Investment Implications for UK DC Schemes in Light of Tax and Regulatory Changes

- With greater flexibility and choices available to DC savers in the latter stages of their career, we believe DC schemes need to reconsider their traditional pre-retirement approach to providing low-risk, income-orientated and pre-retirement investment portfolios.

- The primary immediate challenge for UK DC schemes is navigating the need for capital stability versus a portfolio that can generate a sustainable income stream for DC savers in retirement.

- There are a number of PIMCO solutions that could potentially assist in helping DC schemes to successfully address glide path shape, the nature of the equity content and the capital stability of its members at the point of retirement.

Given these new rules, the primary - and most time-critical - consideration for DC schemes is to assess the “pre-retirement” approach embedded within the existing default investment option. No longer is it reasonable to assume (and invest accordingly) that most scheme members will purchase an annuity and take tax-free cash at - or near to - retirement age.

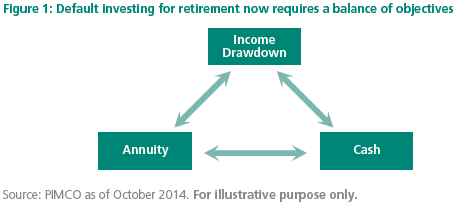

Instead, DC schemes should recognise that their members may choose from

a range of approaches: They may opt to withdraw cash from their fund, take some kind of income drawdown approach to receive regular income in retirement or some may still elect to purchase an annuity. In PIMCO’s view, all three outcomes are plausible. Indeed, we believe that many members may, after considering their retirement guidance, opt for some combination of all three (see Figure 1).

Against this backdrop, many DC schemes need to reconsider their approaches to providing low-risk, income-orientated and pre-retirement investment portfolios to members. PIMCO’s suite of UK fixed income strategies is designed to help DC schemes navigate these new challenges amid the prevailing macroeconomic environment that we call the The New Neutral. The term defines our three- to five-year outlook which foresees a multi-speed world, with countries settling in to historically modest trend rates of potential growth.

Budget changes mean that key risk metrics change too

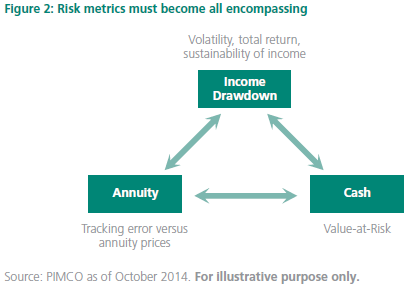

This three-part model represents a material departure from the historical model, necessitating that investment risk parameters change accordingly.

Under the “pre-budget”, or traditional, model, a key metric was a pre-retirement portfolio’s effectiveness in matching changes in annuity prices. This can be thought of as the tracking error between the percentage returns of the investment portfolio and the percentage change in annuity prices. While this metric remains valuable, it is no longer adequate.

Members electing to take an income drawdown approach to fund their retirement will likely be aware of their portfolio’s value, so total volatility and return will be important, as will be the sustainability of a non-guaranteed income stream. Finally, members may elect to take some, or all their portfolio, as cash upon retirement; however, they will also likely be highly concerned with short-term falls in the capital value of their portfolio. Value-at-Risk (VaR), therefore, becomes a critical metric.

Ultimately, the risk positioning of pre-retirement portfolios must now be considered as a balance between tracking error against annuity prices, and the long-term sustainability of income, volatility, total return and VaR.

Pre-retirement investment implications for default portfolios

Today’s increased flexibility available to DC savers should be reflected in default investment portfolios. DC scheme decision-makers face increasing uncertainty over both when and howmembers will withdraw assets.

Uncertainty over when members will begin withdrawing assets has increased

With the liberalisation of tax treatment for withdrawing pension assets, it is plausible that DC savers in the latter stages of their career may supplement their income from pension assets prior to reaching retirement age, perhaps during a transition period of working part-time before full retirement. This would suggest that maintaining a high exposure to risk assets, such as equities, at the point where DC savers can begin to withdraw assets might be inappropriate.

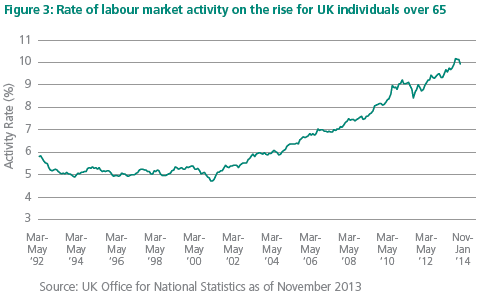

An increasing number of people are continuing to work beyond the traditional retirement age of 65; the activity rate for over 65s has roughly doubled in the past 15 years (see Figure 3). While flexibility around the point at which savers can begin taking pension benefits suggests a lower allocation to risk in the mid-to-late accumulation phase, the trend towards more gradual retirements suggests that at least a modest portion of a default investment option’s allocation to risk assets at the point of retirement might make sense.

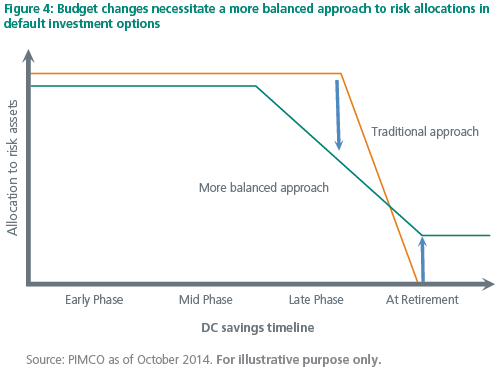

These changes suggest that asset allocation glide paths for default investment options should become more gradual and provide a more balanced transition from risk assets to stable investments, such as fixed income. As allocations to riskier - (and theoretically higher returning) - investments are reduced in mid-life and increased for “at retirement” DC savers (see Figure 4), improving risk-adjusted returns through the use of active management - either to enhance return or reduce risk - becomes more important, whither money-weighted outcomes suffer.

Uncertainty over how members will withdraw assets has increased

An uncomfortable truth about default investment options is that they are ultimately a compromise and may not suit every member, as they should be broadly appropriate for a range of risk tolerances and savings objectives. The UK budget changes have increased the degree of compromise that schemes must embed to ensure that no member is materially harmed by their investment portfolio relative to their eventual decision over the manner through which pension assets are withdrawn: cashing out, drawdown or annuitisation. Successful DC investment default options must now:

- Seek to minimise absolute volatility and downside risk (VaR) for members who ultimately focus on the cash value of their portfolio;

- Seek to minimise tracking error against the cost of a sustainable retirement income, taken through a well-designed income drawdown or an annuity purchase; and

- Pursue adequate long-term returns so that money-weighted outcomes, and the sustainability or level of retirement income, do not suffer.

- We believe that these priorities, which may conflict, suggest that simply relying on market returns (i.e., index investing) will be unsuccessful at navigating the balance of objectives that must now be embedded into default investment options.

Default investment options: potential solutions

Allocations to risk assets for the “at retirement” phase of a DC scheme’s default investment option will depend on a variety of factors, not least the risk tolerance of members and scheme fiduciaries. Given the speed and magnitude of the regulatory changes, we are cognisant of the need to address the glide path shape, the nature of the equity content and the capital stability for DC savers at the point of retirement. We believe that the latter represents the primary challenge for DC schemes to tackle in the immediate future. Hence, specific to fixed income allocations, we believe decision-makers face a quandary over both objectives and strategies: whether to aim to provide stability of asset values through a broadly diversified low volatility approach, an income generative portfolio, or a compromise between capital stability, income generation and tracking error against the cost of a retirement income stream. Please note the strategies discussed below are primarily intended for UK investors and may not be suitable or available to all investors in all jurisdictions.

- UK-focused DC schemes that seek simply to ensure their default investment option has low capital volatility are likely considering cash as a major component of the “at retirement” portfolio. We believe such schemes may want to pursue a diversified, flexible fixed income strategy, such as the PIMCO UK Low Duration Strategy that aims to deliver a premium over cash returns (over market cycles) with very low

capital volatility. - Some schemes may instead wish to pursue a fixed income portfolio

akin to a UK aggregate bond index to reflect a broadly diversified, income-generative fixed income portfolio. The PIMCO UK Income Bond Strategy is designed with such objectives in mind, seeking to achieve attractive yields with a high quality bias to focus on capital preservation, and a broad multi-sector fixed income universe through which to generate returns. - Alternatively, DC schemes may want to pursue a balanced approach of both capital stability and long-term income generation. PIMCO’s UK Retirement Strategy is designed to specifically address the challenges of providing a default investment option for a modern, flexible approach to retirement. The strategy targets a return designed to provide a sustainable income in retirement (achieved through either income drawdown or the purchase of an annuity), while incorporating a tail-risk hedge that seeks to lessen the magnitude of negative absolute returns in adverse fixed income markets. Such a solution may help DC schemes navigate the compromise that default investment options in the pre-retirement phase represent.

Summary

We believe that the primary objective of default investment options should be to pursue a prudent, thoughtful approach that is broadly suitable for a member who has not made any specific decisions about their DC investments. These strategies must be designed to account for the fact that members’ retirement income needs reflect a future income stream in retirement, but must also seek to mitigate total, and particularly downside, volatility in the event that members elect to take cash instead.

Finally, DC scheme governance bodies may want to re-evaluate the manner in which they consider and monitor investment risk: They should contemplate the overall return and absolute volatility of their scheme’s default investment strategy, the tracking error relative to the changes in cost of a sustainable retirement income stream (both secured through an annuity and otherwise) and the VaR of the strategy in order to adequately monitor the key risks faced by scheme members.

About PIMCO and Our DC Practice

Headquartered in Newport Beach, California, PIMCO is a global investment management firm with over 2,000 dedicated professionals focusing on a single mission: to manage risks and deliver returns for our clients. For four decades, we have managed the retirement and investment assets for a wide range of investors, including corporations, governments, not-for-profits, and other organisations, as well as for individuals around the globe.

As of 30 September 2014 our:

- Clients include more than two-thirds the Fortune 100

- Investment professionals on staff exceed 700

- Global presence includes offices in 13 locations

- Total assets under management exceed $1.87 trillion / £1.15 trillion

- DC assets under management over $191.1 billion / £117.88 billion

Our PIMCO DC Practice is dedicated to promoting effective DC plan design and innovative retirement solutions. We are among the largest managers of assets in defined contribution plans, offering investment management for stable value, fixed-income, inflation protection, equity and asset allocation strategies such as target-date solutions. We also provide analytic modeling, plus can help plan sponsors identify DC consultant resources. Our team is pleased to support our clients and the broader retirement community by sharing ideas and developments for DC plans in the hopes of fostering a more secure financial future for workers. If you have any questions about the PIMCO DC Practice, please contact your PIMCO representative.

Past performance is not a guarantee or a reliable indicator of future results. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investing in foreign denominated and/or domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets.Equities may decline in value due to both real and perceived general market, economic, and industry conditions. Tail risk hedging may involve entering into financial derivatives that are expected to increase in value during the occurrence of tail events. Investing in a tail event instrument could lose all or a portion of its value even in a period of severe market stress. A tail event is unpredictable; therefore, investments in instruments tied to the occurrence of a tail event are speculative. Derivatives may involve certain costs and risks such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. Diversification does not ensure against loss. Thecredit quality of a particular security or group of securities does not ensure the stability or safety of the overall portfolio.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

Tracking error to liabilities assumes that all the plan assets are invested in fixed income and we calculate the performance dispersion of the 100% fixed income portfolio relative to the liability performance. Value at Risk (VAR) estimates the risk of loss of an investment or portfolio over a given time period under normal market conditions in terms of a specific percentile threshold of loss (i.e., for a given threshold of X%, under the specific modeling assumptions used, the portfolio will incur a loss in excess of the VAR X percent of the time. Different VAR calculation methodologies may be used. VAR models can help understand what future return or loss profiles might be. However, the effectiveness of a VAR calculation is in fact constrained by its limited assumptions (for example, assumptions may involve, among other things, probability distributions, historical return modeling, factor selection, risk factor correlation, simulation methodologies). It is important that investors understand the nature of these limitations when relying upon VAR analyses.

This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark or registered trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. THE NEW NEUTRAL and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Pacific Investment Management Company LLC in the United States and throughout the world.

©2014, PIMCO.

© PIMCO