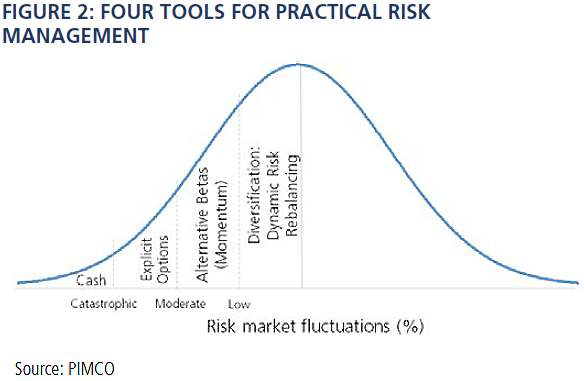

- Risk management in proper portfolio construction consists of a combination of dynamic risk balancing, diversified beta sources, explicit options-based tail hedging and a minimum amount of liquidity.

- Faced with a long and expanding list of things that could go wrong, uncertainties about the likelihood of each shock and the lack of dependable precursory indicators, it seems that a structurally sound portfolio construction methodology that uses all these tools is essential.

- Given how inexpensive tail hedging today is in the context of long term-history, it seems that the risk-reward tradeoff also favors hedging.

We know the story: Chicken Little worries too much about the sky falling, and in a specifically Aussie context, my intrepid friend and colleague Ben Kelly worries about surfing shark-filled waters. But the sky does not fall, and the shark does not bite … until they do.

A few months ago, our desk portfolio managers put on our brainstorming hats and tried to imagine what could make volatility go up, spreads widen, markets sell off and a small element of fear return to the markets. Consensus bull market forecasts were getting us a bit worried, and we felt that we had seen this movie before.

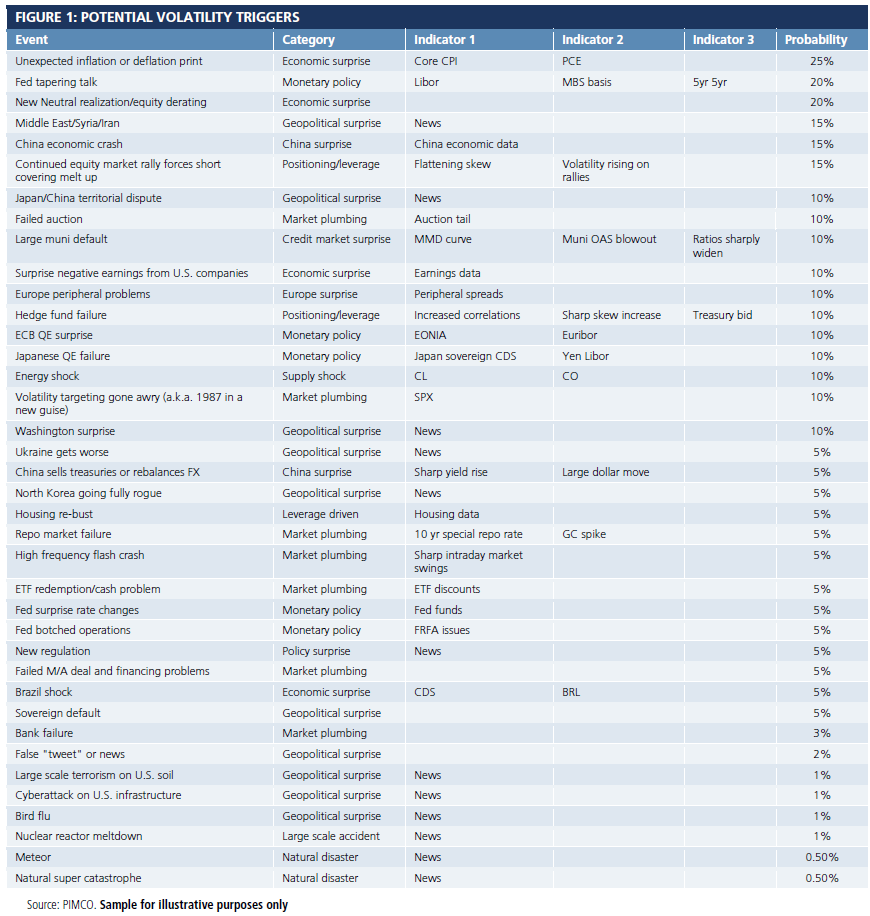

We made the list in Figure 1, and circulated it to the rest of PIMCO’s portfolio managers and to some of our clients. The response was overwhelming, and indeed resulted in expansion of our original list. Momentum in markets has a way of convincing you that Newton’s First Law of Motion applies without fail, and that tail risk management to moderate portfolio risks is only for the aforementioned chicken (who, of course, eventually, and sadly, actually gets eaten by the fox).

Like Chicken Little, we can't know with any certainty what the greatest risk will be in the future. That suggests a broad hedge against risk is prudent – especially when it's inexpensive. Risk management is not just for chickens. (And, if you want to photograph sharks, Ben Kelly will tell you a cage is a good idea!)

But making lists is only the beginning. What we were really interested in doing was to try to quantify our list. To us, this meant doing two things. First, ranking in the order of highest to lowest the events of most gravity, literally – the recent meteor event in Russia found a space on our list, but we think the probability of scientists totally missing the next one (assuming there is a next one) is fairly low: Still, we gave it a 0.5% probability. Second, we asked the question: If an event that would precipitate a market correction were to occur, how could we know ahead, so we could prepare? In other words, what indicator would alert us to take market actions for our portfolios? For each event, we brainstormed a maximum of three potential indicators to watch. It’s still mostly a work in progress.

Two things stand out. First, the list is long, and second, the probabilities are necessarily arbitrary. And, we are still left with the nagging feeling that we might have accidentally missed the most important catalyst (for instance we included the flu epidemic, but totally missed the unfortunate spread of Ebola). But in broad terms, macro and geopolitical risks to us seemed relatively large risks that the market might not be paying enough attention to. Second, the precursory indicators, at first blush, weren’t all that good. In other words, we were not able to come up with a great early warning system by just following what the market knows and can see – e.g. news – though we do have another list of approximately 30, mostly coincident, indicators that we pay some attention to. This has led us to an interesting area of study: the impact of mini-crash and delevering events and how markets react, at very high-frequency (we are talking about 100 millisecond data), and how that applies to low-frequency markets (topic of another paper).

For the time being, we have been working with the operating rule that given how hard it is to forecast and get in front of shocks, it’s smart to tail risk hedge large exposures as part of a permanent asset allocation decision; i.e., what we have often called “always-on” or “just-in-case” instead of “just-in-time.” In addition, as we discussed in one of our recent editorials (see “The Four Modes of Practical Risk Management,” Journal of Portfolio Management, Winter 2013, see Figure 2), risk management in proper portfolio construction consists of a combination of dynamic risk balancing, diversified beta sources, explicit options-based tail hedging and a minimum amount of liquidity. Faced with a long and expanding list of things that could go wrong, uncertainties about the likelihood of each shock and the lack of dependable precursory indicators, it seems that a structurally sound portfolio construction methodology that uses all these tools is essential. Given how inexpensive tail hedging today is in the context of long term-history, it seems that the risk-reward tradeoff also favors hedging.

All investments contain risk and may lose value. Tail risk hedging may involve entering into financial derivatives that are expected to increase in value during the occurrence of tail events. Investing in a tail event instrument could lose all or a portion of its value even in a period of severe market stress. A tail event is unpredictable; therefore, investments in instruments tied to the occurrence of a tail event are speculative. Derivatives may involve certain costs and risks such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested.

This material contains the opinions of the author but not necessarily those of PIMCO. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world.

©2014, PIMCO.

© PIMCO