The FIFA World Cup (for soccer aka football) is in full swing. There are 32 teams from around the world treating a world-wide audience of nearly 2 billion to a great show of sport. The teams are competing for $576 million in prize money. The host country Brazil is spending over $14 billion on infrastructure and has an opportunity to learn from this experience as they look forward to hosting the 2016 Summer Olympics. Like their predecessor host country in 2010, South Africa, they are excited to highlight their country’s progress on a world stage. The Federation Internationale de Football Association (FIFA) has received billions of media sponsorship dollars including television, radio and internet. And while the U.S. will not likely make it to the final match, the tournament does offer some insight into diverse economies around the globe and why we should consider international investments as a pillar in any portfolio.

Diversify

Our clients have both international stock and bond investments while some also invest in global real estate and commodities. It is easy to dismiss investments outside of the U.S. because we are the largest economy in the world. However, to dismiss international investments suggests that we don’t want exposure to other interest rate and currency environments, global companies domiciled outside the U.S., and small growth companies around the world. Investors in the U.S. tend to have a “home-country†bias which is to say that we generally don’t invest globally as much as our foreign counterparts do. Why should we, our markets are some of the largest, most liquid and heavily regulated in the world so they provide ample opportunity right? There are many U.S. companies that manufacture and sell their products and services overseas. By default then, a U.S. stock portfolio that includes large-cap conglomerates like GE and IBM must be the same as investing abroad. Not true. There are many companies overseas that compete with our own U.S. based firms successfully. They also provide opportunities to benefit from accelerating growth in foreign markets and different consumer behaviors that lead to different product successes.

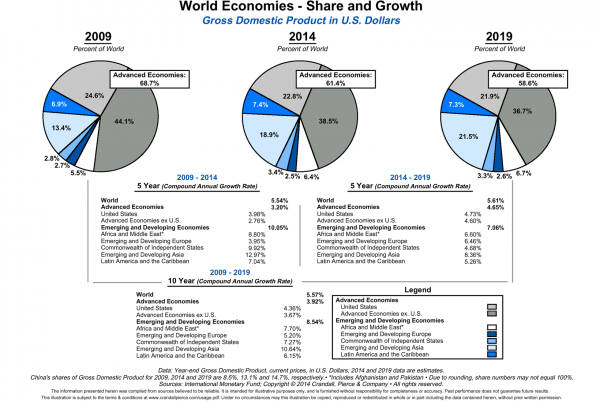

Global GDP

Look at the pie charts below. They represent the allocation of global gross domestic product between the U.S., other advanced economies like Germany, Japan and the U.K. as well as emerging and developing economies like those in Asia and South America. From this chart you can see that the U.S. had 24.6% of the world’s GDP in 2009, approximately 22.8% of it today and is expected to have 21.9% in 2019. At the same time the other developed countries will see their global market share dwindle from 44.1% in 2009 to 36.7% in 2019. When combined, the developed world’s percentage of GDP will decline by 15% over the decade measured. That growth is going to the emerging and developing economies represented among the 32 teams vying for a piece of that prize money in the World Cup. Central and South American teams like Mexico, Columbia, and Brazil; African teams like Nigeria, Ghana; and eastern European teams like Croatia. These countries and their counterparts are expected to grow at a rate just over 7% versus the 4.65% growth rate for developed countries. While there are certainly U.S. firms that will take advantage of this opportunity successfully, there are many companies based outside the U.S. that will do so as well if not better.

World Economies – GDP

Stocks Around the World

It is easy to use the global stock market debacle of 2008 and early 2009 as the only measure of whether stock diversity across the globe makes sense. During that period when the global crisis led to a very high correlation among equity markets there was no benefit from global diversification. However that is the exception to the rule. We don’t have to look any further than the years since the crisis for an example. The U.S. stock market as measured by the Russell 3000 Index is up 22% from April, 2009 while the MSCI All Country World Index ex-U.S. is up only 16% on an annualized basis. The difference in recovery rates represents the diversification effect of differing economies improving at different rates. It also highlights the difference in valuations across global equity markets. The forward price to earnings ratio for the U.S. S&P 500 Index is 17.1 times earnings while for the MSCI ACWI-ex US Index it is just over 13 times, below the pre-crisis level and less than our own market. One of the benefits of global investing is the ability to look at a broader opportunity set and find good companies that are trading at below average valuations due to geo-political concerns. Many investors are surprised to learn that the U.S. only comprises 37.4% of the global stock market capitalization. This is an interesting fact considering that most American investors have less than 20% of their portfolios invested abroad. Using a variety of international and emerging market strategies that emphasize different types of companies can provide a diversified way of investing globally.

What about Bonds

A similar case can be made for investing in global bond markets. The 10-year Treasury currently yields 2.62%, the 10-year German Bund 1.32% and the Japanese 10-year 0.57%. The yield environment in most developed countries is repressed as a result of some sort of central bank interventionist policy that is pushing interest rates lower. These countries governments (our own included) also have very high levels of debt. On the other hand there are countries around the world with less debt to GDP and higher interest rate environments. The Australian 10-year is currently yielding 3.69%. Brazilian dollar bonds yield over 5%. Certainly these economies have problems of their own, however, a good global bond manager is able to identify those problems and determine the impact on yields in that environment and take advantage of markets overreaction to near-term events.

So, enjoy the World Cup. While you are doing so, think about the other two billion people watching and then think about what they are buying and investing in.

Brian K. Andrew

Mr. Andrew is President and Chief Investment Officer at Cleary Gull, Inc., an investment advisory firm in Milwaukee. He leads the firm’s investment research and strategy and chairs the Investment Policy Committee. Mr. Andrew received his B.S. in business and finance from the University of Minnesota and completed the Harvard Business School/CFA Institute Investment Management Program.Â

© Cleary Gull