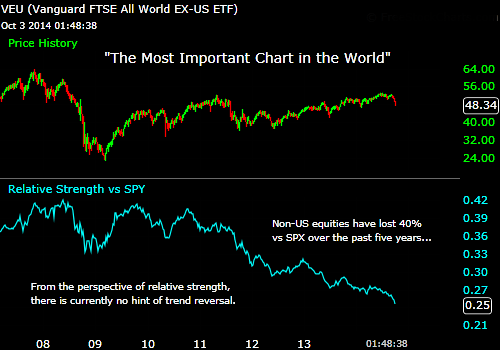

One of today’s most glaring inter-market divergences is the relative performance of US versus non-US equities. For dollar-based investors, non-US stocks have underperformed US stocks by an astounding 40% over the past five years.

The chart below plots relative-strength of the Vanguard FTSE All World Ex-US fund (VEU) versus the S&P 500 (SPY). VEU samples an index of non-US equities representing approximately 50% of global capitalization. VEU is weighted 46% toward developed Europe, 28% toward developed pacific, and 19% toward emerging markets. It would be easy to argue that troubles in Europe are driving the divergence. But the issue runs deeper. All of VEU’s constituent regions are in steep downtrends versus the US market.

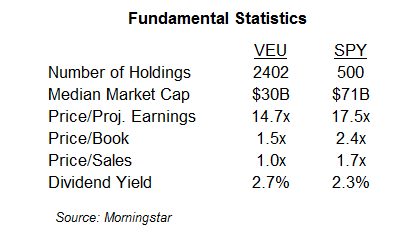

What about valuation? Fundamental parameters from Morningstar are presented below:

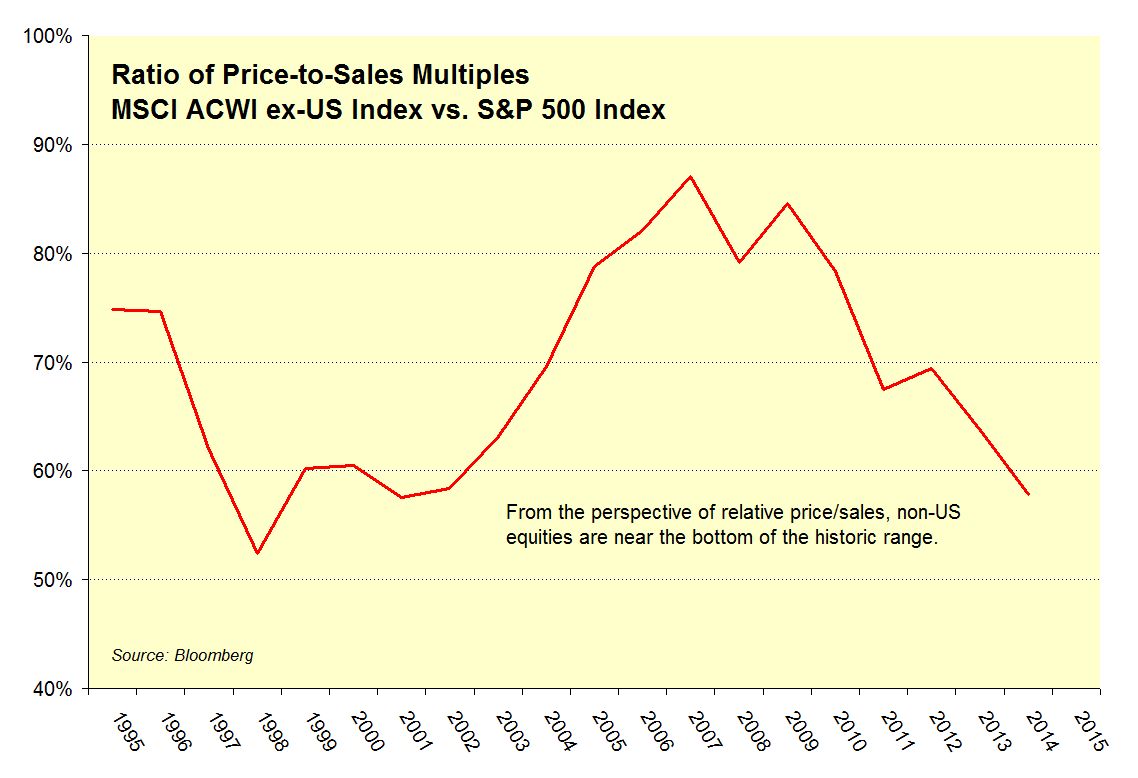

Price-to-sales is probably the most reliable valuation metric, given differences in global accounting standards. Based on current multiples of 1.0x and 1.7x, non-US equities are priced at 58% of US valuation. But be careful with this figure. Non-US equities have always traded at a discount, at least over the past twenty years for which data is available. The chart below presents the historic record based on the MSCI ACWI ex-US Index, a close cousin of VEU. From this angle, non-US equities are indeed cheap, but not as cheap as they get. On average, non-US stocks have traded at 68% of US valuation with a low of 52% in 1998 and a high of 87% in 2007.

So, what might shift the tide in favor of non-US equities? Getting this question even partially correct may well pose the greatest asset allocation opportunity of the next five years or longer. Valuation differentials will eventually put a floor under non-US markets. But this could take more time. As we have argued in the past, we would like to see non-US banks lead non-US markets to the upside. This hasn’t happened yet….