Over 25 years ago I took my family (my wife, Pat, and two sons, Michael and David) to the big island of Hawaii. It was a dream comes true.

We’d been to Honolulu, Kauai, and Maui, but not to the Big Island. Our family spent two weeks in a car circumnavigating the isle on our own. It was a joy not to be forgotten.

Early on in our trip, it became apparent that the major island attractions (after the live volcano that is) were the waterfalls. We seemed to race from one waterfall to another as we circled the island.

Finding them became like a giant scavenger hunt. A few stood very accessible, right by the side of the road. Many were the prize at the end of a dirt trail and a well-worn footpath after that.

Some began high above the tree tops in the mountain crags. Others were nestled amongst the fronds and other native greenery, emerging as if the source of a bubbling creek that meandered down a stony path back into the jungle brush.

All were beautiful. Many were breathtaking.

Unfortunately, life is not all vacation time and not all waterfalls are beautiful.

The price action in the Chinese stock market is indicative of this. A decade ago some market gurus were talking about the Chinese stock market as a one-way street, and that road only led higher. How could it miss? A billion people in an economy emerging from a socialist economic winter into the capitalist sunshine.

There was infrastructure to build. Peasants were leaving the great farming collectives of Mao and moving to the cities, where services and manufacturing were flourishing. They needed housing, and perhaps the world’s greatest housing boom ever commenced.

Yet it did not turn out that Chinese stocks could only go up. Instead, they fell and they experienced years of declines and sideways markets before finally rallying beginning in last year’s second half.

Then the bottom began to drop out. By last week the value of the Shanghai stock market had shrunk by over 27% … IN LESS THAN A MONTH!

Source: Bespoke Investment Group

In market parlance this is called a “waterfall decline.” These declines happen suddenly and often violently. Like water from a gentle stream hitting the edge of a cliff that suddenly plunges over and out into the abyss and does not find support until it splashes with a roar on the rocky riverbed below, asset prices in a waterfall decline seem to rush to plummet to depths that are unknowable in advance.

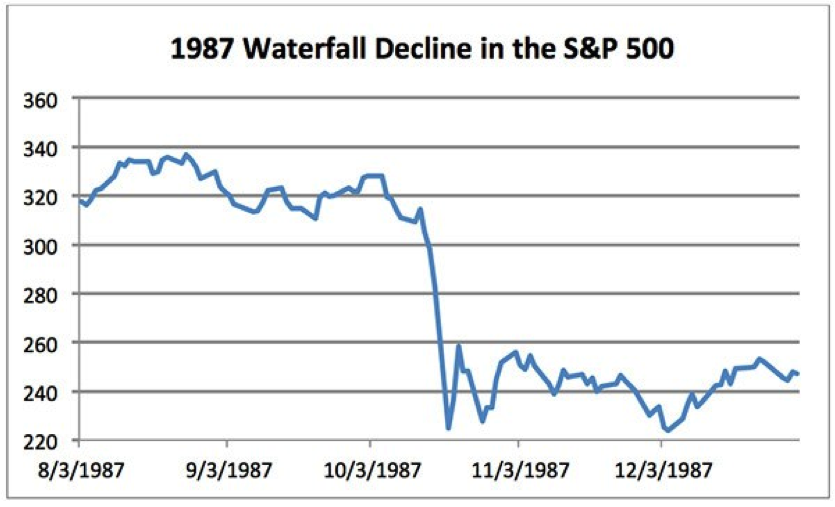

Our own stock market experienced a similar decline in 1987. In a two-week period, the stock market plunged over 33%. On one day alone, a $100,000 account invested in the S&P 500 would have lost more than $24,500.

Source: Flexible Plan Investments research

While both of these examples arise from stock market activity, neither bonds nor commodities are immune to these events. Check out the 20%+ plunge in oil futures prices just over the last three weeks and the collapse of the German Bund since April.

Source: Bespoke Investment Group

How does one invest in an investment world where such loss of capital, regardless of asset class, is always possible? And if history is our guide, for anyone who is invested long enough these events are inevitable!

The conventional answer is to diversify. As the story goes, by investing in many different asset classes your portfolio will dissipate the losses of one asset class with gains experienced in another.

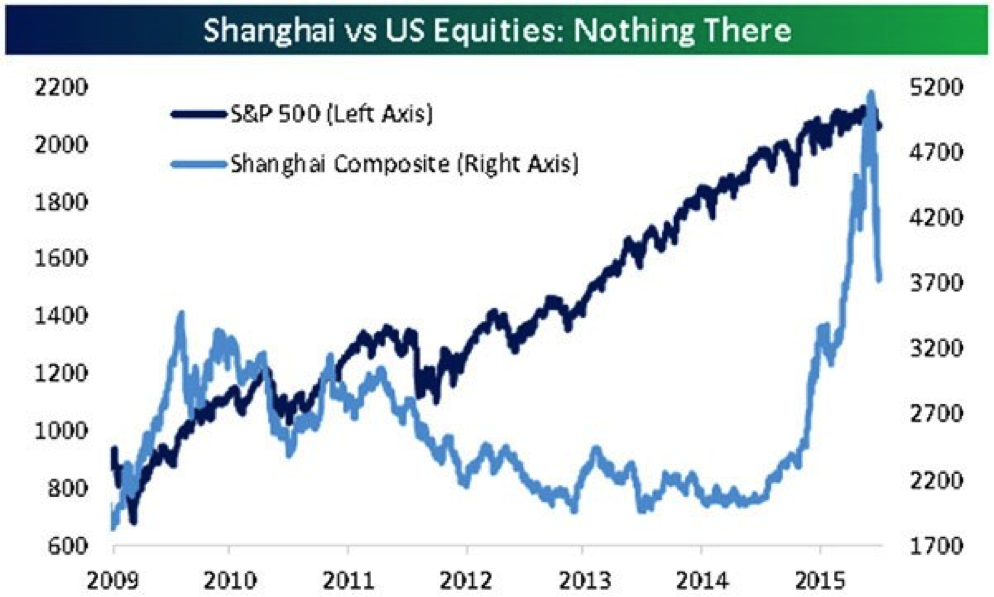

Like any bit of conventional wisdom, it is correct … some of the time. Like last week, while the Chinese market was falling, our graph demonstrates that our stock market held up pretty well. It has not been blindly following the Chinese party line for years.

Source: Bespoke Investment Group

At other times, notably the 2007-2008 market crash, everything moves down together regardless of asset class. Historically, the only exceptions during these times have been gold and bonds. Of course, with both of these asset classes in bear markets of their own at the present time, they may not provide much diversification.

What do we do then? There are two answers. Tactical strategies that move in and out of the asset class try to anticipate declines. These can be very effective, but investors need to understand that there is no tactical strategy that is always right (60% accuracy is considered excellent). Also, many tactical strategies are trend-following based and they rarely can avoid waterfall declines.

Other tactical strategies are mean-reversion based. These follow short-term market patterns that can quickly reverse, providing profits. While these tend to work in fewer market environments than trend-following strategies, they can be effective with waterfall decline events.

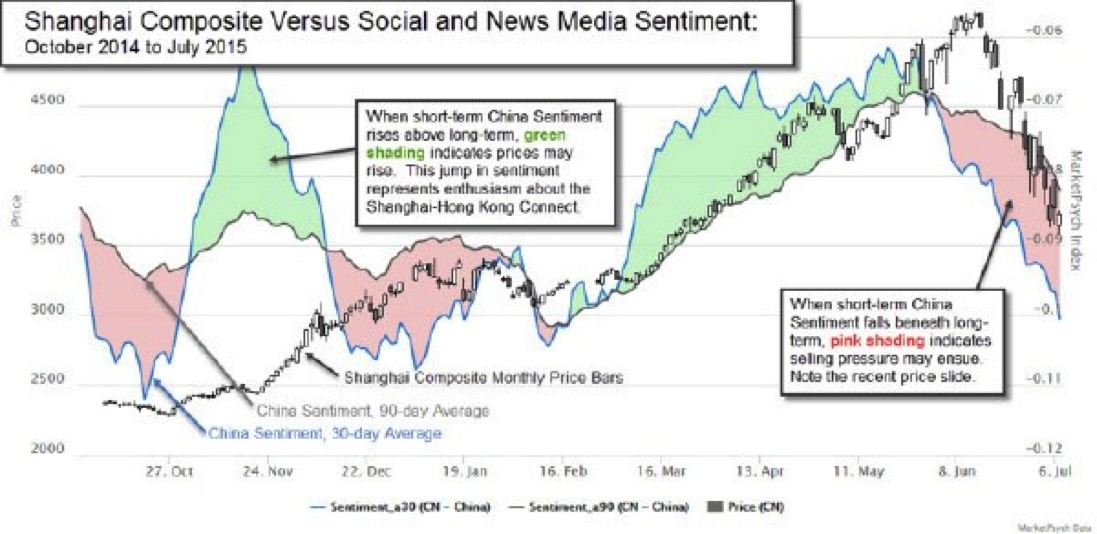

Finally, there are a whole host of tactical strategies based on price and fundamental patterns and market sentiment. At the upcoming ProActive Advisor Conference here on the International Riverfront in Detroit, September 15-16, one of the speakers will be Dr. Richard Peterson. He is one of the leading experts in the world on market sentiment and created the Thomson- Reuters MarketPsych Indices.

Source: MarketPsych

Here’s how one of his indices, based solely on the volume of Internet and social media mentions of China, actually forecast the “waterfall decline” of the last month in the Chinese market.

Chinese business sentiment appears to lead the Shanghai Composite somewhat. The shading between the two averages is pink if the 30-day average is lower than the 90-day average, and it is green if the 30-day average is higher than the 90-day. When the short-term sentiment rises rapidly, it tends to pull prices upwards, and when it falls, prices tend to follow down. Such sentiment moving average crossovers have appeared a useful indicator for timing bubble tops in historical testing, and we see examples of sentiment driving prices most often during dramatic events (bubbles and crashes). The MarketPsych Newsletter.

Of course, it is also obvious from the chart that the methodology can get it wrong, with sentiment plunging but stock prices moving still higher. And, of course, that’s the problem of relying exclusively on tactical strategies. Sometimes they are very right and sometimes they can be very wrong.

What’s the solution? Well, it’s actually a return to the conventional wisdom—more diversification. But it must be true diversification; the use of asset classes like gold and bonds, but also the inclusion of a variety of dynamically managed (including tactical) strategies that have a history of not following in lock step with the major market averages.

This won’t make the waterfall declines look beautiful, but it can change a frightening plunge over the cliff into a quick whirl ‘round the bend on a white water rafting trip. It’s over quickly and it’s much more enjoyable, and survivable.

All the best,

Jerry

P.S.: Market Update

The markets continue to be held hostage by the headlines – Iran, Greece, China, and now second quarter earnings reports.

I know the stock market opened up in a buying frenzy due to the release last night of an outline of a path through the Greek financial mess. Most markets around the world were up more than 1% by noon our time. Many had gained more than double that amount. I’d like to be optimistic and say this is now behind us, but I know it isn’t so. There remain many hurdles to be jumped before we end this race. As my friend David Moenning said in his State of the Markets’ blog today:

Oh, it is also worth noting that (a) the terms of the this deal are actually much tougher than the one the citizens of Greece voted to thumb their noses at last weekend, (b) the negotiations won’t start until Greece actually passes the new austerity and reform measures, and © the deal has to be passed by the Greek parliament and various Eurozone member states. As such, anyone thinking that Greece is now “fixed” and that the latest drama is over may need to think again. - See more at: http://stateofthemarkets.com/report/52568/ - sthash.g5s4V5N7.dpuf

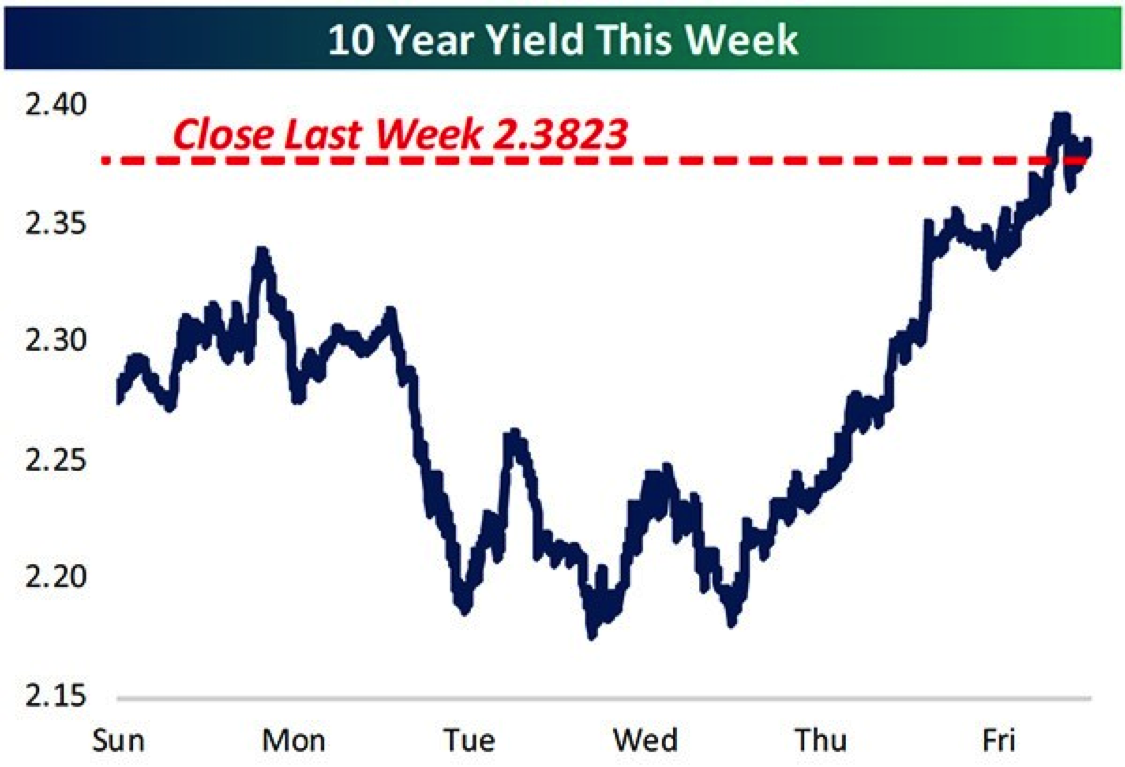

Interest rates also remain a concern. While there have been some flight-to -safety rallies in bonds, the price of bonds continues to generally trend lower. Just take this chart of rising T-Bond yields and turn it upside down and you’ll see a waterfall decline that reflects what’s happening to bond prices these days.

Source: Bespoke Investment Group

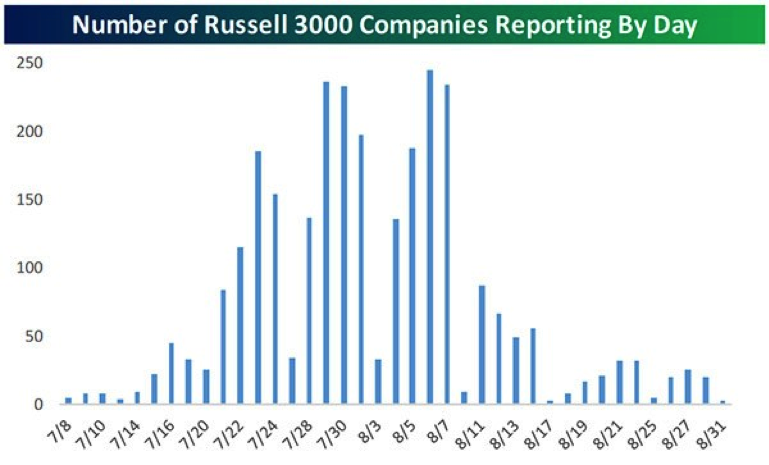

Finally, I mentioned that earnings reports for the second quarter will soon be filling the headlines. In fact, reporting season started the middle of last week. While the chart shows that the number will accelerate from here during the typical six-week reporting season, I don’t think that’s a bad thing.

Source: Bespoke Investment Group

Rather, once again the earnings analysts have set us up for a rally, as I expect more reports will beat expectations recently lowered by them. More than 80% of the time in this bull market when analysts have had more negative revisions than positive revisions (as has been the case during this off-season), the S&P 500 has moved on average about 2.5% higher during the six-week earnings reporting period.

Finally, a number of major stock market cycles will predictably bottom in the next month or so. If the future follows the past even roughly, we could have a strong rally in the last four or five months of the year as these business cycle patterns work their magic. The long-term and intermediate market trends continue to support this expectation as well.

With a portfolio truly diversified among asset classes and dynamically managed strategies, anytime is a good time to begin a new portfolio or add to an existing one. The way I see it, there’s always a rainbow someplace around a waterfall, no matter which type we are talking about – the ugly or the beautiful.

http://www.flexibleplan.com/market-hotline/disclosures