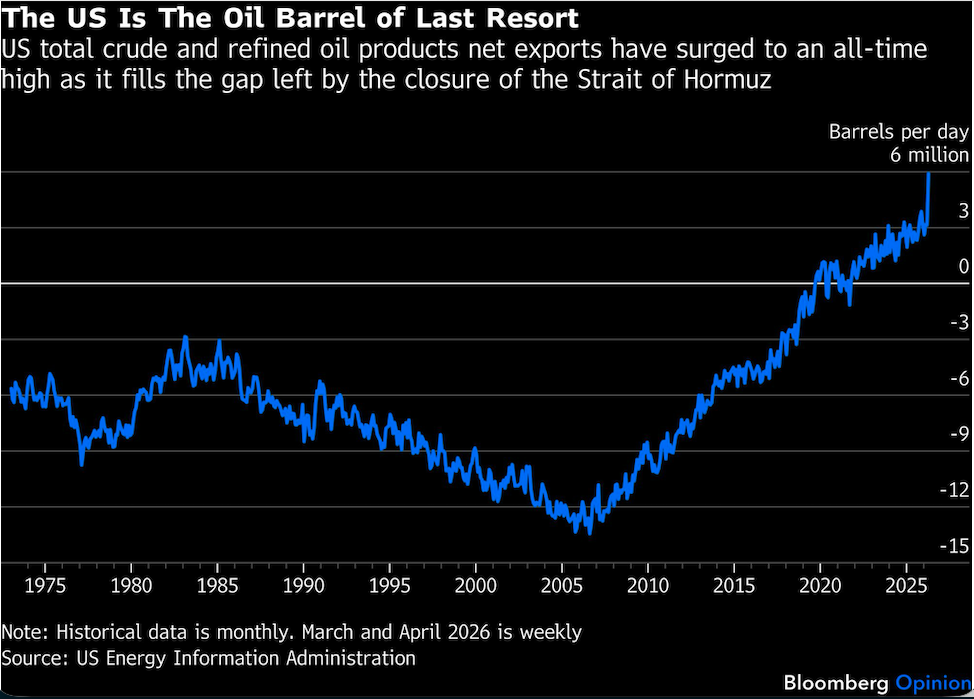

Facing an unprecedented shortage, the global oil market has called on the US, the world’s top producer, for help. And thanks to the shale revolution, America has been able to respond: Over the last four weeks, US net exports of crude and refined products have averaged a record high of 5.9 million barrels a day, up from 3.3 million a year ago. Only a decade ago, the US was a net importer in excess of 5 million.

Can the US sustain that level of net exports forever? No — the American shale revolution is extraordinary, but not miraculous. The question, however, isn’t whether the nation can keep up with no end in sight; instead, it’s whether it can do it for long enough to keep oil prices from exploding before it reaches a deal with Iran. Looked through that lens, the US has the ammunition, thanks to its emergency stockpile, to sustain its outsized oil exports for several more weeks, perhaps even a couple of months.

The export boom is a key reason why oil prices have tumbled, particularly in the physical market (the portion of the market where real barrels, not swaps or futures, change hands). The collapse in Chinese oil imports has also helped, as have other well-known levers, like the use of bypass pipelines around the Strait of Hormuz.

The US, with its 2.6-million-barrel net export hike, is the biggest driver in an overall surge from the American continent. Others are contributing, too, and when combined, their extra exports do add quite a bit: Canada (400,000 barrels per day); Venezuela, Guyana, Colombia and Argentina (200,000 each); and Brazil (100,000). Together, the Americas are exporting, on a net basis, almost 4 million barrels a day more than they did around this time in 2025. That equates to one-quarter of the shortfall created by the closure of Hormuz.

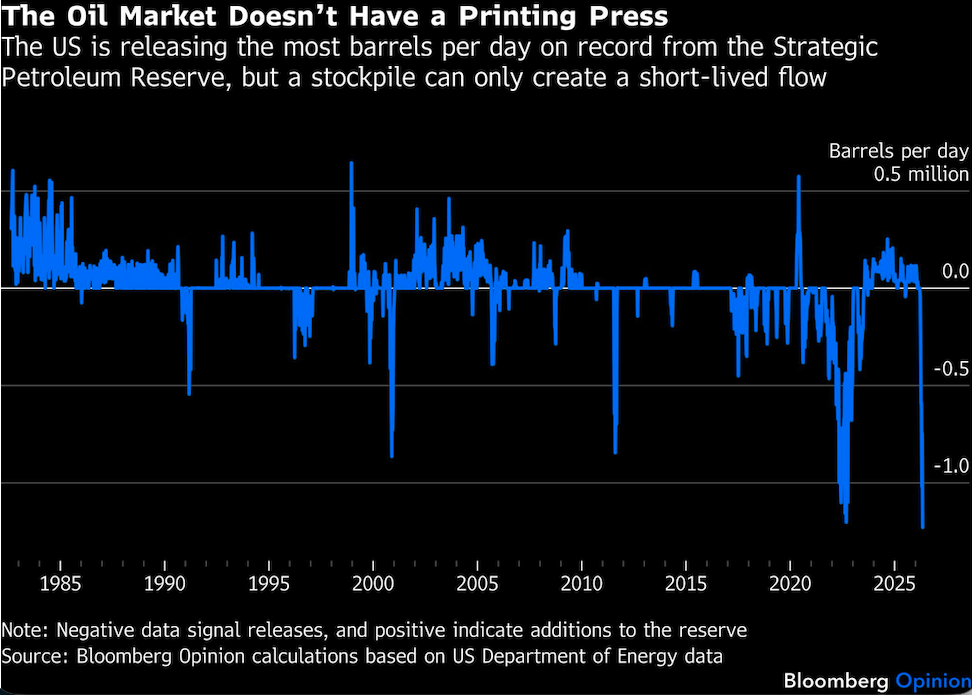

For the US, the key is the willingness of President Donald Trump to squeeze the country’s Strategic Petroleum Reserve (SPR) as never before — harder than President Joe Biden did in 2022 after Russia invaded Ukraine. In March, Washington agreed to loan 172 million barrels from the SPR as part of a coordinated release of the emergency stockpiles with other industrialized nations.

The market knew the barrels were coming but wasn’t sure about the speed of the flow. Initially, it was a trickle; now, it’s a gusher. Last week, the US put into the market more than 1.23 million barrels a day from the SPR, the highest weekly volume ever — and well above naysayers’ predictions that the emergency stockpile wouldn’t be able to do anything near 1 million, let alone more.

With super-high flow rates, the US is offsetting half its net increase in exports via the use of the SPR. Washington is also letting the emergency supply reach the global market. SPR barrels are already heading to the Netherlands, Italy and Turkey.

The American oil gusher has crushed the physical oil market. West Texas Intermediate (WTI), the US oil benchmark, at one point traded at a record-high premium of $22.80 a barrel above Dated Brent, the North Sea physical oil market benchmark. Now, it trades at just $1.50 higher. Put it all together, and the drop in real-world prices is extraordinary. One month ago, the total cost of a barrel of WTI landing in Europe, including not only the benchmark, but also freight and the physical premiums top-up buyers pay above the benchmark, was nearly $160 a barrel; now, it’s $106.

Through last week, the SPR has released about 31 million barrels since Trump tapped it. Assuming the release rate of about 1.2 million barrels a day continues until the final drop, Washington has another 117 days — or the beginning of September. At much higher rates, say, 2 million barrels a day, the 172 million barrels earmarked by the reserve would still last until late July.

Sure, Trump could order further releases, but that will push an already weakened SPR to its limit. After the full loan is released, the reserve would be left with 242 million barrels, the lowest since the early 1980s. Perhaps the president can order an heroic final release. But I fear it would only trigger panic. Would Texas, New Mexico and other oil states come to the rescue? Probably not. US shale drillers will certainly increase output, first by tapping their reserve of so-called drilled-but-uncompleted wells, which can be fracked quickly into production. But they are unlikely to make a big difference until the final months of the year.

So to keep up with exports, the US will need to tap not just the strategic reserve but also the day-to-day commercial stocks that private companies hold. It’s relatively well positioned to do so: At the starting point of the export surge, the country’s commercial crude inventory was above the five-year average level and just slightly below the 10-year average.

On balance, Trump probably has the rest of May and probably into June before the combination of the shrinking SPR and growing pressure on the commercial inventory start to stir up market anxiety. That’s probably enough time for the White House find an exit to its quagmire in Iran. Still, the clock is ticking: America is sustaining an enormous flow of oil using a stockpile. And unlike the printing presses of the Fed, it can’t just be topped up with a fresh sheaf of paper.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.