Last Friday’s jobs report was significant in that for the first time since July of 2008 the unemployment rate dipped below 6%. The September report indicated that the unemployment rate fell from 6.1% to 5.9%. While we have seen improvement in labor markets for some time now, the Fed still seems to want to take their time reducing stimulative policy.

Yellen Dashboard

We know that the Federal Reserve has been reducing their bond purchases all year. The program should come to an end by the end of 2014. The question now weighing on bond investors’ minds is when will they begin to raise short-term interest rates. The Fed Funds rate is pegged near zero and, based on Fed Funds futures, it doesn’t appear that the market believes it will rise much before the third quarter of 2015. The October 2015 Fed Fund futures are trading today near 0.55%.

In order to understand why the Fed feels the need to remain cautious about raising rates, we can look at the Yellen dashboard for some clues (dashboard hyperlink courtesy of Bloomberg). It provides a view of where each factor was before the recession, how it changed during and where it is today. This is a set of labor market indicators used by Fed Chairwoman Janet Yellen to look beyond the unemployment rate to get a better characterization of what is really going on in the U.S. labor market.

The dashboard has a number of indicators that provide more clarity on who is finding jobs, how are people being paid and what is the quality of the labor improvement. It includes measures such as the number of people hired as well as laid off as a percentage of paid workers. It also includes the number of people that have quit and the number of job openings available.

The data in her dashboard also provides more color on the unemployment rate because it includes the number of people working part-time who would rather be working full time if they could find full time employment. It also provides information on the number of people that have been unemployed for more than 27 weeks and the number of people participating in the labor market as a percentage of those that are eligible.

This last piece of information seems to be the most troubling. The participation rate currently stands at 62.7%, up from its low but still nowhere near the better than 66% rate we had pre-recession. There are a number of reasons that appear to be at play here. Most of them have more to do with secular shifts in the economy than specifically related to the recession or the meagre recovery we’ve experienced since. Because they are secular in nature it is possible that the Fed may decide to either remain on hold longer with respect to policy, or they may begin to communicate that the dashboard features have changed so that they can begin raising rates sooner. It seems more likely that the latter will be the case.

Secular Trends

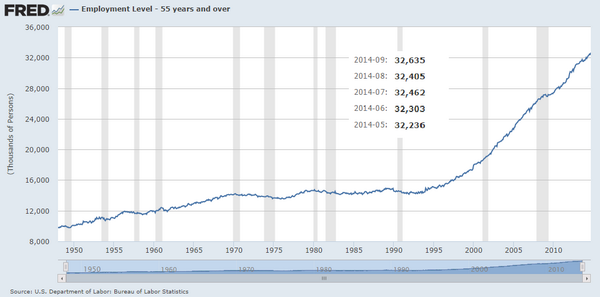

One of the biggest secular trends is the aging of the work force. As older baby boomers remain in the work force longer, both because they want to and in some cases because they have to, the underemployment rate among younger workers is intractably high. At the same time the unemployment rate among older workers in their late 50’s is particularly low, especially among college educated workers. Because the baby boom generation is very large, it is likely that this issue will take some time to work through and as a result we may see the numbers related to people feeling under employed remain high for some time. It is possible this is also why we see such a slack recovery in housing.

Employment Level – 55 years and over

Another secular trend in the labor force is the lower participation rate. Federal programs to provide assistance to those without work have remained in place much longer and in a manner that provides greater assistance than in periods before the recession. As a result, it may have been possible for those people to remain out of the labor force longer, thereby reducing the participation rate.

Price Stability

The Fed seems very focused on the labor market as a justification for their policies. However, their primary objective is price stability. So far, the economy has muddled along at a slow rate of real growth, less than 3% over the last five years, so that inflation hasn’t been a problem. There are also global deflationary forces at work that have provided the Fed a tail wind. Deflation in Japan and Europe and a big slow-down in Chinese economic growth have reduced the pressure on capacity utilization around the world. As a result, the Fed hasn’t had to really fight inflation with higher interest rates.

Germany just posted the lowest level of industrial production they’ve experienced since 2009. China is likely to see slower growth, in the mid-single digits, as a result of their transition to a consumer driven economy. Japan, even with the latest round of Abenomics, can’t seem to get their inflation rate moving in the right direction. With these headwinds, the rate of global growth may continue to be slower even though the U.S. is experiencing some improvement in our own growth rate.

This suggests that, for now, the Fed Funds futures market may have it right. The Fed doesn’t need to be in a hurry to raise rates and probably won’t be.