Uncertain direction of bond market presents unique challenges

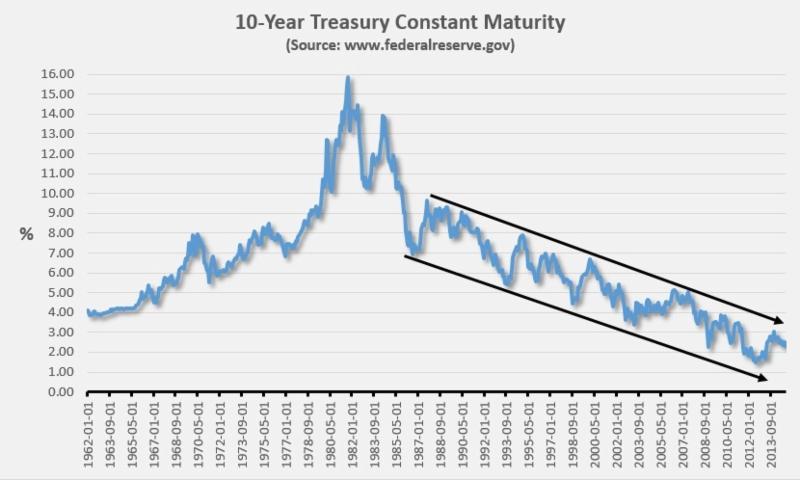

As interest rates fell over the past 30 years, bond investors enjoyed substantial gains due to the subsequent rise in bond prices. Since 1981, the Barclays U.S. Aggregate Bond Index total return is 8.34% annually, providing a big boost for all those stocks/bonds/cash portfolios. During the same time period, U.S. stocks returned 11.25% (S&P 500 TR) and "cash" returned 4.38% (U.S. Money Market). It's the bonds and cash portion we need to examine more closely for one simple reason: Yields can only go to zero (we're basically there), while stocks can grow to the sky.

As the chart shows, this was one giant party for bond holders. Rates have been on a steady decline (and therefore, bonds have been on a steady climb) for so long that no one seems to think it can end. To get an 8%+ return for over 30 years with only a moderate level of risk was the chance of a lifetime, literally. But where do we go from here?

There are three scenarios that can play out. First, rates can continue their descent to "Japanese-style" basement levels of less than 1.0%. Second, rates can meander up and down between say 2%-4% for years to come like they did during the Great Depression. Third, rates can rise from where we are now and continue to rise to who knows where. Let's examine all three.

Scenario #1: Rates continue to decline - This scenario sounds very unlikely, with all the talk of rising rates. Actually, it is quite possible. If you haven't noticed, other than Japan, Germany's yields have now fallen BELOW 1%! The "growth engine of Europe" hasn't had rates that low EVER! We all know that Japan has had their lost decade(s), but Germany? Europe itself seems to be circling the drain, but what about the U.S? We just reported GDP growth of over 3% last quarter. Could we be headed for a slowdown as well?

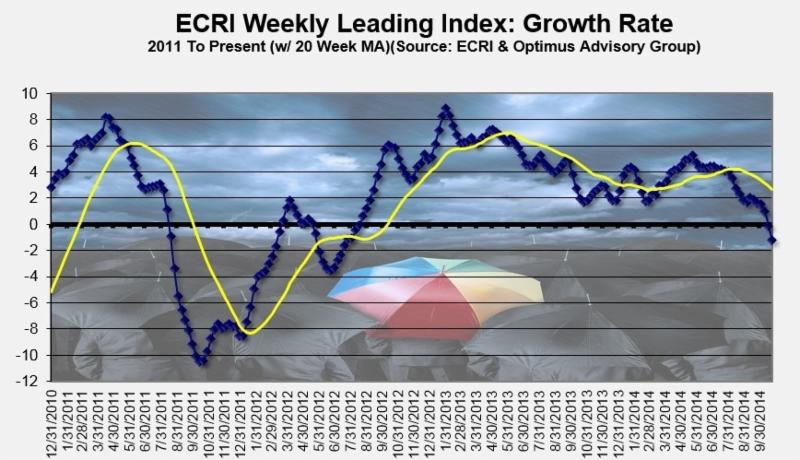

Based on leading indicator data from the Economic Cycle Research Institute (ECRI), the U.S. economy is headed for a slowdown. While their data is not infallible, their leading index did just go negative from an elevated level, something that hasn't happened since 2011. When determining the future direction of rates, economic growth is one factor and inflation is another.

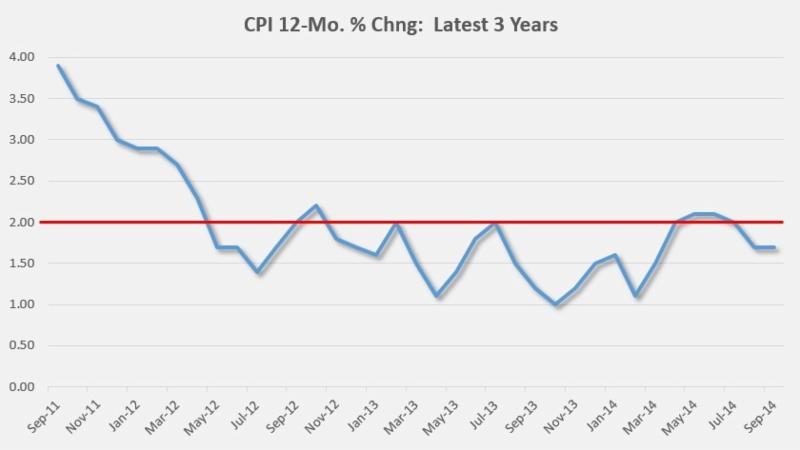

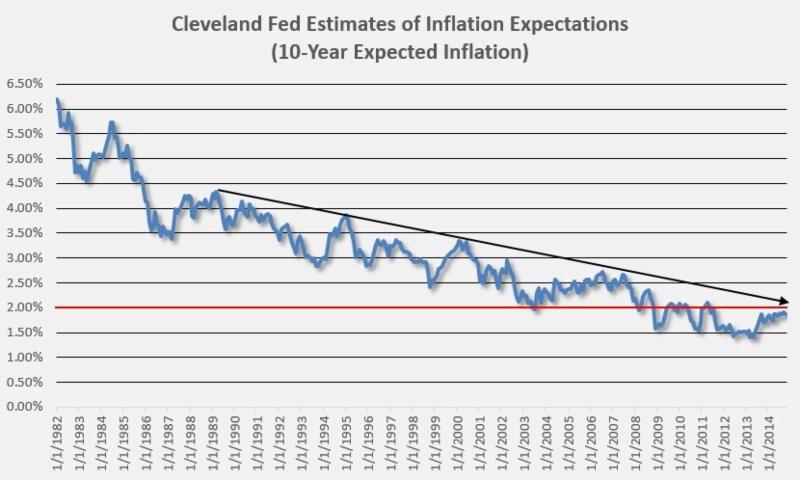

Both the actual inflation data and inflation expectations are at very subdued levels. Many Central Banks including our own like to "target" an inflation rate of 2%. Most of the last few years the CPI has been below that level, along with future long-term inflation expectations. Thus, at this moment, inflation does not seem to be an issue.

If growth is slowing and inflation is subdued, we could easily see a scenario of continuously falling rates meaning modest capital appreciation and low yields for bond holders.

Scenario #2: Rates are range bound - With steady low economic growth and subdued inflation, 10-year Treasury rates could just as easily meander their way between say 2% to 4% for the rest of the decade and beyond. This scenario wouldn't give much in the way of capital appreciation, but would spin off a modest yield.

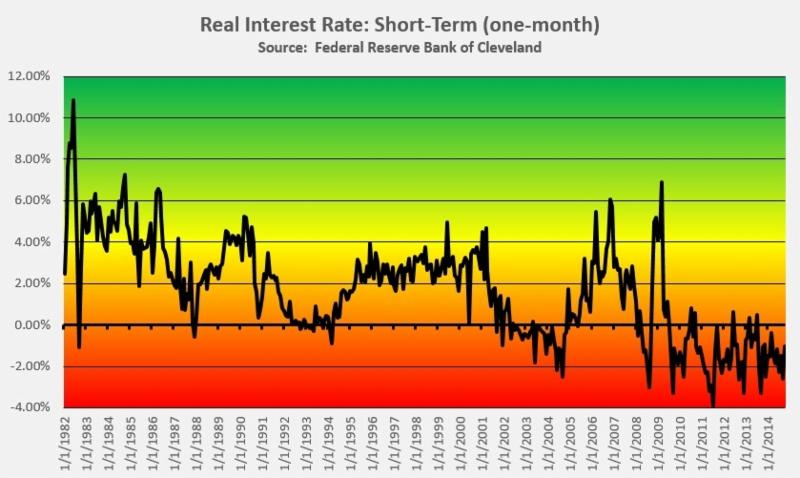

Scenario #1 & #2's common problem - low yields. Falling rates and steady rates have a problem: bargain basement yields. With yields of 2.2% for intermediate-term bonds and zero for money markets, how can investors keep up with inflation? Answer: They can't.

Negative real rates are killing investors, especially those that were scared into dumping all their long-term bonds and going for short-term only. Investors have seen negative real returns for several years now. Being mostly in short-term bonds may keep their account steady (on paper) in volatile markets, but in reality, they are getting crushed by financial repression.

Scenario #3: Rates rise - This is the scenario that has everyone concerned. If rates start a steady climb from 2.2% to 4.2%, 5.2% or higher, bond prices will fall. Long-term bonds will fall hard. Remember, the iShares 20+ Year Treasury Bond ETF (TLT) dropped over -25% from December 2008 to June 2009. That was when yields moved less than 200 bps. The iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD) dropped over -20% between February 2008 and October 2008. Bonds have vicious bear markets too.

2015 & Beyond

Gone are the days of easy money. Today's bond market is not what it was in the 1980s & 1990s when all you had to do was buy some actively managed bond mutual funds and be rewarded with low risk, high single-digit returns. Today's bond market investor is faced with many pitfalls that may prove to be damaging to their financial health.