Credit Availability Underpins Recovery in Commercial Real Estate Prices, But Also Poses Risks to CMB

- Credit availability, low interest rates, limited new construction and improving economic conditions have contributed to the recovery in commercial real estate (CRE) prices.

- We expect a strong 2014 in the commercial mortgage-backed securities (CMBS) market, which has been a primary source of CRE credit expansion.

- Increasingly aggressive loan underwriting is a concern. CMBS investors need to speak with their wallets and push back on either valuations or underwriting standards if recent trends continue.

The U.S. commercial real estate (CRE) sector is regaining strength in the post-crisis environment. CRE prices increased in 2013, with the Moody’s Commercial Property Price Indices (CPPI) national all-property composite index rising 16.3% in the 12 months ending in December (most recent data). At this point, PIMCO believes the CRE market has reached the middle to late innings of a recovery, with prices just 8% below their November 2007 peak. Importantly, the recovery remains notably bifurcated, with select multifamily and office property prices well above their late 2007 and early 2008 peaks, while many industrial, office and retail properties outside of major cities remain 20%–40% below their pre-crisis highs.

In addition to origination volumes increasing, lending standards have loosened, allowing credit to flow more freely to properties outside of top tier cities (e.g., New York, San Francisco). While the increase in interest rates in the latter half of 2013 put a brief pause on commercial lending volumes, the expansion in CMBS credit availability largely offset interest rate volatility. Several developments in the CMBS lending environment in 2013 reflected continued growth in origination activity:

-

Increasing competition among lenders. The number of commercial mortgage lenders originating loans for CMBS has practically doubled over the last two years, resulting in greater competition and increased capacity, and also setting the stage for continued growth over the near term.

-

Robust investor demand for CMBS debt. As activist Federal Reserve monetary policies have pushed investors further out on the risk spectrum in search of yield, demand for commercial mortgage debt remains quite strong. And demand is strong across the capital structure, as many hedge funds and real estate investment trusts (REITs) with high-single-digit return targets have been investing in mezzanine CRE debt.

- Continued expansion of the “credit box.” The combination of greater competition among lenders and robust demand for CRE debt income is contributing to a continued easing of credit standards (i.e., expanding the so-called credit box) in commercial mortgage lending.

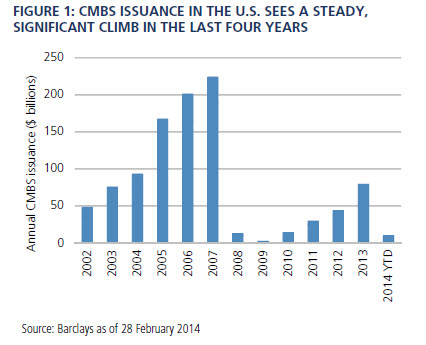

Against this backdrop, the stage has been set for a strong 2014 in the CMBS market, despite the abundance of upcoming maturities on legacy CRE loans that will need to be refinanced. Several years ago, many market participants were concerned that this “wall of upcoming maturities” would pose material risks to CMBS investors, but robust issuance and credit expansion in recent years have resulted in a CMBS market much better positioned to provide capital: PIMCO expects 2014 CMBS issuance in the range of $60 billion – $80 billion, which should provide ample financing for the $56 billion in maturing loans this year.

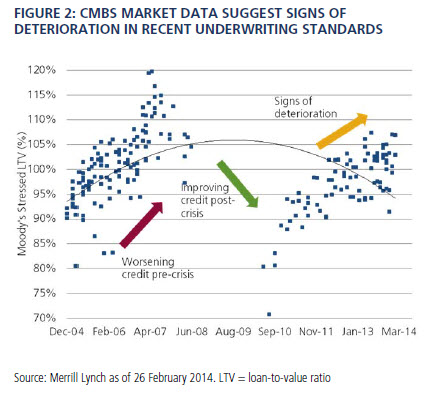

While newly issued CMBS LTVs remain below the pre-crisis peaks of ~120%, recent trends clearly point to gradual increases in LTV, as well as other disturbing developments that are emerging from below the surface – including the ratios of interest-only loans and additional debt. Rating agencies that analyze CMBS debt attempt to “normalize” for these trends using their own LTV assessments based on internal adjustments, models and forecasts. These rating agency views can vary greatly from an underwriter’s typically optimistic outlook, and even among each other.

All investments contain risk and may lose value. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice.

This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world.

© 2014, PIMCO.

© PIMCO