Super Bowl losing teams are usually quickly forgotten—consigned, as the expression goes, to history’s dustbin. In fact, some NFL historians and coaches have said that the losers of the semi-finals (conference title game) have often received more long-term recognition than the Super Bowl losers, for the simple reason they may have played the Super Bowl winner much tougher in the earlier round.

Of course, there have been many exceptions to the forgotten Super Bowl losers, but not necessarily for the right reasons. The original Baltimore Colts will always be remembered for being the first NFL team to lose the Super Bowl to an upstart AFL team—Joe Namath’s New York Jets in the third Super Bowl (1969).

The Denver Broncos of Super Bowl XXIV (1990) are considered by some to have put in the weakest all-time performance, losing 55-10 to Joe Montana’s San Francisco 49ers. The Buffalo Bills have the unforgettable distinction of having lost all four of their Super Bowl appearances, including the infamous “wide right” missed field goal attempt against the NY Giants in XXV. And despite their mighty dynasty, the then-undefeated New England Patriots are recalled for being on the losing side of one of the Super Bowl’s most miraculous plays in XLII (the Giants’ Manning to Tyree). On a more positive note, the Dallas Cowboys will forever be remembered for two terrific and exciting losing efforts against the Pittsburgh Steelers’ dynasty of the 1970s.

The Seattle Seahawks of Super Bowl XLIX will be recalled for a very long time—as you likely have heard a hundred times on sports radio and TV shows—for the “worst play call in Super Bowl history.”

Let’s skip the highly overanalyzed details of the end-of-the-fourth quarter fiasco for the Seahawks and see if there is anything we can learn from the game. If financial authors can cite investing wisdom that may be gleaned from kindergarten or from playing Monopoly, certainly there must be some important investing lessons emanating from the 2015 Super Bowl, no? At least some of the business press thinks so, especially from the game and clock management of the Seahawks’ coaching staff.

There have been several fairly common themes to the articles, saying, “Don’t pull a Pete Carroll with your investments”:

- “Plan ahead for crucial decisions.” These critics believe Carroll and his staff should have had a preset play selection list for end-of-game goal line situations, eliminating any confusion and last-minute emotional duress in a tight situation where outcomes are uncertain. Some feel Carroll was a bit rattled, not managing the clock or timeouts well and acting rashly. According to Carroll, they did have a plan, but it just didn’t work out.

- “Don’t buy into a hot investment fad.” While a bit of a stretch, this analogy says the Seahawks’ coaching staff played it far too cute and clever, ignoring the higher odds of their “tried and true” running game versus trying to outsmart the Patriots with an unexpected, tricky play.

- “Stick with your strengths.” Similar to the previous truism, this says that if Seattle preferred to try a pass play instead of having Marshawn Lynch run it up the middle, they should at least have gone with the strengths of the best-running QB in the league, Russell Wilson, and tried a play action fake or pure rollout pass play.

- “Mean reversion eventually comes into play.” This one is quite interesting, I think, and says that Seattle had lived throughout a) the season, b) the conference final with the Green Bay Packers, and, indeed, c) the Super Bowl, on high-risk play calling. Risk had to eventually jump up and crush them when least expected.

Let’s take this last point and put an active management spin on it for Super Bowl investing lessons. By calling for a pass play on the one-yard line and second down, and in using a quick slant pass over the middle in the most congested area of an already tight field, the Seahawks brought a “black swan” outcome into the equation.

Had they perhaps applied the risk-mitigating principles of active management, they certainly would have tried a far less chancy running play or a conservative pass into the corner of the end zone—minimizing the odds of having the only thing happen that could end their season right then and there. Let’s not kick Pete Carroll and his staff when they are down, but despite all of his protestations, you just know he wishes he had that play call to do over again—just like many investors who regret their actions during the last two market crashes of the past fifteen years.

On the topic of risk, last week in the markets saw the continuation of the highly volatile trading that has characterized 2015, though this time to the upside. The Dow (DJIA) put in a gain of 3.80%, its best week in two years. The S&P 500 (+3.00%) and NASDAQ Composite (+2.40%) also performed well.

Various theories were put forward for the market turnaround after the very poor start to the year in January, including: crude’s move back higher off what some saw as a bottoming process; the ever-changing prospects for Greece’s financial situation; the now-typical “buy the dip” trade on oversold market conditions; and some (but not all) encouraging news on the earnings front. Others gave some credit to comments from Warren Buffett, who claimed there would be no Fed rate hike this year (though markets seemed to walk away from this on Friday, “selling the good news” of the jobs report on the theory it might force the Fed’s hand).

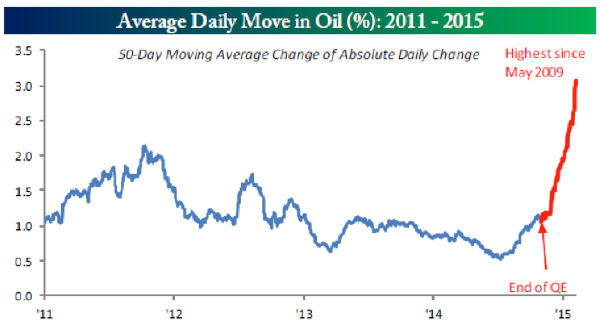

Some astute market observers believe last week’s market action was indeed closely tied to the rise in crude oil prices (WTI crude oil was up 7.4% on the week and has had a very bullish move from its intraday low of $43.58 on 1/29 to last week’s intraday high of $54.24). Said one, “The recent stock market has been driven by the price of oil on a daily basis. Wall Street’s computers have created correlation trades that tie buy and sell programs in the stock market to the movement in oil futures.”

No matter what one believes on the fundamentals and global politics of the oil price situation, one thing is certain: volatility has skyrocketed. According to Bespoke Investment Group, “The pickup in volatility for crude oil takes the cake, with a recent average daily move of 3.1%—the highest reading since May 2009.”

Source: Bespoke Investment Group

I am not sure there are any Super Bowl lessons for how to trade crude oil in this volatile environment. But for those who believe in the “Super Bowl Indicator” for the stock market, and its claimed 80% success rate, there is yet another unfortunate aspect to the Seahawks’ loss. With the AFC Patriots winning, this Indicator claims equity markets are destined for a down year.

Let’s all try and have a great week anyway.

All the best,

Jerry

http://www.flexibleplan.com/market-hotline/disclosures