“So long, honey babe, where I am bound, I can’t tell.”

Bob Dylan, “Don’t Think Twice, It’s All Right.”

Ignoring threatening clouds in the distant horizon, the financial markets are wrapped in a blanket of complacency. Consider the following. The Dow Jones Index has been flirting with the 2007 record peak. Implied stock market volatility, as measured by the VIX Index, is in the basement. Junk bond yields are at record lows, compressing spreads to within shouting distance of risk-free Treasuries. Securitization is back from the dead, while the drought in M&A activity is now getting plenty of rainfall.

Investor euphoria is not confined to the US. In Japan, the Nikkei 225 Index has surged, climbing to a four-year high. The advance has reawakened the enthusiasm of domestic retail investors, who for the last twenty years had come to believe that stocks only go down. Copies of the KaishaShikiho, the so-called bible of Japanese equities, are flying off the shelves.

In Europe, with the sovereign debt and bank crises in remission, thanks to unprecedented support by the European Central Bank, equity markets, as measured by the S&P European 100 Index, have climbed the proverbial “wall of worry” and now are a stone’s throw away from the 2007 peak, while the euro has regained a “safe haven” luster. Similarly, prices of emerging market debt denominated both in hard and local currency are at near-record highs, shrinking the yield spread over US Treasuries to near-record lows as investors seem willing to trade interest rate risk for credit risk.

Underpinning the turn in investor sentiment is the sense that prospects for the global economy are brightening as some of the headwinds that buffeted growth have started to diminish. In the US, pulling back from the “fiscal cliff” has postponed the date of a broadside shock to the economy brought on by drastic government spending cuts. Meanwhile, the private sector, mostly households, is likely to provide greater support on the back of pent-up demand fueled by ongoing job gains, higher consumer confidence, a lighter debt service burden, an improving housing market, and a significant repair of household net worth.

Overseas, a spate of government programs by the new Japanese government, including hefty infrastructure spending and aggressive easing by the central bank, is aimed to shake the economy out of its 20-year lethargy. In the euro zone, the push for fiscal consolidation appears to have dissipated, holding out the promise that the recession underway is likely to give way to modest growth in late 2013 or early 2014. Meanwhile, concerns over China’s hard landing have diminished with the economy ending 2012 on a strong note, spurred by increased manufacturing activity, expanded spending in infrastructure and a pickup in credit growth.

Curves Ahead

Following a “Lost Decade,” the renewed love fest with equities is exciting. At the very least, it implies that investors have not lost faith in the ability of market-based capitalism to create wealth. We are, however, skeptical whether the latest rally has long legs. Much of the perceived improvement in the global economy is fragile and the progress could easily slide off the road. The margin for policy mistakes is tight.

In the US, the threat of sequestration and the debacle of debt ceiling still loom large, as politicians on both sides of the aisle appear to have dug in their heels. Despite significant deleveraging (much of it involuntary as a result of foreclosures and credit write-offs,) the restructuring of household balance sheets has a long ways to go before consumers could step up their spending.

On the business front, while nonfinancial corporate balance sheets appear robust, much of the stash of cash is concentrated (primarily with tech companies) and a large portion of it resides outside the US. Any serious boost to domestic investment spending by deploying the cash reserves is questionable. Also, concerns over a possible rise in debt defaults is yet another hurdle to a pick up in business spending. To be sure, default rates on corporate debt have remained very low – an unusual trend so late in the recovery – even though corporate leverage has climbed back to the high levels of 2006-07 as companies took advantage of cheap credit to refinance more expensive debt. Yet, if growth in revenue and cash flow continues anemic, as we expect, highly levered companies will find it increasingly difficult to roll over maturities, prompting a rise in default rates and a loss of investor appetite for high-yield debt.

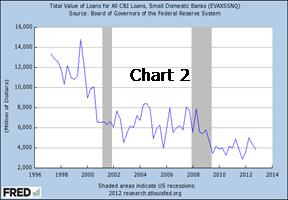

Meanwhile, despite overall improvement in the health of banks, shown by the steep decline in the financial stress index (Chart 1) and record holdings of reserves with the Fed, lending to business continues relatively weak, especially by small banks (Chart 2), whose activity is more representative of the underlying strength of the economy. And absent a strong rebound in bank lending (not highly likely in the face of tighter regulation and lower leverage) the economy will be deprived of high-octane fuel, keeping the pace slow.

Chart 1Chart 2

The picture abroad looks less reassuring as well. The palliative influence of unlimited QE by the European Central Bank has sent the financial crisis into remission, but the knock-on effects of the debt contagion have not been contained, seriously undermining longer-term prospects for growth in the euro zone. In our view, France is likely to show no growth, while Italy, Spain and Holland are expected to contract further this year. Beyond the cyclical factors at hand lie serious structural deficiencies that could be addressed only over a longer time frame. These, too, are likely to restrain growth in the period ahead.

We also doubt whether Prime Minister Shinzo Abe will be able to walk the talk. The G-20 countries have just agreed not to put pressure on Japan to relent in its efforts to weaken the yen in order to gain a competitive advantage. But, trying to boost exports on the back of a weaker currency is not the answer. Japanese companies have shown great ability to adapt to a stronger yen; it provides for cheaper imports, among other things. The real problem is uncompetitive products as shown by the mounting troubles of industry leaders, especially in the electronics and hi-tech sectors, which have been the cutting edge of Japanese exports.

In all, Mr. Abe’s program to re-energize Japan’s economy comes with serious risks. A yen overshooting on the downside, coupled with massive new supplies of government bonds, might trigger a rise in government bond yields, generating capital losses and sapping the willingness of Japanese investors to load up on government debt. In that event, Japanese equities will not be able to avoid a sell-off.

Then, too, China’s ability to engineer a soft landing beyond the near term is questionable. The new government’s efforts to step up infrastructure spending are doable with the turning of the credit spigot. But this is likely to lead to significant further deterioration of bank balance sheets, which are replete with nonperforming loans. And in the face of tepid global growth and weakened export markets, excess capacity in manufacturing is likely to grow, further undermining business investment.

Danger:Falling Rocks

Danger:Falling Rocks

The newly found optimism for equities is puzzling. One explanation might be simply the absence of bad news which is encouraging investors to take on more risk. Another might

reflect investor sense that in the wake of the January stock market surge unless they climb aboard now they might miss out when the train leaves the station. It is also possible that at long last investors are convinced that stocks at today’s valuations are true bargains. For whatever reason, the latest flood into equity mutual funds after five years of net outflows has given rise to the notion that the “Great Rotation” out of bonds into stocks is finally at hand.

Not so fast. Filtering out the Street’s noise, there are a few things worth keeping in mind. Metrics of valuation, like the P/E ratio, the earnings yield and even the dividend yield, could be misreading how much stocks are worth in the midst of “financial repression” brought on by the Fed’s ZIRP and QE policies. For the same reasons, the equity risk premium, an often used but hard to define indicator of stock market dearness/cheapness, should not be relied on in deciding whether this is the right time to jump into the market.

We have misgivings regarding the “Great Rotation.” A more granular look suggests that the bulk of the money that flowed into equities came out of money market funds and not out of bond funds. The latter actually received an estimated net inflow of $30 billion according to Investment Company Institute data. In addition, about 40% of the $70 billion of equity inflows actually went into international/global funds. This is an extension of the trend that got underway in 2012 and reflects US investor needs for portfolio diversification. Overall, the appetite for stocks by US retail investors in their retirement accounts continues to wane as shown by their willingness to sell into the bull market. Whether the latest rush into stocks represents a change of heart only time will tell.

Nor are trends on the institutional front indicative of a newly found love for US equities. Private pension funds had reduced equity market exposure to 34% of total financial assets as of 3Q2012, down from 42% in 2007, according to FRB data. A similar, but less pronounced decline, has taken place in state & local retirement funds (62.2% in 3Q2012 vs. 63% in 2007) as they are tilting their portfolios increasingly toward alternative asset classes in search for higher yield.

On a similar note, non-US investors have yet to show increased appetite for US equities. Despite a better performing US economy, their holdings had declined as a portion of total US credit market instruments to 36.8% as of 3Q2012 (latest available FRB data) from 38.7% in 2007, while doubling their investments in US Treasuries to 16.2% from 8.8% during this period.

It is too early to declare, as Street pundits are doing, that the cult of equities has returned on the back of the latest large flows into stock mutual funds. And we question whether market valuations are reliable indicators. Depending on what metrics are used, stocks are either a screaming bargain or seriously overvalued. In this regard, Darrell Huff’s HowtoLiewithStatistics published in 1954 is worth reading.

At the end of the day, analyzing whether US equities are cheap or expensive is an instructive, but provincial exercise. As the last few years have shown, getting the global big picture right is what it’s all about. Until recently, who would have thought that swings in the Spanish bond market would be a driver of US equity prices, as the tight correlation in Chart 3 between the yield on the 10-year Spanish government bond and the S&P Index clearly shows?

Chart 3

Looking at what lies ahead, our best guess is that against the backdrop of anemic global growth equity markets will generate feeble returns. There is still a thick layer of policy uncertainty overhanging the markets that investors will have to navigate. In the road ahead, keeping an eye out for falling rocks, especially in the euro zone, would make the journey a lot safer.

724 FIFTH AVENUE, 9TH FL

NEW YORK, NY 10019

TEL: 212-598-5757

63 FORESIDE COMMON DRIVE

FALMOUTH, ME 04105

TEL: 207-781-5005

Disclaimer:This report was prepared by Dimitri Balatsos of Tesseract Partners and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security or investment products.

© Tesseract Partners